Regional house and land projects are being increasingly snapped up by foreign buyers who are expanding their search for a home to live or invest in.

At the start of June, 10 buyers purchased house and land packages in the Hunter Valley – with an additional 350 expressing interest in the area.

Originating from Hong Kong, Malaysia and China, the buyers had been lured to two projects in the Hunter Valley, with another project in Lake Macquarie considered highly desirable.

Both local and overseas Chinese buyers were looking to regional areas for their Australian property investments.

Peter Li is the general manager of Plus Agency for both Sydney and Shanghai, and told The Daily Telegraph that inner-city apartments were no longer the most sought after asset for this demographic.

“Chinese buyers have reconsidered regional properties because of the pandemic-driven boom in prices there. They can pay less, get more, and obtain a higher yield if they’re purchasing for investment.

“Non-citizens who purchase a regional house and land package only pay stamp duty on the land, but if they buy an apartment they pay stamp duty on the total value.”

In comparison, Mr Li argues an $800,000 apartment will result in a first homebuyer paying 12 per cent in stamp duty – equating to $100,000.

“If you buy an $800,000 house and land package in the Hunter Valley, you only pay stamp duty on the land, which would be worth about $240,000. That means instead of paying $100,000 in stamp duty, you are only paying about $30,000.”

Located 250 kilometres north of Sydney, the Apollo Village is a housing development being constructed in the small town of Denman.

In April, 16 house and land packages within the master planned community were sold at a local event – with prices starting at $730,000.

Mr Li said the project is aimed at providing housing for people with disabilities.

“These buyers are providing a service by investing in housing for this overlooked demographic.”

Good Value Realty director John Yang said a number of Asian investors had inquired into Mount View Grange in the Cessnock council area.

Mr Yang said the master planned community will span three hectares and be close to a number of wineries.

“As the local vacancy rates are lower than 1 per cent and demand is high, Asian buyers believe it is a good investment. They are either buying pure investment properties for long-term rentals, or they are buying something they hope to use as a holiday house or a retirement home.

“This project offers a big block of land from 450 sqm to 800 sqm with prices starting from $310,888.

“You cannot buy land in China, so the first thing Chinese do when they get here is look for land they can buy. Freehold land is permanent.”

Major banks like ANZ and NAB estimate foreign buyers account for 2.5 to 4.6 per cent of Australia’s residential housing stock, with the UK holding the highest number of residents owning a property in the country.

It is estimated that Hervey Bay’s median house price in Q1 2023 will reach $608,750 and its median unit price will reach $419,000. This represents a 1.5% annual increase for houses and a 7.4% annual increase for units. The median house price for the quarter from Q4 2022 to Q1 2023 grew at a slower rate, 1.0%, and the median unit price slipped by 2.0%. This indicates that the cash rate increases have been reflected in the market. Within the last 12 months, sales declined by -53.7% (to 239 houses) and -35.1% (to 96 units), indicating an undersupply of stock.

As a result of the rapid swing in vendor discounts between Q4 2021 and Q4 2022, the average vendor discount for both types of properties has been -3.2% for houses and -2.0% for units. In the past three quarters, average vendor discounting has demonstrated a shift in market conditions in favour of buyers.

Compared to Brisbane Metro (3.7%), Hervey Bay had a 4.1% house rental yield in March 2023. In the past 12 months, the median rent for houses in the area increased by 6.0% (to $530 per week) and the number of houses rented increased by 35.9% (to 352). In Q1 2023, the average number of days on the market stayed at 23 days. The same pattern can be observed in the rental market for units in Hervey Bay, confirming its resilience.

Investing in 2-bedroom houses has provided investors with annual rental growth of 17.6%, achieving a median rent of $400 per week.

In March 2023, Hervey Bay had a vacancy rate of 1.3%, slightly above Brisbane Metro’s average of 0.9%. Investors may have capitalised on a tight rental market to drive up vacancy rates in Hervey Bay over the past 12 months, but it is still below the 3.0% benchmark set by the Real Estate Institute of Australia. Due to slower house price growth over the past quarter (Q4 2022 – Q1 2023), an investment environment has been conducive, especially in terms of affordability.

An unusual supply/demand imbalance has hit real estate across the country, affecting everyone in the marketplace – buyers, sellers and tenants.

There’s something of a perfect storm in property today, with a significant supply/demand imbalance affecting everyone in the marketplace – buyers, sellers and tenants.

Firstly, a longstanding housing undersupply has been met with a period of market change and low stock for sale.

Why is stock low? It’s likely a combination of factors, including higher interest rates making it hard for some upgraders to get the finance they need, and concern that once they sell it will be hard to buy back in.

On top of that, we’re in the midst of a rise in immigration, with the Federal Budget forecasting 715,000 new migrants (net) to move to Australia over the next two years alone. That is already adding significant demand to the sales and rental markets of Sydney and Melbourne, in particular.

Migrants typically rent for the first few years but some are buying instead because finding a rental has become difficult due to record low vacancy rates. So, that’s extra demand going into the sales market today.

