The prospect of strong capital gains is luring investors back into the market in addition to strong rental price growth.

Australia’s rental crisis is driven by a chronic shortage of rental properties and a rapidly growing population.

Both buyers and sellers continue to benefit from the current market conditions.

PropTrack reports that the number of properties hitting the market has increased, and auction volumes and sales have consistently exceeded last year’s.

As well as strong rental price growth, which maintains healthy rental yields, investors are attracted by the prospect of strong capital gains.

Australia’s rental crisis is driven by a chronic shortage of rental properties and a rapidly growing population.

As a result of this situation, investors have returned to the market.

This is the third consecutive month that new lending, excluding refinancing, has increased.

New lending has followed improved housing market conditions since 2023, with prices recovering from declines in 2022.”

A buyer’s and seller’s sense of confidence

The current market conditions remain positive for both buyers and sellers.

The number of properties hitting the market has increased, and auction volumes have consistently been higher than last year, according to PropTrack’s data.

There has also been a substantial increase in sales.

New lending grew by 4.8% in April, the highest monthly increase since January 2022, and by 24.6% year-over-year, the highest since December 2021.

New lending grew by 5.6% for investors and 4.3% for owner-occupiers, with investor activity increasing by 36%.

Prices and yields of rental properties

In spite of recent slowdowns in rental price growth, rents have still increased faster than property prices.

According to PropTrack’s latest Rental Report, gross rental yields have reached their highest level in almost four years.

Further comments were made by Ms Creagh:

The strong growth in rents and increasing property prices have attracted investors, particularly in Queensland, South Australia, and Western Australia, where new lending to investors has reached record levels.”

The first half of 2024 has seen strong growth in property prices in these states.”

Rental markets are tight

Australia’s tightest capital city rental markets can be found in Queensland, South Australia, and Western Australia.

In the past year, Perth prices have increased by 20.58%, while Adelaide and Brisbane prices have increased by 14.49% and 13.69%, respectively.

Vacancy rates remain around 1% in Brisbane, Adelaide, and Perth, making it difficult for many to find available rentals.

This means properties are unlikely to sit untenanted for long, given the high demand.

Investments on the interstate

More investors are looking to buy interstate according to realestate.com.au.

Among interstate buyers, South Australia accounted for 29% of enquiries.

With 27% and 25% of enquiries, respectively, Queensland and Western Australia follow.

Due to the chronic housing shortage, investors are expected to increase their investment activity.

In the future

While population growth remains strong, Ms Creagh predicts a worsening shortage of homes due to low building activity.

Property prices are likely to rise regardless of interest rates, according to many investors.

As investor activity increases, long-term rentals will increase, helping to ease rental market constraints and the chronic shortage of rental supply that has led to record-high rental prices.

With government incentives, first-time buyers are still pursuing their property buying goals despite deteriorating affordability.

In April, first-home buyer loans rose in both number (+3.0%) and value (+3.4%)

Ongoing home price rises are likely incentivizing many to overcome affordability challenges and transact with the expectation of further price growth.

The tough rental market situation has likely encouraged some renters to purchase their own homes sooner, adding to demand.

Ms Creagh further said:

“The strength in new lending activity is expected to continue as the stage three tax cuts came into effect on July 1, supporting real incomes and boosting borrowing capacities.

Home prices are also expected to lift further, although the pace of growth may slow during the seasonally quieter winter period, particularly with the increasing probability of another rate rise this year.”

In five Queensland regions, investor hotspots have been identified as the next places to invest “before the boom”.

Based on InvestorKit’s Overvalued or Undervalued research, we’ve identified the top locations set to boom in the next 12 months based on housing affordability.

Our data-driven predictions of overvalued and undervalued cities last year proved accurate, with more than 80 percent of overvalued cities experiencing a housing price decline, while more than 90 percent of undervalued cities and regions enjoyed an average growth of more than 7 percent.

Even though the Australian housing market is going through a rough patch, our data suggests there are opportunities to find an affordable growth investment in undervalued markets with strong fundamentals.”

Among Queensland’s top investment destinations, InvestorKit recommends Bundaberg, Townsville, Rockhampton, Warwick, and Gatton.

