PRIME MINISTER SCOTT MORRISON HAS THROWN HIS SUPPORT BEHIND THE ESTABLISHMENT OF A CONTAINER TERMINAL IN THE PORT OF NEWCASTLE.

It is estimated the proposed container terminal would attract $1.8 billion of private investment and generate more than 15,000 direct and indirect jobs and contribute $2.5 billion to the national economy.

Mr Morrision indicated on Thursday that he would allow the Australian Competition and Consumer Commission’s Federal Court action against the NSW Ports consortium and the state government to run its course, however, he ultimately wanted the container terminal issue to be resolved.

“I want to ensure that Newcastle can deliver all of the services that this region needs for it to be successful,” he said.

“There are some processes underway that are addressing those issues….Let me be very clear about the outcome I want to see, whether it’s the port in Newcastle or the port in Townsville or Gladstone, I want these ports be able to service the regions as fully and as competitively as is possible.

“As the Prime Minister I know what’s needed here and that’s a Port of Newcastle that works for the Hunter because when that happens the Hunter is able to do more for Australia.”

Mr Morrison is meeting with representatives from the Port of Newcastle on Thursday afternoon.

Australia’s potential property buyers are facing a “perfect storm” of economic factors that are driving prices up at the fastest rate in almost two decades.Yesterday property research firm CoreLogic revealed that in just one month home values surged 2.1 per cent – the highest single-month increase since 2003.Sellers are being swamped with offers, banks are welcoming new customers through the doors and interest rates are at historic lows.

Steve Mickenbecker, Canstar Group’s executive of financial services, said demand for properties is reaching fever pitch.”It is the perfect storm for house prices. On the supply side, new listings through 2020 were well below the four preceding years and total listings now are also down as stock is absorbed before or as soon as properties hit the market,” Mr Mickenbecker said.”Owners are loath to put a house on the market even at high current prices, fearing they will miss the boat getting back in.”

If historic low cash rates and restricted supply weren’t enough, there’s also a human psychological quirk jamming its foot on the price accelerator: FOMO, or the fear of missing out.”Property demand has run way ahead, with the fear of missing out becoming a powerful psychological driver as government incentives and low interest rates have encouraged first home buyers and home builders into the market in a rush,” Mr Mickenbecker explains.If the growth of Aussie house prices continues at its current meteoric pace, we could see the Reserve Bank’s hand forced in lifting interest rates off their current level of 0.1 per cent.

“The Reserve Bank doesn’t expect to raise the cash rate for three years or more, but unless property prices can be slowed it will have to start looking for some way to apply the brakes,” Mr Mickenbecker said.”First home buyers and new construction are leading the charge for property buying rather than investors, so the Reserve Bank can’t enlist APRA to target investors with lending caps as it has done previously.”Graham Cooke, head of consumer research at Finder, predicts the current growth has legs: a panel of 40 experts and economists forecast the average property price to grow by 12 per cent on average over the next two years.

“With more than $120,000 set to be added to the value of the average Sydney home over the next two years, the brief period of ‘affordable’ prices appears to be ending,” Mr Cooke said.”ABS lists the median Aussie income at $49,805, so homeowners in the Harbour City will be earning 22 per cent more than the average income, just by living in their homes for two years.”Westpac economists Bill Evans and Matthew Hassan are even more bullish.They believe house prices will spike by a total of 20 per cent over 2021 and 2022.”We now expect dwelling prices to rise by 10 per cent nationally in 2021 with this pace continuing in 2022,” Mr Evans and Mr Hassan advised last week.”The upturn is being supported by record low interest rates; the confident expectation amongst borrowers that these rates will remain low for years to come; ample credit supply; and an improving economic backdrop, as the roll-out of vaccines promises to bring the pandemic to an end and drives a sustained lift in confidence.”

But all good things must come to an end, and Mr Mickenbecker believes “market forces” will eventually apply the brakes as renters moving into their first homes free up supply.”Market forces must eventually slow the pace of demand, but we are going to have to see an increase in property listings to get us to that point. Supply must come from investors who will be feeling the heat as first home buyers leave a further vacancy behind, but investors can walk away with a tidy capital gain and no pressing housing need,” Mr Mickenbecker said.”Buyers will be feeling a lot of pressure before this all plays out and the Reserve Bank will be looking for a circuit breaker.

Aussie home values have recorded their biggest monthly increase in 17 years, with many regional areas outpacing their capital city counterparts and regional Queensland was a star performer.

Regional Queensland’s dwelling price rises continue to outpace the capital, recording a 1.9 per cent rise over the past month and 9.2 per cent growth over 12 months.

The staggering figure, released in the CoreLogic Hedonic Home Value Index report this morning, shows home values nationally surged 2.1 per cent higher in February – the largest month-on-month increase in 17 years.