Also, an extended period of high construction costs, labour shortages, and stories of builders going bust has likely encouraged more families to buy in the established market instead of building their next home. So again, that’s extra demand flowing into the sales market.

Strong employment is underpinning demand, but we also have a large and growing cohort of buyers in the marketplace today that is unaffected by interest rate rises because they’re purchasing with cash.

CASH BUYERS EATING AWAY AT SUPPLY

Data from the electronic conveyancing company, PEXA shows 25 per cent of East Coast residential sales in 2022 (NSW, Queensland and Victoria combined) were to cash buyers.

Many of them are in the prestige sector where cash purchases are common, others are baby boomer downsizers.

Some are foreign buyers purchasing for themselves, for their children who are studying here, or for investment.

Some are buying in the regions – likely city dwellers making a seachange or treechange to more affordable markets. Today’s first home buyers also have a lot of help, which is somewhat offsetting the impact of rising rates. There’s the Bank of Mum and Dad and loads of government help including stamp duty breaks and the First Home Guarantee.

Put all of this together, and we’ve got a supply/demand imbalance that is making it quite hard for buyers in some areas to find the right property at the right price for them.

It’s taking longer to secure a home, and this is creating a sense of urgency and stronger competition, which is why prices are moving upwards earlier in the market cycle than we’d normally expect, given rates are still rising. (Yes, rates are on hold for now but the Reserve Bank has flagged that further rises may be necessary.)

BANK WATCHDOG HELPED CREATE RENTAL SUPPLY CRISIS

The supply/demand challenge in the sales market is also present in the rental market.

The undersupply in rentals has been growing for years due to a decline in investor buying between 2014 and 2020, according to Bureau of Statistics figures.

Now that rental demand is rising, we’re seeing the impact of that undersupply in the form of rising weekly rents.

Rising inflation and interest rates are also key factors. Landlords are paying more interest on their loans and higher amounts for council rates, insurance and repairs, so they have to raise the rent to keep their investments viable.

Looking ahead, we are expecting the supply/demand imbalance in the sales market to loosen next month. There are already signs that stock is rising, partly due to the Spring season but also likely due to improving prices. In the rental market, we’re unlikely to see weekly rents stop rising until interest rates stop rising.

The good news is that many economic analysts think we’re very close to the end of rate hikes, with inflation steadily falling and retail volumes dropping as people rein in their spending.

The Fraser Coast council has begun clearing at the site of its CBD redevelopment, despite the project not yet having the final sign-off from its elected representatives.

Demolition work at the corner of Main St and Torquay Rd at Pialba has begun, despite the final sign-off on the multimillion dollar redevelopment of the site yet to be given by Fraser Coast councillors.

The council is expected to vote on final approval of the $100million public plaza, library, council administration centre and community spaces later this month. But the bulldozers have already moved in.

It is understood preparations have begun ahead of the vote as delaying could hold the project up for months.

Deputy Mayor Denis Chapman said the federal government was partnering with the council through the Hinkler Regional Deal to build the new community hub.

The big spending in Hervey Bay has left ratepayers in other parts of the region unimpressed.

“The new development in the Hervey Bay City Centre will feature a public plaza, a larger library over two levels, a council administration centre incorporating a Disaster Resilience Centre and flexible community spaces that can be booked day and night,” Mr Chapman said.

“This project is a once-in-a-generation opportunity to reshape the Hervey Bay city centre, to create jobs and drive economic growth and investment.

“Detailed design of the new Hervey Bay Library and Council Administration Centre is underway now, and work on undergrounding power near where the new building will be is due to start later this month.

“Before that can happen, the vacant building that council owns on the corner of Main Street and Torquay Road must be demolished. That work has started this week and is expected to be finished in the coming days.

“The work to underground power is expected to be completed by November, weather and construction conditions permitting.

“There will be traffic management in place while the works are underway to underground power, including a full closure of Torquay Road from the Torquay Road roundabout west while trenching works are completed.

“Council will be working with Ergon to ensure businesses in the area have continued power supply while the process to underground power is underway.

“We thank businesses and residents in advance for their patience while this important work occurs.”

Councillor David Lewis said more than three-quarters of the development would be community space.

“The new library and council administration centre will be a place to support learning and innovation, and a place where the community can come together to socialise and benefit from centralised council services,” he said.

“By improving the library’s floor space and design, we can cater for our growing population and help improve education outcomes in our region.”

The project has had some detractors, with Maryborough MP Bruce Saunders calling it the “Hervey Bay Taj Mahal”.

It would be partially funded with $40 million awarded from the Hinkler Regional Deal, but the council would need to borrow more than $50 million to build the new facilities, a figure Mr Saunders said would blow out.

“By improving the library’s floor space and design, we can cater for our growing population and help improve education outcomes in our region.”

The project has had some detractors, with Maryborough MP Bruce Saunders calling it the “Hervey Bay Taj Mahal”.