“These regions have strong or strengthening local economies,” Mr Paliwal said.

Over the past decade, their unemployment rate has been at its lowest level ever

All of them are experiencing faster growth rates in the GRP (gross regional products) and in population growth rates.”

The high demand in the identified regions contributes to the limited supply, according to Mr Paliwal, who also noted that each of these towns is not only affordable, but also has bright growth prospects. Despite the high market pressure, inventories are really low in each of the five regions with under three months of stock.

In comparison to the pre-Covid time, there is a significant decline in stock available on the market.”

Bundaberg has a median house price of $505,000; Townsville has a median house price of $435,000 and Rockhampton has a median house price of $400,000.

There were $395,500 and $430,000 median house values in Warwick and Roma, respectively, based on suburb-level values.

Melbourne has a median house price of $1.1 million, while Brisbane’s is $1.1 million.

According to Paliwal, there has been an increase in demand in Queensland due to a tight rental market.

In the REIQ’s Residential Vacancy Report for the March 2024 quarter, vacancy rates were as low as 0% in Queensland, with rental availability remaining dangerously low.

In these regions, rents are rising rapidly, Mr Paliwal said.

“Four of the five regions are experiencing crisis-level vacancy rates, while the fifth region (Gatton) is also below the high-pressure threshold of two percent and significantly lower than its last decade average.

We expect the fast-growing rental prices, combined with the affordable housing prices, to encourage more renters to buy and attract more investors, driving housing values higher.”

Nearly one million Queensland households are suffering from financial stress due to the rising cost of living and housing crisis, according to Digital Finance Analytics (DFA).

It is estimated that more than 320,000 homeowners (45 percent) are under mortgage stress, spending more than 37 percent of their income on home loan payments. Nearly 490,000 tenants — a whopping 72 percent — are in rental stress, spending on average 36 percent of their monthly earnings on housing.

According to Finder, a Queensland school leaver would need to save for 21 years to afford a deposit.

In the past, one income earner and a stay-at-home parent could raise a family in their own home, said Graham Cooke, head of Finder’s consumer research department.

There is no way that wage growth can keep up with the skyrocketing property prices for most people.

Despite the fact that some are able to enter the property market easier with the help of their parents’ bank, not all are able to do so.

Despite both research projects’ dire results, Mr Paliwal said Queensland was still affordable compared to other east coast states.

There are a number of expensive markets in the southeast Queensland (SEQ) region, including Brisbane, Gold Coast, and Sunshine Coast.

“The majority of their hotness comes from incoming migrants from the two major capital cities, as well as from abroad.

There will be a slowdown in house value growth as prices approach an affordability ceiling.”

He said that, on the other hand, the rest of the state is much more affordable.

The median house price outside of SEQ in 23 of 26 SA3 regions is under $650,000, and in 19 it is under $500,000.

The growth in most of these regions over the last 10 years was much lower than the long-term average, so they have a lot of catching up to do.

Many of them are extremely hot because of their affordability, lifestyle, and thriving local economy, so hot that buyers are willing to pay much more than the actual value.

According to Mr Paliwal, Queensland’s economy and population are among the strongest performers among all states, as well as its property market.

“SEQ and the rest of the state, however, have very different markets,” he said.

Forbes Advisor Australia board member Leanne Pilkington, CEO and director of boutique real estate network Laing+Simmons, reviewed this article. Besides being president of the Real Estate Institute of Australia, she was also the longest serving president of the Real Estate Institute of NSW.

Research has revealed what we have all long suspected: owning property is no longer just a dream, it’s an obsession. HSBC bank research shows Australians spend 2.5 hours a week on property, more than twice as much time as they spend at the gym (1.08 hours) or with their parents (0.88 hours).

Australians have turned those hours of obsession into a popular source of wealth building with residential dwelling values rising from $209.4 billion to $10.72 billion in the March quarter of 2024. There is now an eye-watering $10.7 trillion worth of property on the Australian market.