“Spurred on by a combination of record low mortgage rates, improving economic conditions, government incentives and low advertised supply levels, Australia’s housing market is in the midst of a broad-based boom,” the report said.

CoreLogic’s research director Tim Lawless said such a spectacular growth phase had not been seen in Australia in a decade – a remarkable outcome given the global COVID-19 pandemic.

“The last time we saw a sustained period where every capital city and rest of state region was rising in value was mid-2009 through to early 2010, as post-GFC stimulus fuelled buyer demand,” Mr Lawless said.

Back in Queensland, Brisbane recorded a 1.5 per cent increase in dwelling values in February, 3.5 per cent over the quarter and 5 per cent in 12 months..

In regional Queensland, dwelling values rose 1.9 per cent in February and 5 per cent over the quarter.

But where regional Queensland really shines is in the 12 month growth figures, with the regions recording a combined growth of 9.2 per cent compared to Brisbane’s 5 per cent.

The report shows all regions, with the exception of Western Australia, recorded growth over the past 12 months, led by regional Tasmania.

“Regional markets (up +2.1% over the month) have continued to show a higher rate of capital gain relative to the capital cities (up +2.0%), however the performance gap has narrowed compared with the earlier phase of the growth cycle,” the report said.

“Regional areas generally recorded less of a decline in housing values through the worst of the COVID period last year, while also showing an earlier and stronger growth trend through the second half of last year.

“This regional preference is reflected in the annual growth trend, where the combined regionals index is 9.4 per cent higher while the combined capital city index is up a much smaller 2.6 per cent.”

One of the key factors pushing up dwelling values is a lack of supply in the face of increased demand.

The report found that the number of properties advertised for sale was a historically low levels, and was 26.2 per cent below 2020 levels nationally over the 28 days to February 21.

The Aussie Buyers’ Opportunities Report, recently released by mortgage broker Aussie and CoreLogic, found that many regional Queensland areas were in the midst of a ‘great market squeeze’.

In Townsville, the report found that just 6.3 per cent of housing stock hit the market in 2020, but listing numbers were even tighter in some suburbs.

It was a similar story in Cairns, where just 7 per cent of stock was listed for sale.

“The most tightly held suburbs of regional Queensland were a mix of resource intensive locations and coastal regions within the Gold Coast and Sunshine Coast markets,” the report said.

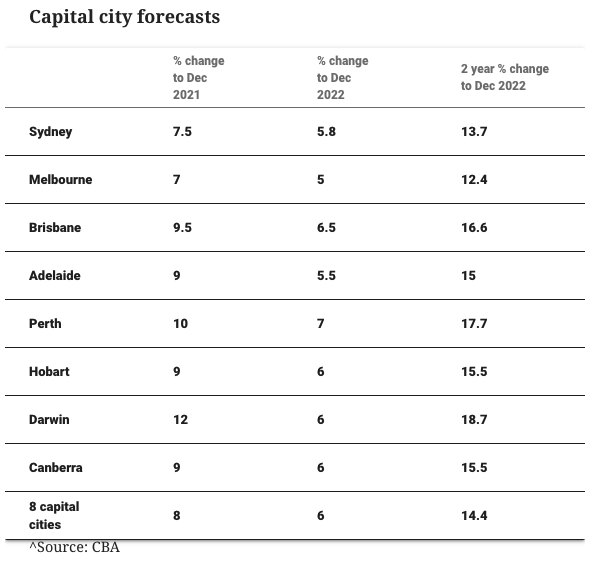

In a report released on Monday, Westpac’s chief economist, Bill Evans, said the bank has now lifted its forecasts to double-digit growth across the nation as momentum across the capital cities continues to swell until a predicted stall in 2023.

The economist stated that the Australian market as a whole is tipped to expand by 10 per cent in both 2021 and 2022.

Sydney dwellings prices are estimated to grow in line with Australia, while Melbourne is expected to rise by 8 per cent in 2021, followed by 10 per cent growth in 2022.

Brisbane (10 per cent over both years), Perth (12 per cent this year, 8 per cent in 2022), Adelaide (10 per cent, then 8 per cent) and Hobart (8 per cent, then 6 per cent) are also showing strong signs of growth over the next two years.

Westpac’s chief economist pointed to the high clearance rates across Sydney and Melbourne, declaring a “sellers market” until new listings become available.

“The upturn is being supported by record-low interest rates, the confident expectation among borrowers that these rates will remain low for years to come, ample credit supply and an improving economic backdrop, as the rollout of vaccines promises to bring the pandemic to an end and drives a sustained lift in confidence,” Mr Evans said.