It would be partially funded with $40 million awarded from the Hinkler Regional Deal, but the council would need to borrow more than $50 million to build the new facilities, a figure Mr Saunders said would blow out.

North Rothbury ranked number one in CoreLogic’s Hedonic Home Value Index in 2022, which encouraged investors to invest there. Why? North Rothbury shares a postcode with Huntlee, the Hunter Valley’s newest masterplanned development.

A new town center with all your essential shopping and personal needs awaits you in Huntlee, just north of the Pokolbin wine region. The main hub is located just north of the Pokolbin wine region. In addition to the daycare, medical center, Coles supermarket [see scroller at bottom], a tavern, and specialty shops, Huntlee Fitness will open in just a few weeks.

With the vineyards right outside your doorstep, Huntlee offers a few years worth of quality weekends. But it turns out Huntlee is well located for another very important reason as well. There are many job opportunities available in Singleton, Maitland and Cessnock, ranging from education to engineering, hospitality to high-tech. Thus, Huntlee has become a destination for working families in the area looking for a safe and supportive environment to raise their children.

It’s all in the numbers

As the Hunter’s first town in 50 years, the masterplanned community will eventually have 7500 residents spread over four villages. The area is 45 minutes from Newcastle and is easily accessible from the freeway to Sydney, so residents are taking full advantage of the remote-working revolution that has taken off since Covid.

As forecasts indicate, North Rothbury-Branxton-Greta is poised for explosive growth, and the region’s unsurpassed lifestyle as well as home prices well below the NSW median make it highly desirable.

It is estimated that the population will grow by more than 60% to 14,100 residents by 2041 — a sixty percent increase from the current 8800 residents.

Hydrogen hub

With the average block in Huntlee ranging from 225sq m to 897sq m, residents can achieve a home that is out of reach in the major urban areas. The median rental yield is a healthy 4.9 per cent* and the rental vacancy rate is just 2.79 per cent*. With the Hunter announced as one of NSW’s first green hydrogen hubs, the region is poised to become a major employment centre for new low-carbon jobs#.

Development is also happening at pace in the town centre. Across the road, the luxury retirement village, Green Ridge, is under construction. Nearby land earmarked for primary and secondary schools is ready for development, as the area is now approaching government-mandated population milestones. In the short term, Branxton and Greta primary schools are minutes away; a wide range of public and private secondary schools are also close by.

Planned to prosper

The emphasis in Huntlee is on self-sustainable communities that generate their own micro-economies by providing employment, education, entertainment, shopping and community services all within the town.

Connectedness is key at Huntlee, which is dotted with parks and walking paths. Huntlee District Park is the jewel in the crown, acting as a social hub for friends and families. Set among the trees is a cafe, an amphitheatre, picnic areas, barbecue facilities and an adjoining dog park.

The year 2023 will see the development focus swing to bringing even more vitality and diversity to the town centre with modern residential and residential/commercial townhomes all within walking distance of the shopping precinct. The Urban Series development offers super modern, open-plan designs––packing a lot of home into highly affordable land footprints.

“The Urban Series will offer a new way of living in the area, especially for the growing number of working and professional people and their families,” says Robert Crane, sales director of Huntlee. “The lock and leave lifestyle will suit a wide range of people, from young couples, executives, right through to downsizers and retirees.”

Huntlee’s residential community is a mix of owners and renters. As at early 2023, the median house price was $826,000 with the median rent $685 a week. Huntlee’s latest land release offers flexible block sizes to suit a variety of needs, the average range is 225sq m to 895sq m with a handful of larger lots available.

Australia’s leading builders offer an impressive range of homes open for inspection at the Huntlee Display Village, worth the trip alone just to steal some design ideas. Of particular interest to investors is the ability to choose design configurations that maximise rental returns and resale.

All land lots come with standard electricity, water and sewer connections. Huntlee also provides a separate recycled water system for toilets and gardening, eliminating the need for bulky water tanks. As well as this, there’s natural gas and FTTP internet connections, fencing at the side and rear, and front landscaping all included in the land purchase price.

The investment and determination to masterplan an entire town is significant. However, the pay-off is also worth the effort, with returns and resales of Huntlee properties homes outperforming the broader housing market. Executive summary: the perfect combination of low vacancy plus high yields in a booming location.

The rapid increase in Australian property prices during 2020 and 2021 is well known to anyone who has sold or bought a property in recent years. While the RBA lifted the cash rate and mortgage rates increased over much of 2022, property prices fell, even dramatically in some markets. CoreLogic’s Home Value Index recorded a slight rise of .6% across all capital cities in March and a rise of .5% in April-the first such rises in 11 months. Many property experts are already predicting the end of the property slump as prices remain above pre-pandemic levels.

The director of research at CoreLogic, Tim Lawless, noted at the release of the Home Value Index in May that net migration and a shortage of inventory likely contributed to the housing market’s recovery.