New ABS data from August last year shows that new investor mortgage commitments have grown to 35.3%, the highest level since 2017. This comes amid the RBA’s run of interest rate hikes in 2022. Western Australia and South Australia are attracting investors away from more expensive markets in NSW and Victoria.

According to Adrian Kelly, immediate past president of the Real Estate Institute of Australia, many Australians still view property as a “more stable life raft” than the stock market.

In the wake of the early 2000s stock market crash, Kelly says, many people are more inclined to put their hard-earned savings in bricks and mortar.

The RBA and Australians began to recognize that housing and housing finance institutions could help prevent future crises after the GFC.

It has caused concern among younger buyers and some policy makers, who argue that property’s generous tax breaks have made shelter unaffordable and speculative. In order to make up for a lack of retirement funds, many boomers who retired before 1992 are investing in property.

Regardless, more and more Australians are taking advantage of property’s wealth-building potential. Before you enter the ring, here are some things you should know.

In the same suburb, a $2 million three-bedroom penthouse apartment might rent for $1,500 per week, but a $2 million three-bedroom house might only rent for $850.

“If your intention is to renovate the property or knock it down and rebuild later on, then the rental yield might not be as important as making a profit on the property, therefore capital gains will be more important.

An investor will try to obtain the best possible rental yield on a property purchased to generate an instant source of income.”

The decision between a house or an apartment comes down to what your investment goal is: capital gains or rental yield. There is one major advantage of owning a house on its own title, however: you won’t have to pay strata or body corporate fees.

Are your properties owner-occupied or rented?

Investors who are simply looking for capital gains may choose to live in the properties they invest in. Meanwhile, investors looking for rental yields would have their properties rented.

CoreLogic’s latest research reveals that while the national profit-making sales rate stands at more than 90%, there is a significant difference between owner-occupied and investor resales when it comes to profitability.

During the quarter ended June 2022, investors were 35.8% more likely to experience a loss-making sale. Median nominal gains for resales of owner-occupied properties were also lower ($223,000) than for those for resales of non-owner-occupied properties ($348,000).

The difference between investing in property for residential purposes before selling versus solely investing for capital growth and rental yields is an important consideration for investors. The investor can use it to decide which type and location of property to buy.

Which suburbs are the best?

Once again, choosing what suburbs in Australia are best for investments depends on the investor’s circumstances and goals. In every state, capital city, and regional location, there will be a variety of growing suburbs, so it’s crucial to conduct extensive research. You can only predict so much, even then. As a result of a global pandemic, regional cities boomed?

According to experts, staying within 10km of the CBD can provide both good rental yields and long-term capital gains, depending on your investment goals. Since the pandemic, working from home has become more popular and commutes to the CBD have become less necessary, however, it remains that suburbs near the CBD are well-established and often highly desirable.

Moreover, you should consider the proximity to schools when selling to families; train lines and highways, as noise pollution can affect your property’s value; and other factors of the suburb that may make your property more attractive when it comes to selling, such as a suburb that is close to supermarkets and transport, or a suburb that is close to the beach.

Additionally, many property advisors do not recommend speculative investing in mining towns that are rumored to be seeing a boom in growth, nor do they recommend “hot spotting”, which involves investing in suburbs before they become popular. Despite the chance of getting lucky and buying into a gentrifying suburb, avoid the hard sales talk and hot spotter spruikers.

Property Investing Mistakes to Avoid

As well as avoiding hurdles that may dissuade prospective tenants or buyers, Brandi also advises investors to avoid cutting corners.

“Some investors don’t want to spend money on professional services or due diligence,” Brandi says.

Schnieder agrees that “speaking with financial planners, mortgage brokers, and real estate professionals will help you figure out the best investment property for your investment goals”.

Before investing in an investment property, Schneider suggests asking yourself the following questions:

Are you planning to move within the next few days?

Are you only planning to rent out the property to earn passive income?

Is this your first home purchase?

In order to sell the house for a profit, do you plan to renovate/upgrade it?

What is the maximum amount I can borrow?

Talk to your bank or broker to find out how much you can borrow. Based on the number of people going in on the loan; the number of dependents you have; whether you plan on living in the property first or solely buying it as an investment; whether the property is already built; the state in which you plan to purchase; and your current income, the bank will calculate your borrowing power.