While noting some of the strong activity relates to markets playing catch-up following the pandemic, Mr Evans pointed to high dwelling approvals and a rise in new lending across the final quarter, which he said demonstrated strong confidence in the current housing market.

“However, even allowing for this, the picture is unambiguously strong. Most tellingly, buyer demand has run well ahead of ‘on market’ supply, with sales outstripping new listings by 34 per cent over the last six months and ‘stock on market’ down to just 2.5 months of sales – the long run average is 3.8,” the economist said.

Mr Evans also pointed to strong gains in regions where the virus remained subdue over the coming months, before the pendulum swings back to Sydney, Melbourne and Brisbane in 2022.

“The upswing is also likely to see a rebalancing towards investors, particularly as affordability constraints re-emerge for owner-occupiers, including first home buyers,” Mr Evans explained.

Touching on the likelihood of a prolonged interest rate hold, Mr Evans noted that if the RBA is no longer prepared to continue committing to ‘three years on hold at 0.1 per cent’ rhetoric in 2022, Westpac’s analysis of their forecasts for inflation and wages suggests official guidance at that point will still be to expect rates to remain on hold for a number of years.

“This adjustment will increase fixed-term mortgage rates and may take some heat out of the market at the margin but is unlikely to derail what will be a very well-established price upturn by 2022,” he said.

Despite remaining bullish, the economist pointed to falling migration levels being a medium term headwind for the property market.

“If borders remain closed for longer or migration inflows are slow to restart, that could lead to a market-wide physical oversupply of dwellings by 2022. How that may influence market conditions and price growth is unclear,” he said.

“For example, rental vacancy rates may remain elevated for longer, perhaps even pushing higher, but that may not do much to deter investors seeking expected price gains, particularly as rental yields are likely to remain above funding costs.”

Property prices in Brisbane’s red-hot market might be soaring but it’s still cheaper to buy than rent in dozens of budget hotspots, with a new Domain report not only revealing where bargain hunters can nab a cheap home, but where a mortgage will set you back far less than a lease.

The rent vs buy data – which crunched the numbers on median rent and mortgage costs up to December last year – further revealed the city boasts far more feasible suburbs than its major southern counterparts, with buyers able to save up to $135 a week in some Brisbane fringe suburbs.

Using weekly mortgage repayments based on the median house or unit price for the suburb, the data is based on an assumed mortgage rate of 2.48 per cent and a deposit of 20 per cent, while excluding extra costs such as council rates and transfer duties.

Based on those calculations, suburbs in and around Logan came up trumps, with houses in Woodridge offering the widest gap between mortgage repayments and rent. In that patch, the average homeowner forks out a mere $165 per week in home loan repayments, compared to $300 for the average renter.

Next on the list was Waterford, where the weekly mortgage repayment for houses is $344, compared to a weekly rent of $410. Logan Reserve ranked third with house repayments averaging $342, compared to $400 for rent.

Domain senior research analyst Dr Nicola Powell said the data set revealed just how many suburbs within Greater Brisbane were cheaper to purchase in than rent, a fact she said was further fuelled by the historic low interest rates.

“This has really aided affordability (in Brisbane) but now it’s a question of how long it will last,” Dr Powell said.

“There comes a point where low mortgage rates do elevate prices, which offsets the benefits. Despite that, I don’t think it will be the last year we will see this, but we will likely see (more) price growth and what that will do is reduce the number of suburbs that have that mortgage/rent divide.”

Property prices in Brisbane’s red-hot market might be soaring but it’s still cheaper to buy than rent in dozens of budget hotspots, with a new Domain report not only revealing where bargain hunters can nab a cheap home, but where a mortgage will set you back far less than a lease.

The rent vs buy data – which crunched the numbers on median rent and mortgage costs up to December last year – further revealed the city boasts far more feasible suburbs than its major southern counterparts, with buyers able to save up to $135 a week in some Brisbane fringe suburbs.

Using weekly mortgage repayments based on the median house or unit price for the suburb, the data is based on an assumed mortgage rate of 2.48 per cent and a deposit of 20 per cent, while excluding extra costs such as council rates and transfer duties.

Based on those calculations, suburbs in and around Logan came up trumps, with houses in Woodridge offering the widest gap between mortgage repayments and rent. In that patch, the average homeowner forks out a mere $165 per week in home loan repayments, compared to $300 for the average renter.

Next on the list was Waterford, where the weekly mortgage repayment for houses is $344, compared to a weekly rent of $410. Logan Reserve ranked third with house repayments averaging $342, compared to $400 for rent.

Domain senior research analyst Dr Nicola Powell said the data set revealed just how many suburbs within Greater Brisbane were cheaper to purchase in than rent, a fact she said was further fuelled by the historic low interest rates.

