Newcastle’s John Hunter Health Campus is in line for a $780-million redevelopment including a new acute services building to help provide healthcare for the region’s growing population.

The State Significant Development has won approval from the New South Wales government to redevelop and future-proof the healthcare precinct in the western suburbs of Newcastle, which currently regularly operates at 98 per cent capacity.

The government originally announced the John Hunter Health and Innovation Precinct in 2019.

Architecture firm BVN said it would “deliver an innovative and integrated precinct” which would meet the future needs of residents in the Hunter.

“The John Hunter Health and Innovation Precinct Project is being planned and designed with ongoing communication and engagement with clinical staff, operational staff, the community and other key stakeholders,” the BVN design report said.

“The proposal will facilitate the development of a new state-of-the-art health facility which will further support and strengthen the services and facilities provided at the hospital for the benefit of the Hunter New England Local Health District.”

According to town planners Ethos Urban, the redevelopment was a “significant investment in the Hunter region” and would deliver about 5500 direct and indirect jobs during the construction phase, and ongoing health services jobs in Newcastle and the Hunter region.

The approved plans are for a new seven-storey acute services building to expand and enhance the emergency department, intensive care services, operating theatres, women’s services, a new rooftop helipad and increased car parking.

It also includes the refurbishment of existing buildings to provide additional inpatient units, a new Hospital entry canopy, new roads, a link bridge to the Hunter Medical Research Institute, and connections to the Newcastle Inner City Bypass.▲ A new entry canopy to the hospital and a seven-storey acute services building are part of the redevelopment of the John Hunter Health Innovation Precinct.

NSW health minister Brad Hazzard said the redevelopment would significantly increase critical care capacity, with a 60 per cent increase in the Intensive Care Unit capacity, and almost 50 per cent more operating theatres.

“The precinct will drive innovative collaborations between the health, education and research sectors, ultimately improving patient outcomes for communities in the Hunter region,” Hazzard said.

Hazzard officially opened a $194-million clinical services building at Coffs Harbour Hospital earlier this month.

“This is an incredible transformation of critical health care for the Coffs Harbour and surrounding communities, which will now benefit form a much larger emergency department, additional operating theatres and inpatient beds,” Hazzard said.

“The NSW government is committed to providing world-class health care to all NSW residents, no matter where they live.”

In the year she has spent trying to secure a family home in Newcastle, Sally has missed out on multiple auctions and offers.

“Homes are going $300,000 to $400,000 over guide,” she said.

“It’s a really tough time to enter the market.

“It’s just making the disparity of wealth wider and wider among families.”

Martin Jackson has been searching for land in the Hunter Valley for two years to set up a cellar door to showcase his wines, which are made from honey. “It’s disappointing that there’s not much on offer for less than a million dollars,” he said. “The prices two years ago were reasonable … I’ve noticed, probably in the last six months, there’s been a massive surge.

Land values soar

Property remains hot across regional New South Wales and is contributing to higher land values.

The Valuer General’s analysis of 67,000 sales in the 2020-21 financial year found soaring residential land values in regional areas.

Selena McMullen, senior project officer for the Valuer General’s office, says land values are based on the analysis of property sales.

“Statewide, the increases have been driven by COVID and the trend to working from home, which has allowed purchasers to look at some lifestyle changes, whether it be a green change or a tree change or a sea change,” she said.

The Hunter Coast saw the largest increase to total land values, including residential, compared to other NSW regions.

Residential land values rose by more than 38 per cent for the Central Coast, Lake Macquarie, Newcastle and Port Stephens local government areas collectively.

The previous year’s rise for the Hunter Coast was just more two per cent.

Across the state, residential land values increased by almost 25 per cent compared to about four per cent the previous year.

Pockets of regional NSW saw much larger rises, including Kiama and Byron Bay, which increased by more than 50 per cent.

Will this affect your rates?

Revenue NSW will use the land values to help calculate the 2022 land tax with assessments averaged out over a three-year period.

Ms McMullen said this set of values would not be used for council rates and stressed that any increase would be determined by a rate peg set by the Independent Pricing and Regulatory Tribunal.

“Landowners don’t need to worry about these land values impacting on their rates,” she said.

Other land value types, including commercial, have also increased.

For the Hunter Coast, values increased by more than 29 per cent, slightly behind Sydney’s west, which saw the largest jump of more than 30 per cent.

Rod Dever, president of the Gosford Chamber of Commerce on the Central Coast, said the region was attractive to business owners because of its proximity to Sydney.

“If you look at it over a five-year time period, then I think it’s a great thing,” he said.

“It’s attracting new business, it’s attracting business growth, it’s increasing the valuation and the importance of the Central Coast as a commercial and business space.”

Opposition Leader Anthony Albanese will promise hundreds of millions of dollars for a fast rail link between Sydney and Newcastle if Labor wins the upcoming federal election as part of a plan to start a high-speed rail network along the nation’s east coast.

Mr Albanese, who will unveil the plan at a speech on Sunday in the Labor heartland of Newcastle, said a $500 million down payment for the new link between the regional centre and the country’s largest capital city would be provided in his first federal budget. The initial funds would help cover the purchase of land in the corridor, planning and early works but the project would require state government involvement.

Labor previously said it would create a high-speed rail authority if it won the upcoming federal election in an effort to launch a “nation building” project running from Melbourne to Brisbane. Trains on the line would run at 350km/h and stop in Canberra, Sydney and other regional centres.

“The growth that we’ve seen outside [capital cities] will accelerate and that growth, when you look at decentralisation, is more attractive for people,” Mr Albanese told The Sun-Herald and The Age ahead of the speech.

He said shorter commutes from regional areas could help with housing affordability, reduce emissions and road accidents from the number of cars commuting and encourage more businesses to move out of the capitals. Cost of living, including property prices, has become an early fighting ground between the Coalition and Labor in the lead-up to the election.

“If you change that dynamic [the length of time it takes to get from regional hubs to capital cities] you change the economics of business locations in favour of decentralisation,” he said.

The high-speed rail network would include stops on the Central Coast and cut a trip from Sydney to Newcastle to 45 minutes. At the moment the trip takes 2½ hours. The initial stage of fast rail would cut this leg of the journey to two hours.

Mr Albanese will also unveil plans on Sunday to provide additional support for after-hours GP access, reversing about $500,000 in cuts. Labor says operating hours have been reduced at after-hours healthcare clinics in areas including Newcastle. The service assists 50,000 patients a year including through 70,000 telephone consults.

During the 2019 federal election Labor suffered a significant swing in the seat of Hunter. In the 2021 Upper Hunter state byelection there was also a notable swing against Labor.

The NSW government has been undertaking planning work to provide a fast rail line between Sydney and Newcastle, with proposals and discussions about the potential of these links under way for years.