Investing with bank loans is “risky business”, according to the Australian government-backed Moneysmart website. Loans for investment properties are also more expensive than loans for owner-occupied properties.

Borrowing to invest can give you access to more money, but it can also come with more risks, such as bigger losses and higher interest rates.

To determine which loan is best for you, speak with a mortgage specialist.

Property Investing Costs

Investing in property involves many more costs than just the purchase price or mortgage repayments. Below are some common investment costs.

Stamp Duty

Stamp duty, also called land transfer duty, is the cost of transferring a property from one owner to another. It’s a compulsory, state-imposed tax, meaning that the cost of it varies from state to state. The time required to pay stamp duty also varies depending on which state you have purchased property.

Stamp duty is calculated depending on the dutiable value of a property (generally the purchase price or market value of the property); the date of purchase; whether you are an Australian or overseas investor; if the property is a new home, an established home, or vacant land; if it will be your primary residence; and if it is your first property purchase.

To find out how much stamp duty you will need to pay, each state government offers a stamp duty calculator online.

Conveyancing and Search Fees

In a nutshell, conveyancing is the legal work involved in buying a property and the transfer of ownership from the vendor—or seller—to the buyer. It protects the buyer against nasty surprises in the future and ensures they’re aware of any potential issues with the property before they commit to the purchase.

However, conveyancing costs money, and conveyancing fees are split into two parts:

Legal fees charged by the solicitor. According to the Australian Institute of Conveyancers (AIC), conveyancing fees typically vary from $700-2500, although they can be higher for more complex transactions such as leasehold properties. You’ll usually have to pay conveyancing fees even if your purchase fails. Disbursements charged by third parties for various searches and legal documentation. Examples include certificate of title search, mortgage registration, and inspection fees.

It’s important to note that each Australian state and territory is governed by their own individual divisions of the Australian Institute of Conveyancers, and therefore may have different pricing costs and agreements.

Property Inspections

No matter what type of property you are purchasing, it’s paramount that you have it inspected by a qualified building inspector. This will check for minor and major defects, quality of construction, structural integrity, moisture issues and the potential for termites. While costs vary depending on the size of the property and the inspector’s call-out fees, investors should expect to pay between $500-$800.

Additional Ongoing Costs

There are also a multitude of ongoing costs that individuals need to be aware of before investing in property. These include council and water rates; building insurance; landlord insurance; body corporate fees if you are buying an apartment or villa; land tax; property management fees; and maintenance costs.

Final Word

With the initial cost and the ongoing requirements, potential investors need to be aware that investing in property cannot guarantee income.

And while strong demand for rental properties may seem like an enticing prospect to investors, it’s important to do your research, talk with experts and specialists, and consider your personal finances before jumping on the property-investor bandwagon.

As CoreLogic figures, show, while the Australian property market was down in 2022, it has staged a steady recovery over the last year.

The prospect of strong capital growth and rising rents are enticing more investors back into the housing market, with investment loans up almost a third.

Investors, however, are being selective in where they park their money, preferring outperforming markets like Western Australia, Queensland and New South Wales over lagging ones like Victoria.

Australian Bureau of Statistics data on Friday showed the total value of home loans rose by a stronger-than-expected 3.1% to $27.6 billion in March, 18% higher than a year earlier.

A total of $17.5 billion in owner-occupied loans were made during the month, a rise of 2.8% over the previous month.

Investment loans grew by 3.8% to $10.2 billion in March 2023, up 31.1% from March 2023 and approaching record levels seen during the peak of 2022.

The size and number of investment loans have both grown strongly over the past year, according to ABS head of finance statistics Mish Tan.

“This is consistent with historically low vacancy rates over the same period, and CPI rental prices rising 7.8% annually to March quarter 2024.”

The Consumer Price Index (CPI) rose by a stronger-than-expected 1% during the March quarter, according to inflation data released last week.

Nevertheless, PropTrack’s director of economic research Cameron Kusher said the investor resurgence is very much a state-specific phenomenon, with Queensland (+45.3% year-on-year) and Western Australia (+63.8% year-on-year) leading the way.