HOUSES

Suburb

weekly repayment

Weekly Rent

Difference between buying and renting

Woodridge

$165

$300

-$135

Logan Reserve

$342

$400

-$58

Helensvale

$567

$623

-$56

Springfield Lakes

$361

$410

-$49

Centenary Heights

$309

$350

-$41

Alexandra Hills

$404

$440

-$36

Beenleigh

$313

$348

-$34

Bracken Ridge

$424

$450

-$26

Victoria Point

$448

$470

-$22

Mount Cotton

$461

$470

-$9

Strathpine

$382

$380

$2

Capalaba

$412

$410

$2

UNITS

Suburb

Region

weekly repayment

Weekly Rent

Difference between buying and renting

Marsden

Brisbane West

$210

$330

-$120

Eagleby

Bayside South

$181

$300

-$119

Upper Mount Gravatt

Brisbane West

$321

$430

-$109

Capalaba

Brisbane East

$305

$400

-$95

Bowen Hills

Brisbane North

$326

$413

-$87

Chermside

Brisbane North

$309

$390

-$81

Calamvale

Brisbane West

$321

$400

-$79

Richlands

Brisbane West

$296

$375

-$79

Stafford

Brisbane North

$294

$370

-$76

Spring Hill

Brisbane North

$331

$400

-$69

“This has really aided affordability (in Brisbane) but now it’s a question of how long it will last,” Dr Powell said.

“There comes a point where low mortgage rates do elevate prices, which offsets the benefits. Despite that, I don’t think it will be the last year we will see this, but we will likely see (more) price growth and what that will do is reduce the number of suburbs that have that mortgage/rent divide.”

Get the best property news and advice delivered straight to your inbox.

While the days of Brisbane’s bargain abodes might be numbered, Dr Powell said the data not only revealed the number of hotspots where first-home buyers could still snap up a house for less than $300,000, but where investors looking for a positively geared property could reap far more rent.

“It’s so valuable because it allows them to do that week-by-week comparison. It also shows the number of suburbs where there’s only a $30 or $40 difference,” she said.

Some of those suburbs where a mortgage is similar to the cost of rent are Springfield Lakes – where the weekly mortgage repayment for a house averages $361 compared to $410 for rent – Strathpine in Brisbane’s north and Capalaba in the east, where the difference is a meagre $2 for houses in favour of renters, Upper Kedron, where it costs $9 more for a mortgage per week than to rent a house, and Jindalee, where the average weekly mortgage is $511 for houses or $475 for the rental equivalent.

For units, Marsden boasted the widest gap with average mortgage repayments costing just $210 per week, compared to $330 for rent.

At the other end of the spectrum, the prestigious inner-city suburb of New Farm clocked the biggest discrepancy in both houses and units, with the average mortgage repayment for houses being $1360 compared to $673 for rent, and $577 for unit repayments compared to $415 for rent.

It couldn’t be more of a contrast in the Logan region, which offers some of the city’s cheapest buys. Sales executive at Ray White Logan City, Teza Fruzande, said houses sold for as low as $260,000 in Woodridge, a suburb that’s less than a 30-minute drive from the city centre.

And buyers, he said, are catching on.

“In the last two months we’ve been dealing with a lot of people from interstate who buy (investment properties here) sight unseen … but we are also seeing more owner occupiers (because of those cheap prices),” Mr Fruzande said.

“The thing they all mutually like is the location, as Woodridge is actually surrounded by all the good areas such as Springwood and Stretton – which is a million-dollar suburb. And they don’t even have good public transport in Stretton.”

But while Mr Fruzande said the suburb was an untapped gold mine for those looking to take their first steps on the property ladder or start an investment portfolio, he warned Woodridge wasn’t immune from the Brisbane property boom, with prices already rising.

Harcourts Connections Stafford sales representative Robbie Lofaro said first-home buyers were flocking in droves to Marsden, where the repayments on a mortgage were significantly less than paying rent, sparking a demographic shift in the suburb.

“It’s not going to be a fast transition but the sale of [the] housing commission homes is slowly happening,” Mr Lofaro said.

“And we’re also seeing more investors sell because I think prices have started to increase … and that’s providing opportunities for first-home buyers. They can buy a townhouse here for $260,000 and eventually rent it out for $320 or $340 per week.

“So while you’re dream home isn’t a townhouse in Marsden you can live there a year and then rent it out and start your property portfolio.”

It was that dream that inspired the then-22-year-old first-home buyer Selene Bruynzeels to snap up a three-bedroom townhouse in Marsden for $240,000 from Mr Lofaro in September last year. It costs her just $237 per week in repayments before the body corporate fees.

“I was looking in several areas such as in and around Logan purely because it was more affordable,” Ms Bruynzeels said.