“Through the downturn, many prospective vendors have stayed on the sidelines, keeping inventory levels low and giving sellers some leverage at the negotiating table,” Lawless said.

It is believed by many buyers that the rate hike cycle is nearing its end.

It may be contributing to a general perception that the market has bottomed out, and that it’s a good time to buy, according to him.

It is likely that consumer sentiment will improve as interest rates stabilize, which will increase buying and selling activity in the housing market.”

Due to its high housing debt ratio, Australia was recently ranked as the second-highest country for “housing market risk” among 27 countries.

It is widely believed that the property market will crash in the near future. We spoke to two experts to find out their opinions.

A Covid-led Boom

Australian properties are still extremely expensive, despite the fact that they have become more affordable since the pandemic.

The Australian housing market reached its peak in April 2022, when it had risen by about 30%, says Eliza Owen, Head of Research, Australia at CoreLogic. Between late 2020 and early 2022, regional Australia experienced an upswing of about 40%, while capital cities experienced an upswing of about 25%.”

According to Owen, the boom was largely fuelled by emergency low interest rates during the Covid-19 pandemic, which reduced borrowing costs, and by a strong recovery with high demand, low unemployment, and high levels of savings.

The housing market was also buoyed by some preference shifts that occurred during the pandemic, including increased demand for holiday houses, tree-changers moving to regional areas, expats returning, and people wanting more space or their own space after lockdowns.

So Will the Property Market Crash?

Australian capital cities’ housing markets fell by -5% in 2022, according to Domain figures. In Sydney, house values declined by -10.9%, and in Melbourne, they fell by -5.9%. In Canberra and Brisbane, they declined by -6% and -1.1%, respectively.

By the end of spring selling season, most of the damage had been done. Between early 2022 and November, Australian combined capital city property prices fell 6.5%, according to CoreLogic figures.

However, Owen does not consider this a crash.

In my mind, a housing market crash is defined by the loss in value and a loss in mortgage serviceability, when people can’t service their mortgages, and they have to sell, but they can’t get enough money to pay off the loan when they try to sell.” We’re not seeing that right now.

Although the property market was in a downturn over the latter half of 2022, Kilroy says a crash is unlikely due to strong economic fundamentals. The first is demand, with high rents and the return of overseas migration resulting in more buyers. On the supply side, low unemployment is limiting the number of properties for sale, with distressed sales not yet evident.

Check out this article for more information: How to beat the rate hikes

The Impact of Rate Rises

Last year’s property market downturn was largely caused by rising interest rates, according to Kilroy. There is a credit availability issue driving this downturn, rather than an increase in unemployment or oversupply.”

After raising interest rates ten consecutive meetings beginning in May of 2022, the Reserve Bank of Australia raised the cash rate to 3.6% in April before holding it steady.

According to Owen, this is the fastest rate increase since the early 1990s as a result of extremely high inflation levels. A major cause of this correction in housing values has been the rise in interest rates, so this has essentially reversed the upswing in housing prices.”

Is 2023 going to be a year of rate declines?

What Is in Store for the Property Market?

In Owen’s words, “prices will continue to fall as long as interest rates rise”. Her research indicates that the magnitude of the declines has moderated in recent months, with a national drop of 1.6% in August slowing to a fall of 1.2% in October. Over the past few months (of last year), there has been a slowdown in the pace of decline, and an orderly trend is beginning to emerge.”

Then, of course, there was the slight rise in CoreLogic’s dwelling values in March of .6% and .5% for April, indicating that we may have reached the bottom of the falls.

Owen says the best guide for the housing market outlook is the cost of debt, with property prices likely to increase once interest rates start to fall, something Kilroy is expecting in either the last quarter of 2023 or the first quarter of 2024.

However, Kilroy adds that since the boom was fuelled by the unique circumstances of a global pandemic, property prices aren’t expected to bounce back to their previous highs in the short term, as interest rates are unlikely to fall as far. She is forecasting any fall in interest rates to bottom out at around 2.6%.

How Far Will Prices Fall?

“We’re expecting a nationwide dwelling peak-to-trough price fall of 11.5%, and we’re expecting that trough to be met in the second half of (2023),” Kilroy says, adding that BIS Oxford Economics forecasts are “at the low end of the scale compared to some commentators”.

However, the same falls will not be experienced universally.

“We’re forecasting a 13% fall for houses and 8% for units, and we’re forecasting Sydney to have the greatest fall in house prices of around 18%, while we have Perth houses at the other end of the scale with a more modest 4% drop.”

While CoreLogic doesn’t make forecasts, Owen says that the Big Four banks are tipping combined capital cities prices to fall by a median of 16%. “Based on the forecasts, this could be one of the largest housing market downturns that we’ve observed, but this is coming off the back of one of the biggest upswings we’ve observed in Australia’s housing market as well.”

However, by late April, ANZ had updated its forecast, downgrading its prediction of a peak-to-trough fall from 16% to 10%. In May, the big four all released revisions of their earlier housing price predictions, reneging their previously pessimistic takes.