According to Mr Kusher, these markets are extremely attractive to investors due to their relatively high rental yields and lower prices than Victoria and NSW.

Due to the Reserve Bank’s rapid increase in interest rates during 2022, investor lending substantially declined.

“It is likely that the stable interest rate environment and strong property price increases over the past year, along with higher interest rates improving tax deductibility from investments, low rental stock volumes, and strong rental price increases are encouraging investors to return.”

Since the pandemic, the national vacancy rate has fallen to a near-record low of 1.11%, according to PropTrack.

Despite tight rental conditions, Mr Kusher said investors are still selling out.

It is not clear whether these new investors are renting their properties long-term or short-term, as many investors are exiting the market.

The rental shortage can be addressed instantly with more rental properties and more investors, but it will take some time to show up in the supply.”

In favor of smaller states, investors turn their backs on Victoria

In March, investors borrowed more for housing in Queensland than Victoria for the first time since 2008, as weaker prices and concerns about land tax and tenancy laws discouraged buyers.

Mr Kusher said that lending to investors in Victoria has increased 6.3% over the past year, while lending to investors in Queensland has increased 45.3% over the past year.

Due to higher property taxes in Victoria, people are instead investing in places like Queensland and WA, or in other asset classes instead.

PropTrack’s latest Home Price Index shows Melbourne prices declined by 0.1% in April, which means prices are only 1.1% higher than a year ago and 3.4% lower than the previous peak.

After falling 0.1% in April, regional Victoria property prices remain 0.9% lower than a year ago.

Over the past year, Brisbane prices have surged 12.8%, surpassing Melbourne for the first time in 14 years.

April’s home price changes across the country

There was also a record high in investment lending in Western Australia, where property prices soared by more than 20% in Perth over the past year, and 10% in regional areas. Investor lending in South Australia is also approaching record levels.

According to Mr Kusher, capital cities in these states have seen the highest increases in property values, but they are still cheaper than properties in Sydney and Melbourne.

There is little new housing construction and rental listings are extremely low, making it an ideal investment environment.

The best time to invest in these markets was a few years ago, but investors still see further upside.”

Buyer’s agent Kate Hill from Adviseable cautioned those looking to jump on the booming Perth market without doing their homework.

“Perth has been going bonkers for the past couple of years. When you [buy] and it’s in the media, the bulk of capital growth has already occurred,” she said.

In contrast, she said, ‘smart’ investors were taking advantage of the weakened conditions in the south, given its solid prospects for cash flow and capital growth.

In addition to fewer buyers on the ground, property prices have remained subdued, and Melbourne’s vacancy rate is only 1%,” said Ms Hill.

As a result of the exodus of investors from the state, rents will likely increase, which is a terrible situation for renters.”

There is a hidden gem in South-East Queensland that appeals to nature lovers who need a regular fix of the city.

A quiet community surrounded by the scenic rim of Queensland, Beaudesert combines quiet living with easy access to Brisbane and the Gold Coast.

Earlier this month, the highly coveted Smart Property Investment Fast 50 ranking for 2024 named Beaudesert as one of the top suburbs in Queensland.

It aims to provide unparalleled insight into the Australian suburbs that are set for future growth, based on the insights of an expert panel of 14 and open-source data.

For those seeking a rural lifestyle but wary of being cut off from the big city, Beaudesert has long been a well-kept secret in Queensland’s hinterland.

It is located 70km from Brisbane’s central business district and just under 60km from Surfers Paradise. The town is surrounded by some of the best hiking, camping and rock climbing spots in the region, as well as the pastoral calm fostered by the local farming community.

CoreLogic data shows Beaudesert is well below the median house price of both neighbouring metropolises, yet within easy reach of them both.

There is an average home price of $500,000. The median house price in Greater Brisbane as of April 2023 was $781,881, while the median home on the Gold Coast is $945,000.

Over the past year, properties in the hinterland area have performed well, and consistently in general. The median quarterly growth rate in Beaudesert is 4.20 percent, while its average annual growth rate is 4.9 percent. There has been a 20.70 percent increase in the town’s value over the past year. On average, investors can expect yields of approximately 4.3 percent from rents that hover around $410 per week.