In April, former NSW premier Gladys Berejiklian said the government was renewing its commitment to faster rail to regional centres. Federal Labor’s plans are in line with existing state plans but would aim to speed up the delivery of the infrastructure.

Mr Albanese said fast rail was a “genuinely transformative project” and would need to be undertaken with the states.

“We’ll provide the funding straight away, but we will sit down with NSW and it would have to be the subject of appropriate conversation [with the state government],” Mr Albanese said. “Sydney is the key.”

When this part of the project was secured, he said there would be scope for the authority to work on a Sydney to Melbourne link where there were clear economic benefits for the investment.

“We’ll have more to say on corridor acquisition and other things [for that part of the link] down the track,” he said.

“The Commonwealth should be playing a role in genuine economic transformation … and looking for projects that boost productivity and boost the economy.”

The Urban Developer’s latest Brisbane housing market insights reveals that the city’s house prices is on track to outperform all other Australian capitals during the next 12 months.

This resource, updated periodically, will collate and examine the economic levers pushing and pulling Brisbane’s housing market.

Combining market research, rolling indices and expert market opinion, this evolving hub will act as a pulse check for those wanting to take a closer look at the movements across the market.

Brisbane housing prices grew almost three times as much as expected this past year, with prices set to rise further amid fresh predictions it will outperform all other Australian capitals in 2022.

Brisbane has well and truly surpassed expectations of a dwelling price rise of 8 per cent in 2021, instead notching a 25 per cent jump off increased interstate migration, low stock and heightened demand.

Brisbane’s house prices have increased by a staggering 27.9 per cent in the past year, with the median price now $757,000, following a peak-to-trough fall in values of -1.4 per cent between April and September 2020.

November’s bump in dwelling prices was a modest increase from the previous month, when dwelling values grew at a rate of 2.5 per cent.

House price growth has also seen an uptick and unit prices have lost some momentum after lifting by 2.8 per cent and 1.3 per cent respectively in October.

According to Corelogic, property values rose 2.9 per cent in November—the biggest increase of any capital city—to be up 25.1 per cent over the year, providing sellers with a gross yield of 3.8 per cent.

The rise in Brisbane home values over November, the most in 18 years, was closely followed by Adelaide, which was up 2.5 per cent for the month, the biggest gain in 28 years.

The current median value for a property is now $662,000, and has further advanced an additional $20,000 during November.

A typical Brisbane house is now about $180,000 more expensive than it was at the beginning of January, while units have experienced a gain of $52,000.

Brisbane’s north remains a hot spot for property price growth, with an increase of 24 per cent across the year, while inner Brisbane houses have recorded record rises of up to 28 per cent for the year.

In the past three months, Bunya in Moreton Bay has surged by 12 per cent with a similar increase in Auchenflower in the inner west.

Teneriffe and New Farm have now crossed the $2-million median mark with Ascot and Hamilton likely to follow suit early next year.

Brisbane’s housing market: policy updates and trends

Affordability, not interest rates will slow housing market

Concerns about the impact of a possible interest rate rise on the booming property market may be growing, but opinion is sharply divided over what effect it may have, and when.

The Reserve Bank of Australia has indicated an interest rate rise was likely to remain at 0.10 per cent in 2022 after dropping to that level in November 2020.

Home buyers the winners as owners rush to sell

Residential listings are set to pile up when the housing market reopens in January with a surge in the number of homeowners looking to sell before prices peak.

Requests for appraisals have jumped by 19 per cent in Brisbane indicating that a large number of potential vendors are looking to enter the market in the new year.

Olympics to push Brisbane market’s limits

Brisbane house prices could more than double by the time the 2032 Olympic Games roll around, taking median home values above $1.4 million, economists predict.

The growth rate would be consistent with the market’s past performance during the G20 summit in 2014 in Brisbane, when dwelling prices surged 112.7 per cent over 12 years from when the event was announced in 2003 to 2015, a year after it was held.

What the experts are saying about Brisbane’s housing market

Eliza Owen Head of Research Corelogic

“The housing market is well and truly past its peak for the current cycle, and it makes sense that as more headwinds accumulate, price increases will continue to slow, and more suburbs may see an adjustment in price.

“Fixed mortgage rates appear to be bottoming out, and this will limit the amount of finance that can be taken out as well.

“In the short term, we’ve still got a week or two before we hit the peak spring selling season, so more available listings will reduce price pressures.”

Shane Oliver Chief Economist AMP Capital

“By the end of next year, I think the upswing will come to an end, and we’ll start to see price falls as higher interest rates feed through.

“I think later next year, we’ll start to see higher variable rates, and the combination of higher interest rates, poor affordability and increased listings, I think will start to weigh on the property market.

“The overall picture for the housing market is still strong, but it’s slowing, and I suspect that as we go into next year, the pace of growth will slow dramatically.”

Nicola Powell Senior Research Analyst Domain

“The [recent] surge in appraisals is quite revealing, particularly at this point in time as we’re so close to the end of the year.

“I think this shows that more homeowners are thinking of putting their homes on the market, for fear of missing out on the peak, and that will probably come to fruition early next year.

“Housing stock is now building up and rapidly changing the dynamics in the market in favour of the buyers.

Louis Christopher Managing Director SQM Research

“The win of the 2032 Brisbane Olympic Games is clearly a positive for the city’s economy.

“It is likely to help with the housing market over the next ten years. So we can expect outperformance of the Brisbane housing market compared with other Australian cities over this time.

“It will also benefit over the short term from interstate migration inflows from Sydney and especially Melbourne, notwithstanding any future state border closures.”

Brisbane housing market forecasts

ANZ has tipped house prices to jump by 9 per cent next year in Brisbane before falling by 4 per cent in 2023 as the post-pandemic boom cools.

CBA now expects Brisbane house prices to increase by 9 per cent next year before plunging by 8 per cent in 2023 when the Reserve Bank ramps up interest rates.

NAB is forecasting Brisbane house prices to rise by 5 per cent over across 2022 as impact of low rates and strong income support begin to fade.

Westpac has also updated its property forecasts, with Brisbane real estate prices tipped to surge 10 per cent between 2022 before dialling back -1 per cent in 2023.