“The bank wouldn’t let me borrow as much as I dreamed ($500,000) and they told me I’d only get $290,0000 as a first-home buyer on the scheme and it was a slap in the face … but then I purchased a townhouse that was only 10 years old.

“I plan to live in it for a year and then rent it out for about $330-$340 per week.”

Brisbane City Mortgage Choice managing director Matt Cunliffe said first-home buyers and upgraders were now flooding the market, having realised rent prices were higher than a mortgage in some parts.

“I think any time is a great time to buy if you’ve got the capacity to do, but at the moment it would seem in comparison to rental prices the story is the most compelling it’s been in a long time,” Mr Cunliffe said.

“We’re now seeing more upgraders and they are saying that they are going to miss the boat [if they don’t buy soon] because they’ll be priced out,” Mr Cunliffe said.

But while FOMO alone could drive up those property prices, he said it was a prime time for buyers to dive into the market thanks to the wealth of opportunities that still abounded.

“If you’re looking at a loan of about $400,000 … the rent will often be around $1700 a month while the mortgage would be sub-$1500 for the same property,” he said.

The CBA is forecasting a surge in house prices over the next two years of up to 16 per cent, while unit price-growth will be more muted at 9 per cent.

According to the CBA, lending rates have lifted sharply, signalling a housing market on the “cusp of a boom”.

“The increase in new lending is now feeding into higher prices for bricks and mortar,” CBA economist Gareth Aird said.

“The negative impact that Covid-19 had on Australian property prices turned out to be much more muted than almost any forecaster expected, us included.

“We were earlier than most, however, to recognise this and revised our call in September 2020 to look for a smaller peak-to-trough fall and a decent lift in prices over 2021.

“But even then, the rapid growth in new lending over the second half of 2020 was stronger than we anticipated.”

In its most recent economics issues report, released today, economists at the CBA reported the boom was off the back of record low interest rates and a v-shaped labour market recovery.

Aird said record low borrowing rates remained below rental yields across most markets and it meant property markets “would need to find equilibrium” in the form of dwelling price rises.

“A critical assumption underpinning our forecasts is the cash rate remaining at its record low of 0.1 per cent, which is in line with RBA forward guidance,” Aird said.

“We do, however, factor in a modest increase in fixed rate mortgages, which will rise if the RBA removes or raises its target yield on the three-year Australian Government bond, as we expect in the second half of 2021.”

The CBA is reporting positive momentum is building within the property market and “as the market firms, would-be buyers are more confident to purchase and this brings other buyers into the market”.

The news is less positive for unit-owners. CBA is forecasting a disparity in price growth between houses and apartments.

“We forecast national house prices to rise by 16 per cent over the next two years and unit prices to rise by 9 per cent,” Aird said.

Across the suburbs, they’re lining up for home inspections. With COVID-19 restrictions, only a handful are allowed in at a time. The queues, for units in particular, stretch down the stairwells and spill outside. In some regional areas, particularly coastal locales, the situation has reached fever pitch.

Regional prices rose 1.6 per cent in January, more than double that of the main capital cities.

Auction clearance rates are hurtling towards a perfect score in some cities.

Canberra recently clocked up clearances in excess of 90 per cent while Sydney has pushed way above 80 per cent; rates that indicate extremely tight conditions.

When Corelogic tallied the final numbers on Friday, the previous weekend’s national auction clearance rate hit a six-year high at 79.3 per cent.

The preliminary results from Saturday indicate an even stronger performance at more than 86 per cent.

With interest rates locked in at a whisker above zero — and with Reserve Bank assurances they’ll stay put for the next four years — it’s little wonder buyers are scrambling for a piece of the action.

Add in the imminent removal of responsible lending laws and the stage is set for a sustained real estate boom.

Even accounting for the hyperbole usually employed by the industry, this note dropped into your diarist’s inbox over the weekend from a local agent summed it all up.

“In my 25 years of working in the industry, conditions have never been stronger.”

Nothing to see here

In ordinary circumstances, we’d be at the point where a rational Reserve Bank governor would be expressing concerns, perhaps even warning would-be home buyers that prices don’t always rise, and that caution is warranted in such a frenzied environment.

Behind the scenes, you’d expect contingency plans being formulated on how to deflate the real estate bubble without hurting the broader economy.

Not this time. Instead, our monetary mandarins are doing the opposite. They’re stepping aside, more than happy to let prices rip.

“There’s a lot of focus at the moment on the fact that housing prices are rising again, and the stock market has been strong,” RBA Governor Philip Lowe said recently.

“Well, the national house price index today is where it was four years ago … and the equity market, we’re back to where we were at the beginning of last year.”

He’s absolutely correct, of course.

Statistically, you could argue prices have barely moved in years.

The only problem with that line of logic is that it ignores what has taken place in the meantime.