Just over 6,400 people live in the town, and population growth is modest but steady. Recently, two new well-planned residential areas have been established in the town – Brayford Estate, east of town, and Tullamore Downs, north of town.

Mountainous terrain forms the southern boundary of the Scenic Rim, which is dominated by the Flinders Peak Group. This area is home to Lamington National Park, Tamborine Mountain, McPherson Range, Main Range National Park, Mount Barney National Park, and landforms including Cunninghams Gap and Fassifern Valley, which are popular hiking and climbing destinations.

A “traditional” climbing method, operating without bolted routes, has become particularly popular at the Mount French peak, part of the Moogerah Peaks National Park.

There’s no wonder the small town has become a hub for creatives with such inspiring surroundings. In addition to art exhibitions and performances by acclaimed bands, singers, and dance groups, Beaudesert’s cultural hub, The Centre, screens recent release films and hosts film screenings.

Recently, it has become a popular choice among adventure lovers looking for a base to enjoy the Scenic Rim’s spectacular scenery.

In the north of Beaudesert, there is a community arts and information center that sells pottery, crafts, and art.

The Beaudesert Historical Museum in Jubilee Park displays local farming artifacts like vehicles, machinery, and tools dating back more than 100 years, as well as Pioneer Cottage, an authentic slab hut built in 1875.

It has two primary schools, two high schools, a range of aged-care facilities, and is a great place for families. Several daily needs can be met along a bustling main street, including medical services, dining, and shopping.

The Australian housing market is currently so undersupplied that I have rarely seen a supply-demand inflection point like this. It’s only going to get worse.

There are a number of unknowns and risks ahead for our housing markets, but there are also five certainties: 1. RBA expects inflation to persist for a little while longer 2. There will be a decline in interest rates 3. Rental and purchase housing will remain scarce for some time to come. 4. There will be an increase in rents 5. Housing demand will continue to be fuelled by the impressive demographics and strong population growth.

In this way, there is a window of opportunity before falling interest rates result in a resetting of the property market.

There is little doubt that inflation and interest rates have peaked, and in due course consumer confidence will return and the markets will resume their upward trajectory.

In 2024, watch out for these trends:- 1. There will be a continuation of the recovery phase of the property market cycle. 2. Rates will eventually fall, but this may not happen until later this year or early next year. 3. There will be more fragmentation in our property markets. 4. Immigration will continue to underpin our housing markets. 5. There will be a continuing rise in rents.

6. Property market investments will continue to be made by strategic investors. 7. The importance of living in the right neighbourhood will increase. 8. There will be growth in employment and a robust economy.

How do you see the Australian property market for the rest of 2024?

Is the RBA going to raise rates again in 2024 or have interest rates peaked now?

In 2024, will affordability issues result in distressed sales and falling prices or even a property market crash?

After 13 months of rising values in the housing market, people are asking these questions.

Our housing market has defied the many doomsday forecasts and entered a V-shaped recovery early in 2023, making the 2022 downturn one of the sharpest and shortest on record.

With home prices hitting fresh record highs in many markets, the price upturn has now been entrenched for 15 months.

During this period, auction clearance rates are consistently showing the depth of our major capital city housing markets, and FOMO (fear of missing out) is creeping in as house prices reach new peaks.

Consumer sentiment and auction results have historically shown a strong correlation with future housing prices.

Each state is at its own stage of the property cycle, and each capital city has multiple markets.

While some regional areas outperformed the capital cities in 2022, capital city property markets have led the price upturn in 2023 and regional areas had slower growth.

Overall, persistently low supply relative to demand are supporting arising housing values despite high interest rates, ongoing cost of living pressures, worsening affordability pressures and a deeply pessimistic level of consumer confidence.

And after underperforming throughout the pandemic period, unit prices recorded stronger growth for much of 2023 and are still growing strongly this year as affordability constraints will mean more Australians trade backyards for balconies and courtyards.