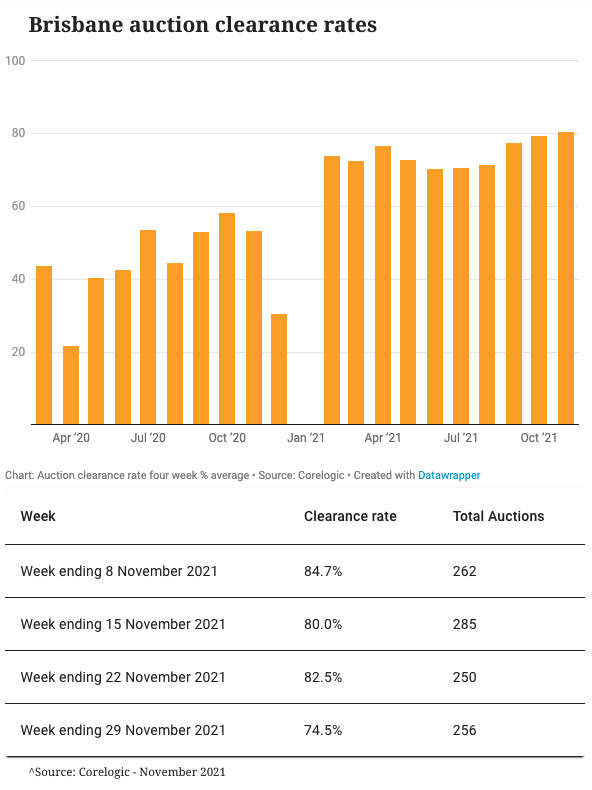

Brisbane’s auctions market is currently red-hot after the city escaped the worst of the pandemic disruption, drawing increased population from disenchanted southerners.

The market has moved from strength to strength and shows no sign of slowing down, remaining one of the few cities on an upward trajectory a year into the latest property boom and over November recorded a healthy clearance rate of 80.5 per cent across 1053 properties.

The city’s best performing suburbs—Norman Park, Indooroopilly and Camp Hill—have experienced median house price hikes of up to 36 per cent in the past 12 months and are amongst the most sought after on Domain and REA.

According to Domain, Norman Park—which topped its list for house price growth—saw the median climb 36.3 per cent to $1.24 million, with Indooroopilly collecting a 35.9 per cent lift to send the median house price to $1.277 million.

The fast-booming suburb of Camp Hill secured third place with a rise of 34 per cent, which sent the median house price to $1.2 million.

Different supply dynamics are also creating divergent trends across Australian capital cities and placing pressure on agents struggling to find stock.

Across November, the total stock available for sale across Brisbane was 33.9 per cent lower than the five-year average.

Comparatively, stock levels in Sydney and Melbourne have become far more normalised in recent weeks, with Sydney total listings sitting just 2.6 per cent below the five-year average, while stock levels across Melbourne are 7.9 per cent above the five-year average.

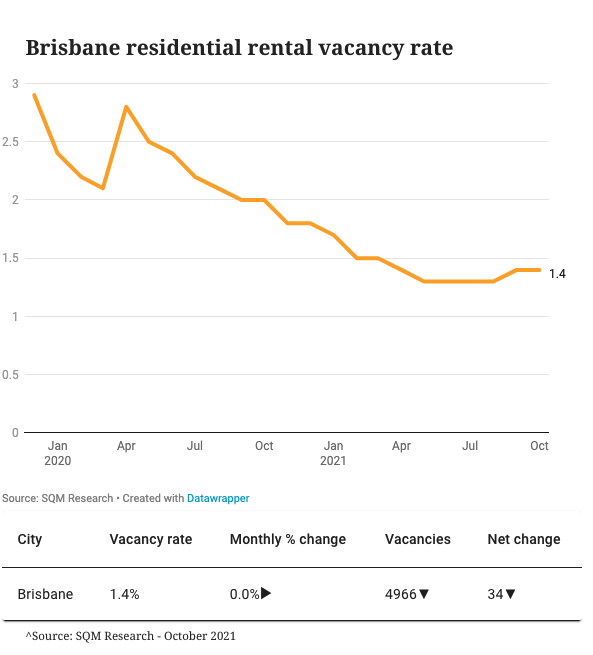

The national rental vacancy rate has now fallen to a 10 year low, of 1.6 per cent, as improving economic and health outlook prompts a rush of tenants to lease vacant rental properties.

Fewer properties are being left empty in Australia’s biggest rental markets, with vacancy rates falling or holding steady in each of the capital cities, new figures show.

Rising vacancy rates across the capitals have been brought to a halt, and are likely to fall further in the months ahead as the end of lockdowns and border restrictions near.

This should mean increased rental demand from returning Australians, international students and migrants.

Vacancy rates halted their upward climb in the locked-down cities of Melbourne and Canberra, falling slightly while the rate continued to track sideways in Brisbane.

The vacancy rate in the Brisbane CBD has dropped by 20 basis points so far this year to now be 8.4 per cent.

Since the onset of the pandemic, capital city house rents surged 10.1 per cent, while unit rents stayed 0.3 per cent below pre-Covid-19 levels.

Brisbane’s relatively low impact from the pandemic has meant that house rents have risen for five consecutive quarters—consistent growth not experienced since 2007.

Mount Ommaney has been the city’s top performing suburb after house rents there rose over the last year by $138 per week to now be $690.

Cornubia, Fig Tree Pocket and Seventeen Mile Rocks have all experienced similar rental increases, rising in that period by 19.9 per cent to $535, 17.2 per cent to $700 and 16.1 per cent to $560, respectively.

Bulimba is now the city’s most expensive suburb to rent a house after a 9.3 per cent annual hike sent weekly asking prices to $765 while Kenmore Hills is a close second after prices rose 7.6 per cent to $710.

House rents in South Brisbane suffered an annual 8 per cent drop to $460 while Grange house rents, in the city’s north, also took a dive of 7.6 per cent to $550, with Manly in the bayside south suffering a slump of 5.1 per cent to bring house rents to $490.

For the apartment market, the worst-performing suburbs were Sunnybank and Macgregor, which suffered price drops of 5.1 and 4.8 per cent to bring weekly rents to $370 and $400, respectively.

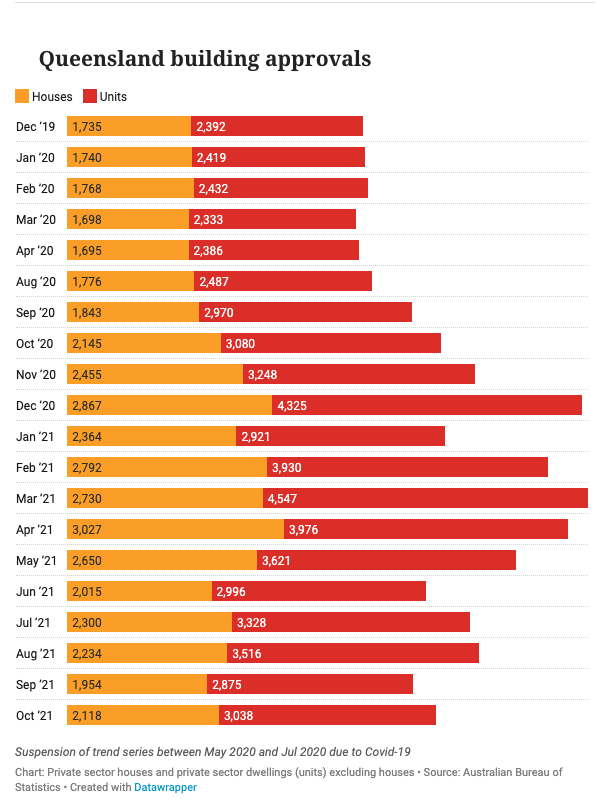

Australia’s new home building boom is set to continue next year, with about 190,000 homes—including 121,000 houses—tipped to be built nationally.