Domain economist Dr Nicola Powell said there were signs that the bottom had been reached, and the turnarounds of the banks could be a strong indicator.

“This could very well be the bottom of the market, but we need another couple of quarters of sideways movement of prices, or slight improvements, before that is confirmed,” she said.

Whether this is the bottom or the beginning of another boom is yet to be seen, and, alike to the economists, the banks are split: CBA predicts prices to rise 3% in 2023; NAB expects a slight fall in the year; ANZ and Westpac say the market will be mostly flat for the rest of the year.

Is Australian Housing at Risk?

Most recently, the IMF released a report, A Rocky Recovery, that ranked Australia second only to Canada in relation to housing risk. It did so after looking at five key metrics:

Outstanding housing debt to household income in June last year. Australian housing debt is roughly 145.4%, of the country’s total disposable household income.

The share of housing debt on variable interest rates. Around 70% of loans are variable in Australia.

The share of home owners with a mortgage—around 37%.

Cumulative cash rate changes from March 2020 to September 2022. The RBA has hiked rates 10 times since April last year.

Real house price growth between March 2020 to March 2022, which in Australia amounted to a pandemic surge of about 25%.

Commenting on the IMF report, Owen said that while the ranking is sobering, there is reason for optimism.

“Many households have accrued strong savings buffers through the low interest rate period, and labour markets remain extremely tight,” Owen said.

“Housing market conditions are turning a corner amid low stock levels, rising demand from overseas migration, and consumer sentiment shifting higher as we approach what may be the end of the rate-tightening cycle.”

As the IMG said in its report: “In most cases, it is unlikely that an ongoing fall in house prices will lead to a financial crisis, but a sharp drop in house prices could adversely affect the economic outlook.”

There’s more to NDIS properties than meets the eye when it comes to achieving returns three to four times higher than traditional property investments.

A surprising performer continues to be a viable investment option for property investors despite much coverage of Australia’s housing boom in 2021. NDIS property delivers returns of up to 20% per year due to Australia’s unpredictable housing market, which is home to thousands of disabled Australians.

While NDIS property investments offer significant returns, the ethical implications are also significant. During the next four years, the number of users of supported independent living is expected to increase by 35% from 26,000 to 35,000, according to a statement released by the National Disability Insurance Agency in August last year.

NDIS properties nationwide are in short supply, which contributes to the rise in Australians needing supported living. Linda Reynolds, Minister for Government Services and National Disability Insurance Scheme, said the Government understands it can be challenging for some participants to find suitable Specialist Disability Accommodation (SDA).

Minister Reynolds said that expanding the SDA market is critical to ensuring that participants with high support needs have access to housing that is innovative and meets their needs.

SDA is specifically designed housing for people suffering from severe functional impairments and/or who require high levels of support. Each year, the Federal Government provides $22 billion in NDIS funding to individual participants to pay for housing under SDA.

Ethical considerations versus financial gain

Founder and managing director of NDIS Loan Experts Yannick Ieko said if you look at it purely from a numbers perspective (because not everyone is interested in ethical aspects), you can generate a much higher income or yield with an NDIS property than with a traditional investment property.

The truth is that Australians with disabilities are facing a terrible, terrible situation at the moment. In particular, young people with disabilities are being forced to live permanently in retirement homes, hospitals, or some very inappropriate settings in order to meet their needs, according to Mr Ieko in Your Investment Property magazine.

As NDIS houses, apartments, and townhomes are constructed, they will provide some stock for those people to move into a place that is entirely suited to their needs, which is the ultimate win-win.”

I want to invest. What should I do?

Those tempted by the returns and potential for life-changing changes will find it difficult to find and purchase an established, completed NDIS property with a tenant already living there.

Most investors we see buying NDIS properties are purchasing house and land packages, which means they are creating new housing stock, which is what is most needed.

“It’s not completely different from traditional house and land investments, in that you still need a parcel of land, knockdown or rebuild, or if it’s in a new estate, identify the land and purchase it. You should engage a builder that specialises in NDIS properties like G Developments. prior to purchasing as the block needs to be assessed due to access requirements.

The limited number of NDIS specialists across the country makes it very helpful to work with someone who has expertise and a network within the space, Mr Ieko says.

Despite its specialized nature, NDIS property is not out of reach for anyone willing to put in some time in order to reap some very big rewards, Mr Ieko explained.

Incentives from the Federal Government’s SDA scheme account for the rewards mentioned by Mr Ieko. Registered providers can lease approved SDA housing to approved participants on behalf of investors. SDA funds can only be paid to registered providers with enrolled and compliant properties.

The apparent decline in popularity of Brisbane real estate toward the end of last year appears to be over, with the city’s real estate market regaining momentum and trailing only one other state capital.

With a fourth consecutive month of price growth, Brisbane property buyers are demonstrating a robust appetite for real estate.

Property prices in the capital of Queensland also increased in June, albeit at a slightly slower rate than the month before, in keeping with the overall trend of rising home values across the nation.

