Property boom tipped to continue into 2022

Property prices are likely to keep roaring higher into further record territory next year, as the Australian economy’s stronger-than-expected recovery continues.

And there is a good chance that they could continue to climb after that, market experts say, albeit prices could start to moderate and even return to their long-term percentage annual growth rates of low, single digits.

Louis Christopher, founder of SQM Research, says there are more property buyers than sellers and with the Reserve Bank of Australia re-affirming interest rates are likely to stay low for a long time, the evidence “suggests the market is going to continue to go up from here; particularly for free-standing houses”.

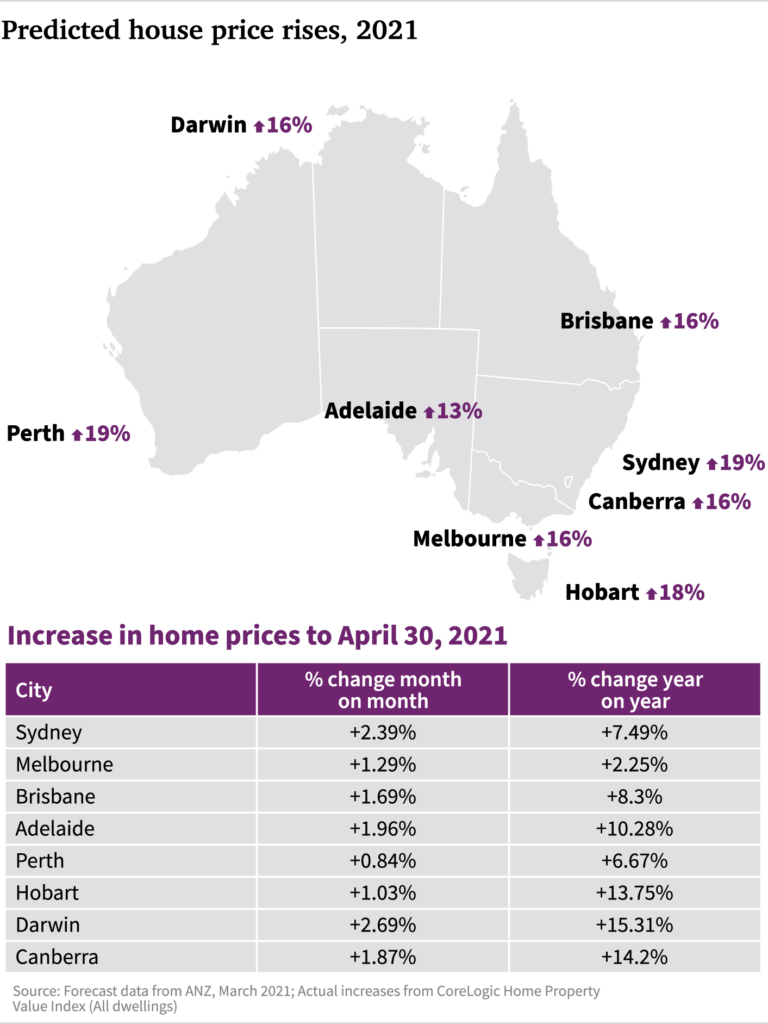

He estimates the price of free-standing properties in Sydney are up close to 20 per cent in the past year, with similar properties in Melbourne up between 12 per cent and 14 per cent.

“It’s a strong [cities] market and it is also strong in the regions, particularly along the east coast [of Australia],” he says.

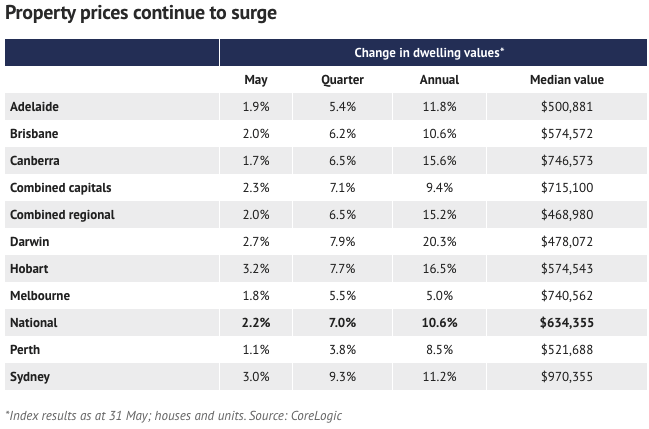

After price rises slowed during April of this year, many property market watchers thought that growth would continue to moderate. However, capital city dwelling prices defied expectations and jumped again in May.

Prices in regional areas also climbed, likely driven by those working from home in the wake of the coronavirus pandemic who are seeking a lifestyle change and cheaper housing.

Figures from researcher CoreLogic show dwelling prices in Sydney climbed 3 per cent in May and 11.2 per cent over the 12 months. In Melbourne, prices jumped 1.8 per cent in May and are up 5 per cent for the full year.

Angie Zigomanis, director of Charter Keck Cramer’s research and strategy team, says prices in Sydney and Melbourne could rise by another 10 per cent over the next 12 months.

However, he would not be surprised if it was more like 5 per cent to 7 per cent, given there are so many factors at play; the most obvious being the impact of COVID-19.

Zigomanis forecasts that prices would remain robust for at least 12 months before moderating. He says with Melbourne’s economy traditionally highly dependent on migration growth – not only overseas immigration but also people relocating from other states – the closure of international borders would likely continue to see smaller price rises than in Sydney.

Melbourne’s central-city apartment market is likely to continue to be particularly challenged.

Figures from SQM Research show that although inner-city apartment rental vacancy rates have dipped from their record highs of last year, they remain elevated by historic levels.

SQM Research’s Christopher says the return of property investors to the market could signal that we are now nearer the end of the price-rise cycle than the start.

Usually, price-growth cycles start with first-home buyers, then upgraders join in and, finally, investors come into the market, attracted by the prospects of capital gains, Christopher says.

There is another factor that could help dampen price rises, Christopher says. The Australian Prudential Regulation Authority could “tap the brakes” on home lending, by putting restrictions on lenders. It did that in 2015, continuing the policy until prices peaked in 2017.

Shane Oliver, chief economist at AMP Capital, expects property prices to keep rising until 2023, when we could see the start of another cyclical downturn as interest rates move up more decisively.

Lenders are already starting to increase their 2 and 3 year fixed mortgage interest rates, after earlier increasing their 4 and 5 year fixed rates.

Steve Mickenbecker, Canstar’s group executive financial services, says variable mortgage interest rates are holding firm, but rising fixed rates are a sign that the interest-rate cycle is turning.