Approximately 25,000 new houses and 18,000 units will be constructed in Queensland next year, according to the Housing Industry Association.

Brisbane’s house building construction costs increased 7.4 per cent in the past year, and remains one of the most expensive regions to build in the country behind Hobart, Adelaide and Melbourne.

The price of timber has lifted by 12.4 per cent over the year in Brisbane, 31.7 per cent for steel, 7.3 per cent for plumbing products, 2.3 per cent for electrical equipment and has reduced by -2 per cent for concrete.

In order to raise a 20 per cent deposit, the typical Brisbane house buyer now needs around $140,000 and unit buyer $79,000.

In Queensland, the average figure for a loan for buying a newly built home is $461,000 and $489,000 for a loan to build a new home.

The average monthly repayments for an existing home is currently $2075, $1980 for a newly built home and $2100 for a new construction.

In September, the Reserve Bank governor, Phil Lowe, ruled out using interest rates “to cool the property market”, meaning low rates were likely to stay until 2024.

Lowe said the cash rate would stay on hold until “actual inflation is sustainably within the 2–3 per cent target range”, likely not until 2024 due to low wage growth despite a tightening labour market.

Lowe acknowledged that young people were “paying a heavy price” during the Covid pandemic due to lockdowns and public health measures, citing increasing incidence of mental health issues and calls to support services.

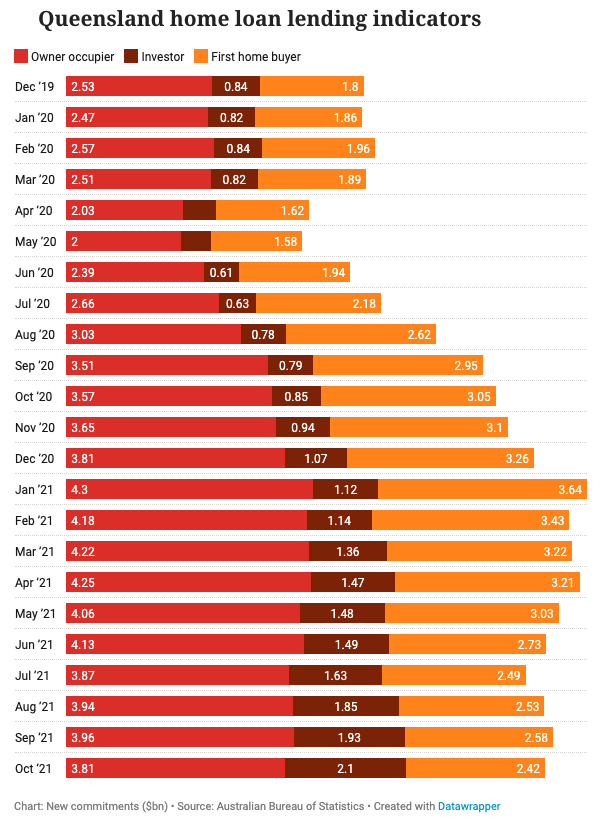

The latest ANZ-Property Council quarterly survey shows industry players expect a tightening in credit conditions over the next 12 months.

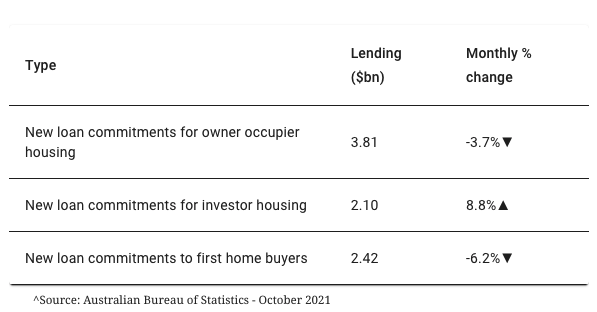

New lending finance to owner-occupiers has already peaked while first home buyer finance has been trending down since its peak in January. Home lending to other owner-occupiers has fallen 10 per cent over the past two months.

Growth in investor lending is positive after more than doubling in the year to May.

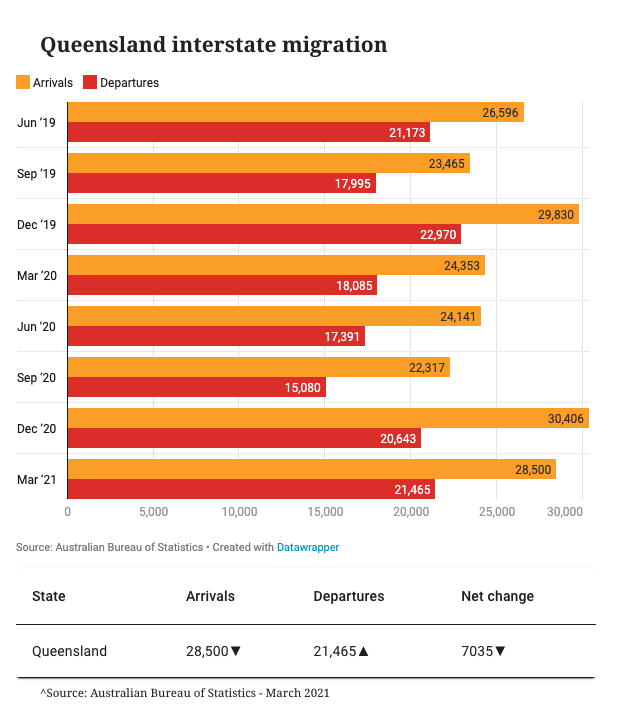

Interstate migration into Queensland, growing at its fastest rate since late 2003, has remained a tailwind for housing demand.

Brisbane’s population grew by 1.9 per cent during 2019-20, recording the highest growth rate of all capital cities, according to Australian Bureau of Statistics data.

Queensland experienced a net gain of 28,500 people from interstate in the March quarter and 21,465 departures.

Queensland’s population is expected to surge by more than a quarter of a million people in the next four years according to forecasts in the federal budget, as people flood in from other states.

Treasury boffins have predicted Queensland is set to gain around 20,000 people from interstate each year for the next four years—amounting to almost 85,000 new residents by mid-2025.

Next year alone, federal treasury estimates see Queensland gaining 23,800 new interstate residents, while Victoria is set to lose 1200 and New South Wales is tipped to shed as many as 15,500.