For the second month in a row, detached houses led the recovery, growing faster than units.

Albeit that pace of development in June marginally facilitated contrasted with May, it stayed solid notwithstanding the effect of increasing loan fees and school occasions on the general market.

Given the low consumer sentiment associated with the initial shock of Covid and the Global Financial Crisis at the beginning of the year, it may be considered remarkable that buyer numbers remain resilient.

The closeout market in Brisbane showed soundness from May to June. As per Apollo Closeouts, the typical leeway rate in June was 65%, marginally lower than May’s 66%.

While the typical number of enrolled bidders per sell off diminished somewhat from 3.9 in May to 3.7 in June, there was a striking expansion in the level of enlisted bidders who effectively partook and made offers, ascending from 60.3 percent to 63.95 percent across the two months.

Brisbane is presently the subsequent best performing property market among Australia’s capitals, sitting simply behind Sydney as indicated by the June cost development information.

While certain people might decide to sell because of rising holding costs, especially those progressing from fixed loan fees in the last a very long time of 2023, the current profundity of purchasers seems adequate to retain such changes.

Except if there are significant changes sought after drivers, it is far-fetched Brisbane will observer further cost decreases for the time being.

New listings scarce in Brisbane

Again reflecting the broader national situation, the issue of limited supply continues to dominate the Brisbane market.

According to CoreLogic, new listings entering the market are 30 per cent lower than this time last year, while total listings in Brisbane have decreased by 15 per cent from a year ago.

This scarcity of available properties poses a significant challenge for Brisbane property buyers, as despite their willingness to make transactions, they struggle to find suitable options to purchase.

Sellers in Brisbane have been hesitant to put their properties on the market, primarily due to the lack of confidence in finding a new property to buy or rent.

In an exceptionally competitive rental market, the possibility of renting as an interim solution between a sale and purchase is challenging and often impossible.

The absence of widespread panic among sellers has resulted in a situation where they refrain from taking action, further tightening the market.

Options for buyers vary across different suburbs.

According to PropTrack data, certain suburbs experienced a significant decrease in new listings compared to the previous year.

Marsden, located in Brisbane’s south and known for its secondary school catchment zone, witnessed a decline of 64 per cent in the year to May.

Similarly, Yeronga and The Gap also had substantial drops in year-on-year listings, with 59 per cent and 55 per cent fewer properties available for sale, respectively.

On the other hand, some suburbs provided more choices for buyers.

Ashgrove in Brisbane’s inner northwest saw a remarkable increase of 108 per cent in year-on-year listings. Ascot and Auchenflower were also big movers over the year, each with 64 per cent more options.

Real estate buyers making compromises

The ongoing increase in interest rates is significantly affecting borrowing capacity, which in turn impacts the property demand, however, what we’re observing is that individuals are making compromises based on affordability, rather than delaying their property purchasing decisions.

Compared to other capital city markets, Brisbane property remains more affordable than most.

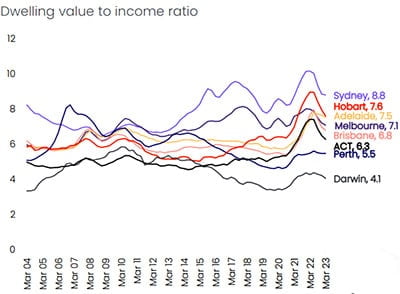

The dwelling value-to-income ratio for Brisbane is lower than that of Sydney, Hobart, Adelaide, and Melbourne. It’s little wonder buyers from other east coast capitals are increasingly drawn north.

According to CoreLogic, Brisbane property buyers need to allocate 40 per cent of their household income to cover mortgage payments.

While high and placing the average borrower in the mortgage stressed category, this percentage is 52 in Sydney, 45 in Hobart, and 44 in Adelaide, making Brisbane the most affordable capital city on the east coast.

This affordability factor has contributed to an influx of buyers relocating from the south in recent years.

Many of these newcomers have sold their homes in New South Wales or Victoria and found equally desirable properties in Brisbane, with substantial savings remaining.

Alternatively, some buyers are upgrading their homes to enhance their lifestyle, fully aware that they can stretch their budget further and secure a high-quality property in Brisbane.

Units no longer star of the show in Brisbane

In June, the values of dwellings in Greater Brisbane rose by 1.3 per cent, according to CoreLogic, translating to a quarterly growth rate of 3 per cent. The median value of a dwelling in Greater Brisbane now stands at $725,397.

Additionally, PropTrack data reinforces this positive trend, indicating a 0.08 per cent increase in dwelling prices for the month across Greater Brisbane. The median value of dwellings by PropTrack is recorded at $731,000.

Brisbane’s housing market has shown strong performance for the second consecutive month, with median house values outpacing unit growth.

In June, median house values experienced a 1.3 per cent increase, resulting in a quarterly growth rate of 3 per cent. The current median value for a house in Greater Brisbane stands at $806,781, according to CoreLogic.