Here’s what the big four banks forecasting for property prices in 2024

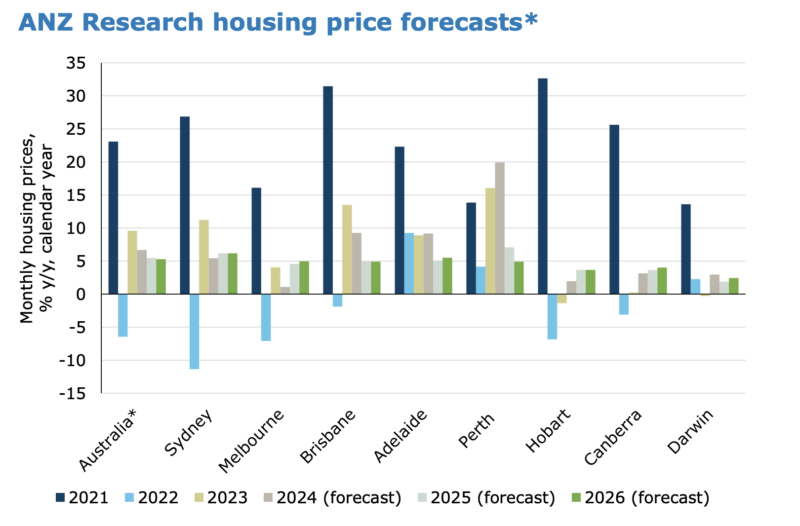

According to ANZ, capital city housing prices will rise by 6-7% in 2024, 5-6% in 2025, and around 5% in 2026. As a result of a longer-running shortage of available homes, Brisbane, Perth, and Adelaide are likely to outperform other cities. Household incomes are expected to rise (first due to fiscal policy) from late 2024 onward.

According to ANZ, capital city housing prices will rise by 6-7% in 2024, 5-6% in 2025, and around 5% in 2026. As a result of a longer-running shortage of available homes, Brisbane, Perth, and Adelaide are likely to outperform other cities. Household incomes are expected to rise (first due to fiscal policy) from late 2024 onward.

CBA expects capital city prices to rise by 5 percent, with small variations across cities. According to forecasts, Brisbane will grow by 6%, Melbourne and Perth by 5%, Sydney by 4%, and Adelaide by 1%.

According to NAB, prices will rise by an average of 5.4% across the capitals. Brisbane prices are expected to rise by 6.5 percent, Perth and Adelaide prices will rise by 6.2 percent, Melbourne prices will rise by 5.5 percent, and Sydney prices will rise by 5 percent. Values in Hobart are expected to remain flat for the remainder of the year.

According to Westpac, the combined capitals will grow by 6 percent. According to forecasts, Perth will grow by 10 percent, followed by Brisbane at 8 percent, Sydney at 6 percent, Adelaide at 4 percent, and Melbourne at 3 percent

There is always a way to beat the averages.

Although there’s a likelihood that property prices will grow a little more slowly in 2024 than they did last year, the good news is that investing in the right property in the right location can always beat the national average.

The next hotspot isn’t what I mean by that.

In other words, I mean buying quality properties in gentrifying suburbs that will outperform over time.

With property, you can increase your results by using your own time, skills, and knowledge – so don’t settle for average.

There’s more to it than just location. It is possible to add value to a property by renovating or redeveloping it.

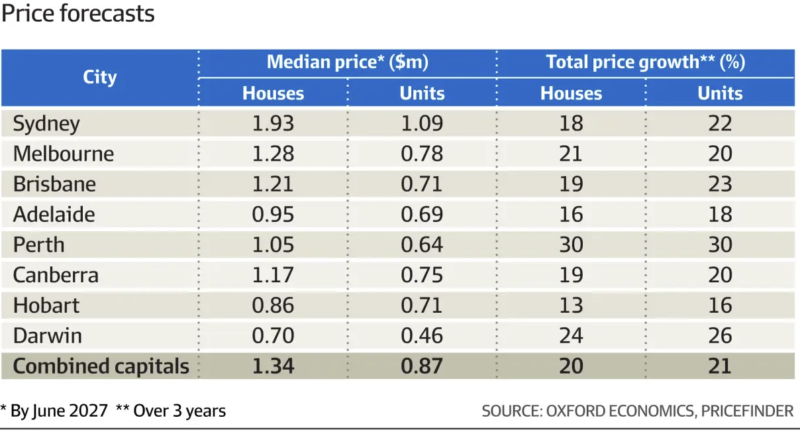

In three years, Oxford Economics forecasts the following house price levels.