With a population of roughly 3.7 million, Queensland’s southeast is Australia’s fastest-growing zone.

Queensland’s population is predicted to hit 5.44 million by mid-2025, up from 5.17 million as of June 2020.

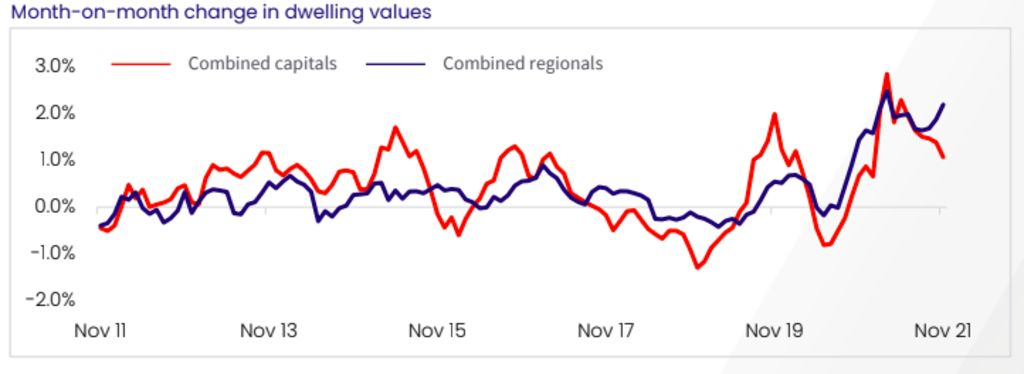

Australia’s pandemic property boom continues its upwards trajectory, with the latest figures revealing housing values rose in November for the 14th month in a row.

Property values have climbed more than 20 per cent over the year nationally, adding approximately $126,700 to the median value of an Australian home.

But the market is losing steam. Although housing values continued to rise in November – nationally, they’re up by 1.3 per cent – the November result was the softest outcome since January, CoreLogic’s latest national home value index revealed.

Across Sydney and Melbourne, conditions have slowed sharply with the sudden rise in new listings and affordability pressures taking their toll.

Sydney housing values rose 0.9 per cent over the month, while Melbourne by 0.6 per cent – a far cry from the massive rises in March this year when prices soared by 3.7 per cent in Sydney and 2.4 per cent in Melbourne.

CoreLogic research director Tim Lawless said the slowdown in the pace of growth was due to a number of reasons.

“Virtually every factor that has driven housing values higher has lost some potency over recent months. Fixed mortgage rates are rising, higher listings are taking some urgency away from buyers, affordability has become a more substantial barrier to entry and credit is less available,” he said.

But the boom was far from over, Mr Lawless said.

“The heat’s come out of the market but it’s still a hot market,” he said. “The boom isn’t over. Even in Melbourne and Sydney, where it’s slowed, you’re still seeing values rise 1 per cent in a month.

“Even though the market has slowed, the rate is still well above average. If you’re looking at the marketplace in Sydney, that 1 per cent [rise] is still nearly a $10,000 increase in a month.”

The fastest-growing property markets in Australia are now in Brisbane and Adelaide, where housing values are rising rapidly. They are the only capital cities yet to experience a slowdown.

Brisbane’s home values hit a cyclical high, rising by 2.9 per cent in November. That’s the fastest rate of growth for the river city in 18 years, adding $18,500 to the cost of a property in just one month.

Adelaide values rose 2.5 per cent, which equates to a rise of $13,500 – the highest rise since February 1993.

“Relative to the larger cities, housing affordability [in Brisbane and Adelaide] is less pressing – there have been fewer disruptions from COVID lockdowns and a positive rate of interstate migration is fuelling housing demand,” Mr Lawless said.

“On the other hand, Sydney and Melbourne have seen demand more heavily impacted by affordability pressures and negative migration from both an interstate and overseas perspective.”

Different supply dynamics are also creating divergent trends across Australian capital cities. In the four weeks to November 28, the total stock available for sale across Adelaide was 32 per cent lower than the five-year average, and 33.9 per cent lower across Brisbane.Across Sydney and Melbourne however, stock levels have become far more normalised in recent weeks, with Sydney total listings sitting just 2.6 per cent below the five-year average, while stock levels across Melbourne are 7.9 per cent above the five-year average.

Mr Lawless said he expected new listings would continue to rise into the new year, which would be a key factor driving the slowdown in capital growth.

“It’s no surprise that those cities where stock levels are starting to rise faster, buyers are getting more leverage and getting more choice,” he said.

Houses have continued to outperform units, with capital city values up 1.2 per cent and 0.7 per cent respectively over the month.

Based on median values, capital city houses are now 37.9 per cent more expensive than capital city units – the largest difference on record. In dollar value terms, a capital city house is averaging approximately $240,500 more than a capital city unit. In Sydney, where the gap between house and unit values is the widest, a house costs $523,000 more on average than a unit.

“With such a large value gap between the broad housing types, it’s no wonder we are seeing demand gradually transition towards higher density housing options simply because they are substantially more affordable than buying a house,” Mr Lawless said.

Heading into 2022, Australia’s property markets would continue to rise, albeit at a milder rate, he said.

“The market still has somewhere to go before prices start falling. The cue for the market to go down is when rate rises happen,” Mr Lawless said.

“My guess is through 2022, the rate of growth will gradually ease off but prices will probably still rise.

“Importantly, there’s going to be more diversity in the results. It’s not going to be every market recording double-digit annual growth – that will be the exception to the rule.”

The average price of a residential property in Australia is nearing the $1-million mark for the first time on record, with house hunters spending about $350,000 more than they did a year ago on the typical home.

According to Domain, Australian house prices have experienced the fastest annual rate of growth on record at 21.9 per cent with house prices rising three times faster than units over the past year.

Over the three months to September, all capital cities except for Perth and Darwin hit record highs for house prices with Canberra now the second most expensive capital city to purchase a house for the first time since 2005.

Sydney, the nation’s most expensive city, hit a new record of almost $1.5 million for houses after surging 30.4 per cent—rising by roughly $6700 a week over the past 12 months.

Unit prices hit a new record high of $802,475 after gaining $18,695 over the September quarter, surpassing the mid-2017 price peak for the first time.

NSW now accounts for $3.3 trillion, or 40 per cent, of the total Australian residential real estate market.

House price change by capital city

Melbourne, despite being in lockdown for most of the quarter, hit a new record high of $1.038 million after increasing by 16.8 per cent in the past year—the city’s strongest annual gain in 11 years.

The number of homes selling in Brisbane continues to surpass previous records to now be at its highest point in six years with listed homes for sale 7 per cent higher over the first three weeks of October compared to the two-year average.

House prices have now reached a new record high, surpassing the $700,000 mark.