Like, four years ago when the RBA, in a desperate bid to curb a runaway housing market, urged the banking regulator APRA to clamp down on interest-only loans, the preferred financing for investors.

It successfully muscled values lower and maintained the pressure.

Clearly, it was worried about a real estate bubble then.

Here we are again, and the most extraordinary thing is that we’ve just emerged from the deepest recession in almost a century with an uncomfortably high unemployment rate, oodles of spare capacity, inflation dragging along in the basement and wages growth at as slow a pace as it’s ever been.

How the RBA learned to love bubbles

Once upon a time, it was a central banker’s role to rain on the parade.

Or as William McChesney Martin, head of the US Federal Reserve in 1955, explained, to “order the removal of the punchbowl just as the party was really warming up.”

The idea was to look ahead, to take preventative action and keep things on an even keel.

So what’s changed?

For a start, there’s the fragile state of the global economy.

Then there are the concerns the Federal Government is about to rip away the budgetary support for the jobless and those left vulnerable from the impact of the pandemic on vital industries like tourism.

If the Government does reduce support, that will put a greater burden on the Reserve Bank to boost growth.

And so, with conventional weaponry almost exhausted and no real appetite to push interest rates into negative territory, our economic masters have latched on to a philosophy that’s been floating around for quite a while.

It’s called the Wealth Effect and it goes like this.

If housing prices inflate and the stock market keeps rising, people will feel wealthier and they’ll start to spend.

That, in turn, will boost earnings, investment, profits and lead to higher inflation and wages.

Rate cuts were supposed to do exactly that but didn’t.

In fact, all they’ve really done is boost asset prices. And now it’s hoped, soaring asset prices will do the job.

Of course, the biggest problem with soaring real estate prices and stock markets is that they drive a mighty wedge between rich and poor.

Those with assets end up sitting pretty. Those without end up being left further behind.

Stronger for longer

There’s an old saying among investors: markets can remain irrational for far longer than you can stay solvent.

So, as irrational as the recent booms have been, there’s every indication they will go on for far longer than is healthy.

Central banks, including our own Reserve Bank, have decided that instead of taking preventative action, from removing the punchbowl, they’ll let the party go on.

It is a dangerous game, and one that can backfire.

For the “Negative Wealth Effect” — the impact on spending when financial or property markets tank — can damage growth.

Ever since the financial crisis, central banks globally have been captured by their own actions.

They’ll do almost anything to ensure markets remain buoyant regardless of the longer-term consequences.

To be fair, the RBA reckons real estate prices will have to start moderating soon for two key reasons.

One is that for the past year, we’ve had no immigration which should have reduced demand for housing.

And the second is that a large number of newly constructed properties have yet to come on the market.

But if prices continue their stratospheric rise unchecked, it may be forced to look across The Ditch for inspiration.

The Reserve Bank of New Zealand has just raised the lending hurdles for investors after real estate surged more than 17 per cent in the past year.

So far, there’s no indication of anything like that here.

The housing market has shown a robust performance, despite the shock of Covid-19 which has created new opportunities for buyers.

The pandemic has impacted pockets of the housing market, where median values have dropped below the first home loan deposit scheme thresholds.

Recent housing value declines are particularly prominent in major cities like Sydney and Melbourne.

These cities accounted for around 75 per cent of international migration across the capital cities in 2018-19, meaning international border closures have created a particular demand shock.

On Wednesday, the minister for housing announced around 1,800 places would be re-issued from the first round of the first home loan deposit scheme.

This means recent value falls may have created an opportunity for first home buyers, where there is a maximum purchase price cap to qualify for the scheme.

As of January 2020, there was an average of 1071 suburbs observed in the capital cities with a median value at or below the qualifying threshold, assuming the application is for established property.

Established property has historically been favoured by first home buyers where benefits for both new and established property have been available.

That was further demonstrated in the slower utilisation of the scheme when it was made available for only new property.

Corelogic median dwelling value data reveals city suburbs where the median value fell below the established property price threshold since the onset of Covid.

This effectively looks at the change in the median value of all houses or units across a suburb between March 2020 and January 2021.

Note suburbs analysed include where Corelogic has high confidence in the median value, and there have been at least 50 transactions across the suburb over the past 12 months.

The list comprises 23 suburbs across the four largest capital cities.

In each of the suburbs, it is unit medians that have slipped below the threshold.

Unsurprisingly, six of these include unit values in the Melbourne–inner region, where median values have declined an average – $33,313 between the onset of the pandemic and January.

As noted in previous research, the inner region of Melbourne has seen particularly severe declines in rent and property values since the onset of the pandemic.

This is because the Melbourne-inner region has historically had particularly high exposure to housing demand from overseas migrants, such as international students, as well as people employed in tourism, hospitality and the arts.