PropTrack data also confirms positive growth in the housing market, reporting a 0.18 per cent increase in house prices for June.

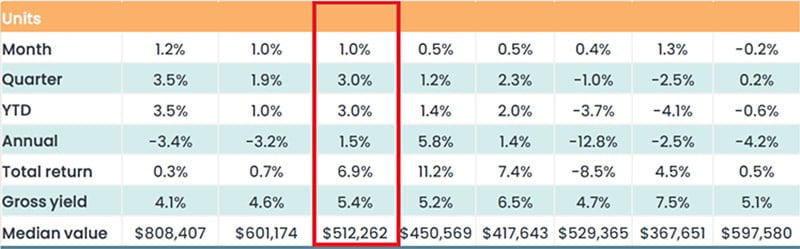

In June, the median value for units in Greater Brisbane were outpaced by houses, recording a 1 per cent increase while reaching a new record median of $512,262.

This growth aligns with the housing market on a quarterly basis, which has also now experienced a 3 per cent increase over the last three months.

Over the past year, units have still outperformed houses in Brisbane, with a 1.5 per cent increase in median values compared to a 9.9 per cent decrease in housing values, as reported by CoreLogic.

However, in contrast to the above information, PropTrack data presented a slight negative change in median unit prices for Brisbane in June, recording a 0.5 per cent decline. The current median value for units, according to PropTrack, stands at $546,000.

Signs of mercy in tight rental market

According to the most recent data from SQM Research, the vacancy rates in Brisbane have remained stable from April to May, staying at 1 per cent.

While the overall city-wide trend remains unchanged, certain regions within Greater Brisbane are experiencing an increase in vacancy rates.

The Ipswich region, for instance, has seen a rise from its lowest point of 0.5 per cent in August last year to the current vacancy rate of 1.5 per cent. Similarly, the Brisbane CBD, which previously had a low vacancy rate of 0.9 per cent in February, has been consistently increasing and now stands at 1.4 per cent.

Brisbane is still witnessing robust international demand for rental properties.

Net overseas migration is projected to reach 400,000 this fiscal year, marking a remarkable surge of nearly 27 per cent compared to the previous record set in 2008. It is worth noting that the majority of international migrants prefer to rent rather than buy when they first arrive in Brisbane.

According to data from PropTrack, the top countries conducting rental searches in Brisbane include New Zealand, United States, United Kingdom, India, China, and Singapore.

Notably, the return of Chinese students to Australia has had a significant impact on the increase in rental searches, as confirmed by PropTrack data.

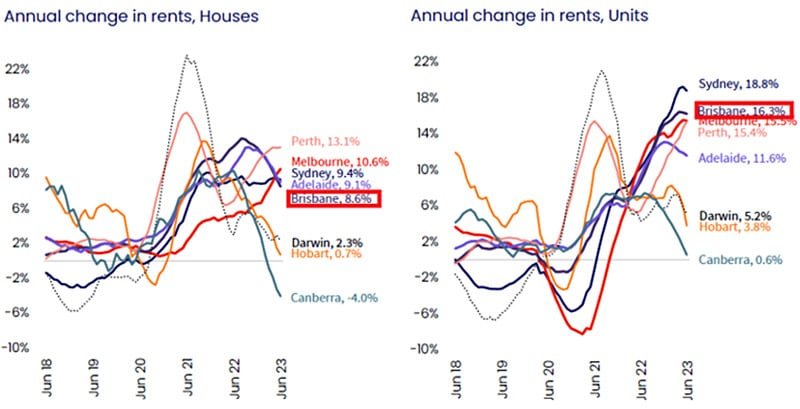

Over the past 12 months, house rents have increased by 8.6 per cent, as reported by CoreLogic, while unit rent growth has nearly doubled at 16.3 per cent.

Despite these trends, rental yields have remained steady this month, with gross yields for houses holding at 4 per cent and gross yields for units at 5.4 per cent.

The top 20 locations in Australia for property investors with a $100,000 deposit have been revealed, with seven suburbs in Newcastle included in the list.

Online research company Suburb Help has identified 20 locations in its $100k Investment Report. It includes nine suburbs in NSW, six in the ACT, two in South Australia, two in Victoria and one in Tasmania with a mix of both metro and regional locations.

To make sure locations were suitable for investors, suburbs were excluded if they had a:

Median price above $1m

Owner-occupier share of 65% or more than 90%

Renter share less than 10% or more than 35%

Vacancy rate more than 1.5%

Yield less than 3%

Median weekly rent that has increased by less than 5% over the previous 12 months

This process excluded the vast majority of suburbs in Australian, leaving just a small number of investor-grade suburbs. Suburb Help then whittled the suburbs down to a top 20 and ranked them based on median price (from lowest to highest).

“The cheapest median price is just $590,000, potentially making that suburb accessible for an investor with a deposit of $59,000,” said Suburb Help chief property strategist Veronica Morgan (pictured above left).

Morgan said it was not easy to buy a property right now for a couple of reasons.