Meanwhile, Hobart house prices have almost doubled over the past five years, the steepest increase of the capital cities.

Powell said price relief was now nearing as the rate of house price growth across capital cities halved in the September quarter compared to the previous quarter, suggesting the peak pace of growth has passed.

“We’re seeing the property market begin to cool down with soaring house prices in the last year adding to ongoing affordability pressures affecting buyers participation in the market,” she said.

“As Covid-19 lockdowns and restrictions come to an end and the sustained high prices appeal to vendors, sellers are beginning to re-engage with the market, increasing supply which in turn offer greater choices for buyers.”

The Reserve Bank of Australia recently acknowledged the hot housing market in its monthly board meeting minutes, and said policymakers needed to keep a close eye on lending standards.

It noted there had been an increase in loans with high debt-to-income ratios, and sustained growth in housing credit added to the risks of high household debt.

Housing credit growth is forecast to top 10 per cent on a six-month annualised basis early next year.

At the same time, wages growth is running at just 1.7 per cent, according to the latest Bureau of Statistics data.

“There has been an increase in the average loan value over the last year indicating that customers are borrowing more to keep up with rising prices and further driving house price growth,” Powell said.

“This may start to slow down as new serviceability measures are implemented from November 1.

“However, the sheer affordability of keeping up with rapid house price gains is proving a barrier for many buyers, especially first home buyers facing spiralling deposit goals and poor interest accrued on savings.

“Upsizing is also becoming a financial leap despite the benefit of strong equity growth, and particularly challenging if sold prior to purchasing.”

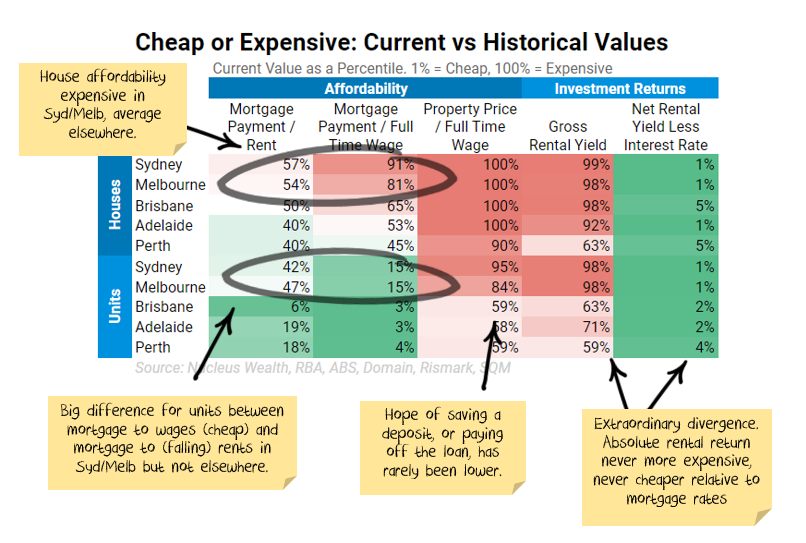

Australian property market prices continued to climb over the last month, with the past six months seeing some of the strongest growth on record. Mortgage fixed interest rates rose slightly, standard variable rates fell slightly but remain significantly above fixed rates. There are some extraordinary divergences in affordability. It has never been cheaper in some markets to service a mortgage, but never more expensive to save for a deposit or pay off the loan.

In general, housing valuation and affordability statistics worsened over August. For investors, rental yields have never been lower in an absolute sense, never higher relative to mortgage rates.

Regulatory actions in the background are worth watching. We are not expecting rising interest rates, but markets are starting to price them in. Last week the Reserve Bank of Australia had to intervene to keep interest rates in their desired range. We note even without official interest rate rises, bank funding costs will rise due to other regulatory changes. It is likely this will flow through to higher interest rates even with no official rate rises.

The Federal Government and Reserve Bank have successfully distorted conditions to encourage as many people as possible to borrow as much as possible. An investment in housing is basically a vote of confidence in their ability to keep force-feeding the market.

We run an Australian property market calculator to help investors or potential homeowners determine the returns on Australian property. The idea we want to illustrate is that there are a number of key inputs into housing valuation. Interest rates are the most important, but the other limiting factors are:

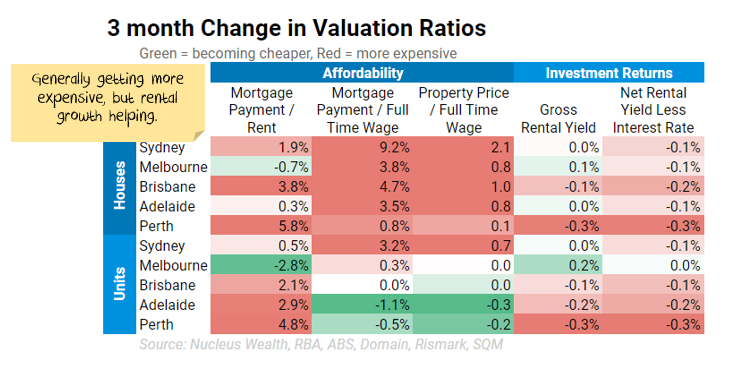

Mortgage Payments to Rent: comparing the cost of a mortgage with the cost of renting the same house. Using this ratio to constrain house prices, we assume that people will prefer to rent when the ratio gets high rather than buy.

Mortgage Payments to Wages: assuming when the ratio gets high, people rent because they cannot afford to buy.

Property Prices to Wages: assuming when the ratio gets high, people rent because they cannot save enough money to afford a deposit. We treat this as less important than the above two ratios.

Rental Yield: Rental yield is the annual rent divided by the property price. By using this ratio to forecast prices, you are assuming when the ratio gets low investors will not buy property as they are not getting a return that is high enough.

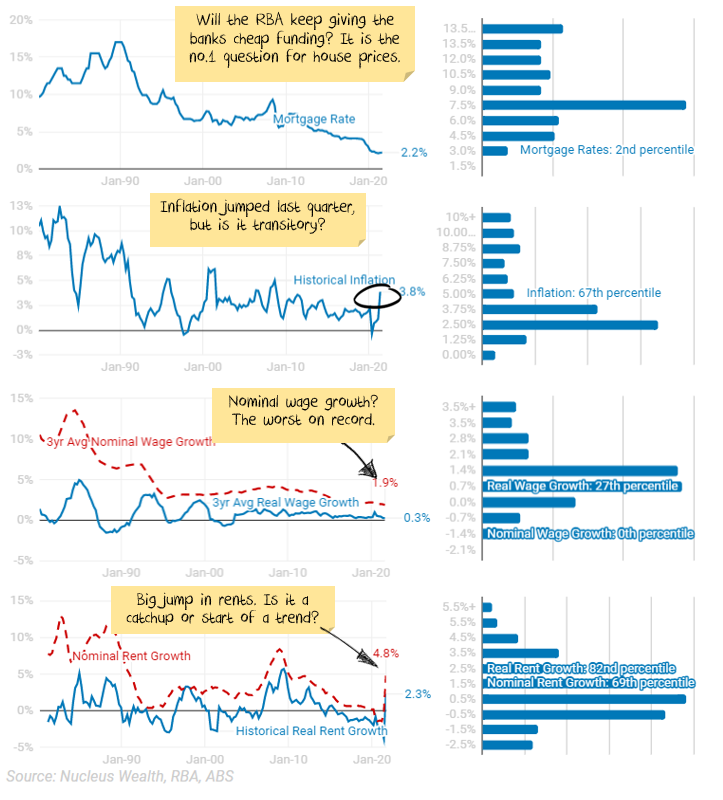

Australian mortgage rates can go lower but look like rising first.