Both cohorts have been particularly affected by the pandemic.

The same trends may explain the decline of median unit values in South Brisbane, where inner city Brisbane has also seen relatively high levels of overseas migration as a component of population growth.

While the impacts of Covid on some markets has seen a decline in values, upward pressure on prices may result from the resumption of interstate and international travel, as well as continued improvements in the Australian economy.

As more of the housing market is caught in a broad-based upswing, first home buyers could face more challenges getting into the market in the year ahead.

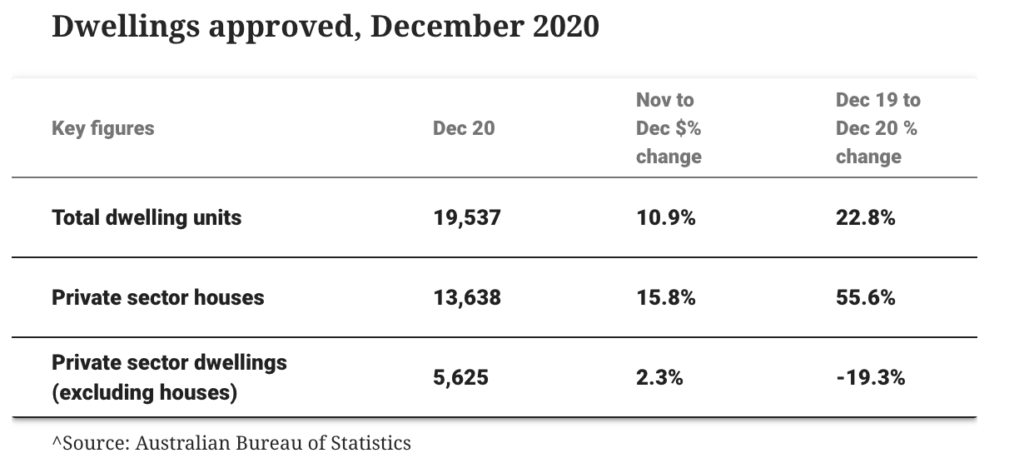

Approvals to build new houses continue to run at two-decade highs, up 55.6 per cent over the year.

Spurred by the cheapest money on record and generous government incentives, applications for new detached houses rose at their fastest pace in almost 20 years—since April 2001—to reach their highest-ever monthly total of 13,785, according to seasonally adjusted figures from the Australian Bureau of Statistics.

The slump in construction activity, which saw the AiGroup Performance of Construction index contract for 25 successive months, has rebounded since October to now be at a hit a 3.5-year high.

The value of total building approved rose 4.9 per cent in December, while the value of non-residential building rose 10.1 per cent, having fallen 27.7 per cent in November.

The total number of new dwellings approved, including detached homes and apartments, lifted by 10.9 per cent to 19,537 while attached dwelling approvals—apartments, townhouses and semi-detached homes—rose 2.5 per cent, largely reversing the losses a month earlier, to a monthly total of 5,752.

Private sector dwellings excluding houses dropped by 19.3 per cent, down to 5,625 units approved.

Approvals for alterations and additions also lifted by 8.1 per cent in December to sit 37.1 per cent higher over the year.

“Despite the uncertainty experienced by developers and households during 2020, the total number of dwellings approved in the calendar year was 4.8 per cent higher than in 2019,” ABS director of construction statistics Daniel Rossi said.