“First, even though prices are declining in many parts of Australia, they’re still elevated following the recent boom,” she said. “Second, investors’ borrowing power is declining with every Reserve Bank rate hike, so it’s good to know that if you find a lender prepared to accept a 10% deposit, you can still buy into a good investment location for a relatively modest price, provided you do your research.”

Morgan said every location in the Suburb Help $100k Investment Report had been carefully selected.

“We wanted locations that were not only likely to record above-average capital growth over the long-term but would also provide a healthy cash return right now,” she said. “That’s why we limited ourselves to locations that had low vacancy rates and reasonable yields. As a result, if you buy a quality property in one of these locations, you should find it relatively easy to secure a reliable tenant prepared to pay a good rent.”

Brenden Lowbridge (pictured above right), director of Newcastle brokerage Money Links, said investors could enjoy the benefit of investing in a growing area close to Sydney.

“We have an affordable price point when compared to Sydney along with excellent lifestyle benefits, increasing rents and very tight rental vacancy which has provided the perfect storm for Newcastle and Lake Macquarie,” Lowbridge said. “Investors have also seen that capital growth in many cases over this last growth period has kept up with Sydney suburbs.”

Lowbridge said he had noticed an increase in investor clients wanting to purchase in Newcastle.

“I have noticed there are more experienced investors using the current negative market sentiment to their advantage,” he said. “We just assisted an investor purchase a unit in the beachside suburb Merewether for $650,000. There are many comparable sales from six months ago that are in the $720,000 range.”

Lowbridge said he forecasted this trend to continue.

“I believe when interest rates level out later this year, confidence will return and a larger wave of buyers will come into the market,” he said. “I also believe that a big reduction in construction starts due to build cost increases will put more pressure on existing rentals, meaning an increase in rental yields. Investors will be attracted to these improved yields and push into the market.

“Whilst people have transitioned to Newcastle from Sydney, due to limited employment opportunities I believe that this has been slow to begin with. As large national employers start to consider these areas as an option and employment opportunities present themselves, migration will really kick in which will push up local rents and prices.”

There are many hidden gems in Maryborough for property investors, although the suburb is largely known as the gateway to Fraser Island’s natural wonders.

This month, Smart Property Investments released its highly coveted FAST 50 ranking for 2024, which includes the Queensland suburb, which is located about three hours north of Brisbane.

Using open-source data and insights from a 14-strong investment expert panel, the report and ranking provide an insight into the 50 Australian suburbs that have the best prospects for the future.

Maryborough offers home buyers and investors an affordable entry point into or expansion into the market with a median price of $340,000.

However, the suburb is not just known for its low house prices. Property Investing Matters host and creator Margaret Lomas says Maryborough’s untapped potential is significant.

“It is placed to enjoy runoff demand from nearby Hervey Bay – long-term opportunity for growth over time, suitable for those wanting low buy-in prices and higher yields.”

The recent growth data shows Maryborough presents a compelling investment opportunity backed by solid market performance.

With a median quarterly growth of 1.50 per cent, and an impressive 12-month growth of 17.20 per cent in prices, the suburb is steadily gaining attention from astute investors. Additionally, properties in Maryborough have also recorded an attractive average annual growth rate of 5.60 per cent.

This consistent growth highlights the suburb’s potential for long-term capital appreciation, making it an enticing prospect for investors seeking solid returns over time.

In addition to capital growth, Maryborough boasts a strong rental market. The gross rental yield of 6.30 per cent indicates the potential for attractive rental income compared to the property’s median price.

And with a median rent of $410, investors can expect a steady cash flow and healthy returns on their investment properties.

Maryborough’s lower entry costs, combined with the potential for capital growth and solid rental yields, make the suburb an appealing option for those seeking a balanced investment approach.

From an investment perspective, Maryborough offers diverse options to suit various investment strategies. The suburb features a range of property types, from spacious family homes to quaint cottages and modern apartments.

Notably, new research from a subsidiary of the PropTech Group, Real Estate Investar, has also identified Maryborough as one of the Australian suburbs with the most opportunities to subdivide.

Joe Hanna, managing director and chief executive officer at PropTech Group, believes “the fact that properties with high subdivision opportunities are not more expensive shows us that there are still many opportunities for investors.”

“The purchase price isn’t higher and doesn’t reflect the value you can unlock by subdividing. That’s probably because of the work and uncertainty involved in the process,” he said.

“There is plenty of opportunities for investors willing to go this route.”

For home buyers who want to immerse themselves in history and experience the charm of a bygone era, Maryborough’s well-preserved streetscape, complete with grand colonial buildings and heritage-listed structures, provides a window into the past.

Maryborough’s proximity to essential amenities also enhances its investment appeal. The suburb offers convenient access to schools, shopping centers, medical facilities, and recreational areas.

Markedly, its location within a short distance from major employment hubs ensures a steady demand for rental properties, making it an attractive prospect for investors seeking reliable rental yields.