There are effectively two different interest rates at the moment, the floating rate and the three-year fixed rate.

The floating rate is determined mainly based on the Reserve Bank of Australia. It reduced the floating rate to 0.1% in March 2020, which reduced the standard variable rate from banks to around 4.5%. This is unlikely to change.

In March 2020, the Reserve Bank also introduced a facility where they lent directly to the banks at 0.1% for three years. This facility (and other market interventions) allowed banks to drop three-year fixed mortgages to around 2%. Its name is the Term Funding Facility. It ended at the end of June.

When you adjust the factors in our property market calculator, you find that with low inflation, wage growth and rent growth that interest rates become even more important for determining property prices. But forget about the cash rate. The important factor is three-year fixed interest rate. This has risen very marginally. It seems likely the three-year rate will continue to rise unless we see further government or Reserve Bank intervention.

The short/medium term supply myth

Don’t get me wrong. The number of houses that get built matters eventually. But, in the short and medium term, affordability matters more.

The reason is that the stock of houses dwarfs the year to year supply numbers:

Each year Australia builds 100,000-200,000 dwellings

There are about 11m houses

11% are unoccupied (i.e. second homes, holiday homes, unleased properties etc)

At last census, there were 2.6 people per occupied dwelling

Do you want to absorb 350,000 new dwellings? Fewer flatmates per house, more young adults moving out. It doesn’t even show up in the rounded ratio of 2.6! Officially the number of people per occupied dwelling was 2.64. Change that to 2.55 and there are 350,000 new homes occupied.

How about another 150,000 new dwellings? Same trick with the rounded unoccupied rate of 11%. Change it from 10.5% to 11.4%.

Net effect: you could spend three or four years building another 500,000 dwellings, the population could stay the same, every new home could be bought and there would still be 2.6 people per house and 11% unoccupied.

I’m not arguing that supply doesn’t matter. It does. But over five year periods, affordability plays a far larger role.

Australian mortgage rates can go lower but look like rising first.

There are effectively two different interest rates at the moment, the floating rate and the three-year fixed rate.

The floating rate is determined mainly based on the Reserve Bank of Australia. It reduced the floating rate to 0.1% in March 2020, which reduced the standard variable rate from banks to around 4.5%. This is unlikely to change.

In March 2020, the Reserve Bank also introduced a facility where they lent directly to the banks at 0.1% for three years. This facility (and other market interventions) allowed banks to drop three-year fixed mortgages to around 2%. Its name is the Term Funding Facility. It ended at the end of June.

When you adjust the factors in our property market calculator, you find that with low inflation, wage growth and rent growth that interest rates become even more important for determining property prices. But forget about the cash rate. The important factor is three-year fixed interest rate. This has risen very marginally. It seems likely the three-year rate will continue to rise unless we see further government or Reserve Bank intervention.

The short/medium term supply myth

Don’t get me wrong. The number of houses that get built matters eventually. But, in the short and medium term, affordability matters more.

The reason is that the stock of houses dwarfs the year to year supply numbers:

Each year Australia builds 100,000-200,000 dwellings

There are about 11m houses

11% are unoccupied (i.e. second homes, holiday homes, unleased properties etc)

At last census, there were 2.6 people per occupied dwelling

Do you want to absorb 350,000 new dwellings? Fewer flatmates per house, more young adults moving out. It doesn’t even show up in the rounded ratio of 2.6! Officially the number of people per occupied dwelling was 2.64. Change that to 2.55 and there are 350,000 new homes occupied.

How about another 150,000 new dwellings? Same trick with the rounded unoccupied rate of 11%. Change it from 10.5% to 11.4%.

Net effect: you could spend three or four years building another 500,000 dwellings, the population could stay the same, every new home could be bought and there would still be 2.6 people per house and 11% unoccupied.

I’m not arguing that supply doesn’t matter. It does. But over five year periods, affordability plays a far larger role.

Australian Property Market Outlook

Property prices have been ripping higher in recent months. This has dented a number of affordability measures, but ongoing conditions appear as positive as they have been for some time.

On the one hand, plummeting immigration, pandemic disruptions and the end of eviction/mortgage payment moratoriums aren’t helping. A boost in supply is in progress, spurred by new home building. Rental growth jumped this quarter, but the last few years have been very weak. And Australia starts with a larger private debt burden than just about any other country. On the other, we have a burning political desire to keep Australian property market prices high and pump more debt into the economy. Wage growth is low, meaning interest rates can stay lower for longer. We have a roadmap to much lower interest rates to help. There is a structurally higher demand for houses vs units due to the fear of more lockdowns.

Australia is stuck in a debt trap. We’ve got so much debt we can’t raise rates because it makes it more difficult for people to pay back debt. To get more growth we have to cut rates, so people borrow more and the cycle goes on. In the meantime, there are other ways to keep the property party going. Once mortgages were for 20 years, then 25, now 30. Soon it will be 50. Japan has 100 year mortgages. Many people will never pay their mortgage back, so owning a home might become like renting – just that it’s renting from the bank.

Sources:

Nucleus Wealth has compiled this data using a range of different sources. We use Domain for more recent data quarterly property prices and rents, cross-checked with SQM to fill any short-term moves. Older information is from Rismark and the Australian Bureau of Statistics to fill time series. For economic data, we use either Reserve Bank of Australia or Australia Bureau of Statistics data. For older data, we have had to estimate some factors due to differing definitions over time.