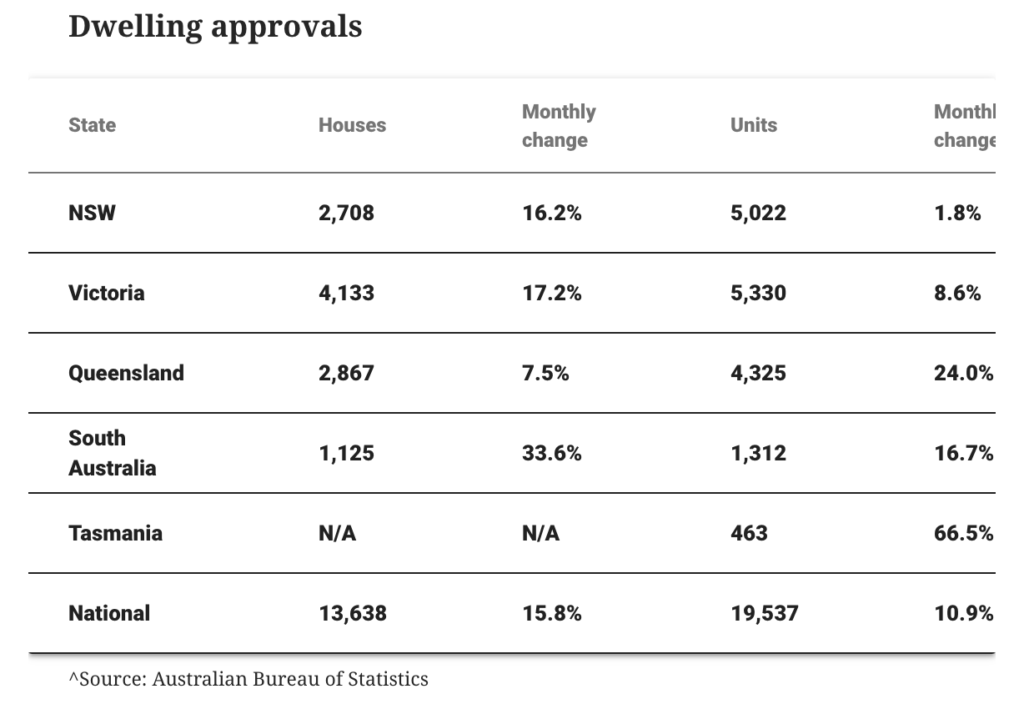

“Private house approvals were strong across the country, with Victoria, South Australia and Western Australia hitting record highs in seasonally adjusted terms.”

New South Wales recorded its highest private house approval figure since March 2000 with Queensland similarly recording its highest result over December since September 1994.

Queensland’s unit approvals surged by 24 per cent over the month, to be up 83 per cent year on year, with house approvals climbing by 7.3 per cent.

South Australia is also recorded its highest rate of growth for new houses since 2010, up 33.6 per cent.

Tasmania witnessed a 66.5 per cent lift in dwelling approvals across the month, with 463 approvals representing the highest number recorded in a month since the series began in 1983.

The value of total building approved across December also rose by 4.9 per cent, while the value of non-residential building rose 10.1 per cent, having fallen 27.7 per cent in November.

It coincides with the surge in borrowing for housing construction which is currently 75 per cent higher than July.

The total value of new loan commitments for housing hit $24 billion in November, a rise of 5.6 per cent on October and 23.7 per cent higher than the same month a year earlier.

Minister for Housing Michael Sukkar said the highly successful HomeBuilder scheme had now generated upwards of $18 billion of residential construction projects since its inception.

“Every additional building approval and every addition home sale means more work for our tradies and activity in our economy at a time it needs it most.

“The extension of HomeBuilder also ensures there will be a steady pipeline of construction activity through to 2022 to lock in this momentum for the construction sector,” Sukkar said.

In the four months leading into December, there were 26,300 applications for the $25,000 federal HomeBuilder grant for new builds, which has been extended until March at a reduced level of $15,000.

There were also 6,200 applications for the grant for “substantial” renovations.

Amid a much better than anticipated recovery from the Covid-19 recession, economists said the signs were good that approvals would continue to climb in the months ahead.

“Record lending for the construction of dwellings in December and building incentives—including the HomeBuilder extension and first home owner building grants—will fuel further strength in building approvals,” ANZ economist Adelaide Timbrell said.

“The key downside risk for 2021 approvals growth is Australia’s ongoing closed international borders, which will slow demand for housing from immigration and temporary international student and worker populations.”

Australian house prices hit record highs along the east coast, marking the steepest increase in four years and rounding out a year of unprecedented events and price predictions.

The median house value now sits at $852,940, up 4.1 per cent over the quarter and 5.8 per cent in the year according to Domain’s house price report.

Sydney, Hobart and Melbourne led the charge in the quarterly results while Brisbane made a modest improvement but was up 5.6 per cent in the year.

Meanwhile unit prices rose marginally over the quarter—with only Melbourne and Canberra seeing significant growth—but could hit new highs in the coming months according to Domain analysts.

This is a far cry from early pandemic predictions including a 7 to 15 per cent fall predicted by the Reserve Bank in the first half of 2020.

House prices across all capital cities are now at new peaks, apart from Darwin and Perth.

Domain senior research analyst Nicola Powell said the pessimistic outlook for property prices failed to materialise.

“House prices [in Sydney] finished the year 6.7 per cent higher than the previous year, although the pace of annual growth is roughly half that of earlier in the year,” Powell said.

“The rebound highlights the resilience of Sydney’s house values following a short-lived 2.2 per cent dip mid-year.

Powell said record low interest rates, the containment of Covid and stimulus packages all played a role in supporting market activity and prices.

The report also shows outer-city regions across the country saw record price growth as demand rose throughout the pandemic.

The Blue Mountains and Central Coast in NSW, the Mornington Peninsula in Victoria and Queensland’s Gold Coast and Sunshine Coast all recorded strong house price growth between December 2019 to December 2020.