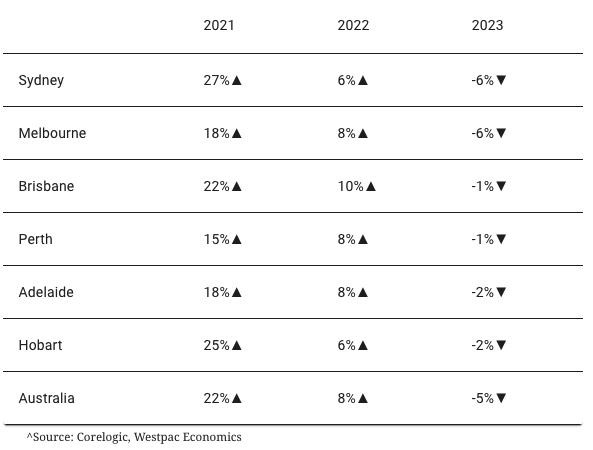

Westpac has upgraded its housing market forecasts, tipping house prices to lift by a further 5 per cent in the remaining three months of 2021 to be up 22 per cent for the year.

Prices in the major capital cities are already up 17 per cent for the year to September and are tracking for a 1.5 per cent gain in October.

Westpac expects Sydney home prices to lift by 27 per cent for this year, well above its previous forecast in August of 22 per cent, before lifting again next year by 6 per cent.

Melbourne is also expected to surpass its previous forecast by 2 per cent to be up 18 per cent for the year.

Brisbane’s house prices, already up 19.9 per cent over the last ten months, still has a further 2 per cent to grow before the close of the year, before picking up again by 10 per cent in 2022.

Nationally, prices are forecast to lift again next year, with Westpac revising its earlier call of 5 per cent to 8 per cent.

The bank expects most of 2022’s increase to be weighted in the first half of the year before moderating.

When are Australian house prices expected to drop?

Westpac chief economist Bill Evans said the bank was preparing for the market to move into a correction phase in early 2023 as higher interest rates, stretched affordability and the tightening of macro-prudential policies take hold.

“While the market upturn has weathered the latest Covid disruptions very well and is clearly carrying strong momentum, the boom is entering trickier territory,” Evans said.

“Price momentum has held up near term, prompting us to revise up the near-term outlook for prices.

“However, affordability is becoming stretched and policy tightening is now in play.”

Dwelling price forecasts

Westpac was the first major bank to tip rate rises ahead of the Reserve Bank’s current 2024 guidance, with Evans forecasting the first increase above the current historically low 0.1 per cent in early March 2023. Other economists are preparing for the RBA to begin raising rates over 2023 and 2024 to a natural rate of about 1.25 per cent. Westpac estimates rates any higher would place “significant stress” on household finances. “We still expect the market to slow over the course of 2022 as macro-prudential policy; prospects of increased rates; and affordability reaching record lows triggers a correction phase that will begin in 2023 and is likely to extend into 2024,” Evans said. “The combination of high levels of new building and slow population-driven demand may also weigh on some sub-markets.” Corelogic research director Tim Lawless said the slowing growth conditions were the result of higher barriers to entry for non-home owners along with fewer government incentives to enter the market. “With housing values rising substantially faster than household incomes, raising a deposit has become more challenging for most cohorts of the market, especially first home buyers,” Lawless said. “Existing home owners looking to upgrade, downsize or move home may be less impacted as they have had the benefit of equity that has accrued as housing values surged.” Housing credit has been growing at an annualised pace of about 7 per cent in recent months, more than double the rate of income growth. According to data from the Australian Prudential Regulation Authority, the number of new mortgage loans where debt is at least six times greater than income lifted by 6 per cent in the June quarter.

A housing affordability crisis could see thousands of Queenslanders displaced as an investor incentive scheme expires.

The National Rental Affordability Scheme, which has run for 10 years, was set up to give investors incentive to keep their properties affordable.

But as the offer expires, there’s potential for more than 9500 properties to see a rent hike.

Everybody’s Home spokesperson Kate Colvin told Sofie Formica rent was already ‘sky high’ in Brisbane, rising 14 per cent in one year.

“What perhaps wasn’t known at the time was we were going to have COVID crisis, which would send even more people north to sunny Queensland.

“The rental crisis in Queensland is even worse than before and having these incentives expiring on top of that situation is just going to make it really impossible.”

She says there needs to be more support to alleviate the issue at a Commonwealth level.

“The Queensland government are already putting a big investment into affordable housing.

“We need the federal government to step up and make their contribution.”

Home values are still rising at their fastest pace in more than 30 years despite lockdowns in Australia’s two biggest cities and the foot coming off the pedal over the past six months.

They jumped another 1.5 per cent in September, bringing the total increase for the first nine months of the year to 17.6 per cent, according to Corelogic.

Nationally, home values have soared by 20.3 per cent over the past 12 months to a median of $676,848, which is up $8334 from last month.

The annual growth rate is now tracking at its fastest pace since the year ending June 1989.

But while the market conditions remain positive, the monthly growth rate is continuing to lose steam and ease back from its peak of 2.8 per cent in March.

Corelogic research director Tim Lawless said worsening affordability—with increasingly higher barriers to entry for non-homeowners and fewer government incentives—was slowly putting the brakes on growth rates.

“With housing values rising substantially faster than household incomes, raising a deposit has become more challenging for most cohorts of the market, especially first home buyers,” he

said.

Lawless said a prime example was Sydney, where the median house value at just over $1.3 million now means the typical buyer needs around $262,300 for a 20 per cent deposit.

“The slowdown in first home buyers can be seen in the lending data, where the number of owner-occupier first home buyer loans has fallen by -20.5 per cent between January and July,” he said.

“Over the same period, the number of first home buyers taking out an investment housing loan has increased, albeit from a low base, by 45%, suggesting more first home buyers are choosing to ‘rent vest’ as a way of getting their foot in the door.”

Corlelogic’s research indicates the monthly change in house values remains positive across all capital cities with Hobart (2.3 per cent) and Canberra (2 per cent) notching up the largest growth, while Darwin (0.1 per cent) and Perth (0.3 per cent) recorded the softest growth.

Generally, house values are still rising faster than unit values with the exception of Hobart and Darwin, where unit values have risen 5.4 percentage points and 4.8 percentage points more than house values, respectively, during the past 12 months.

Across regional Australia, however, unit values rose faster than house values in the September quarter.

“This is probably a reflection of stronger demand for downsizing options and holiday homes in popular coastal markets,” Lawless said.

AMP Capital chief economist Shane Oliver said ultra-low mortgage rates, an ongoing relatively low level of homes for sale along with a resumption of economic and jobs market recovery once lockdowns end, pointed to further home price increases ahead, albeit at a slowing rate.

“A surge in listings once lockdowns end could act as a bit of a dampener on price growth,” he said. “But this looks to be more of an issue in Melbourne where listings have fallen sharply in recent weeks and where economic uncertainty is greater, but less so in Sydney where listings have already been increasing.”

▲ A new entry canopy to the hospital and a seven-storey acute services building are part of the redevelopment of the John Hunter Health Innovation Precinct.

▲ A new entry canopy to the hospital and a seven-storey acute services building are part of the redevelopment of the John Hunter Health Innovation Precinct.