How can values continue rising amid high interest rates?

Clearly affordability has decreased, but the housing markets are being underpinned by a number of factors:

Wealthy buyers entering the market with higher deposits.

Downsizers who had a lot of equity in their homes are buying debt free – in fact a third of properties last year were transacted with no mortgage at all.

The bank of mum and dad and inheritances are helping many buyers with a deposit.

Some buyers are buying in cheaper markets while others are buying units rather than houses.

The property room of 2020-21 left many homeowners with significant equity in their homes.

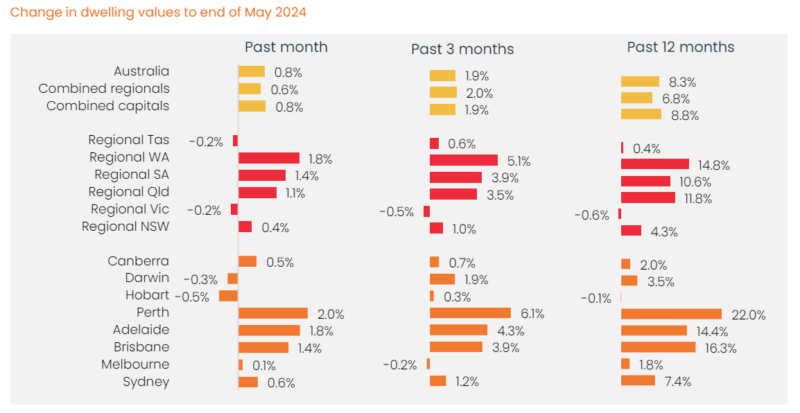

The latest housing market stats

Dwelling values have remained robust as CoreLogic’s national Home Value Index rose 0.6% in February, the strongest monthly gain since October last year.

Here are the latest stats provided by CoreLogic for property price changes around Australia:

As a matter of fact, all research houses reported higher dwelling prices in March 2024:

Home values in Australia continued to rise in May, with CoreLogic’s national Home Value Index (HVI) rising 0.8%, the biggest monthly gain since October last year and the 16th consecutive month of growth.

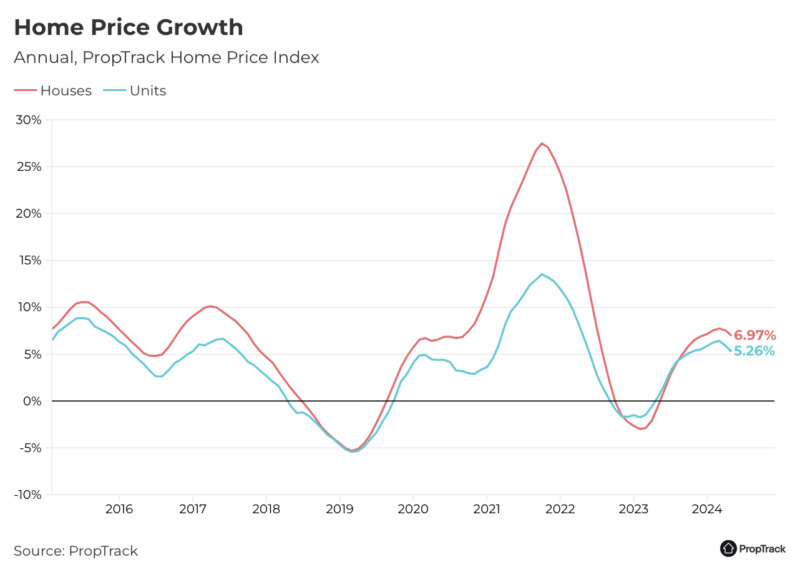

In May, PropTrack reported that national home prices rose 0.3%. They have now risen 6.68 % from May 2023 levels and 9.5 % from December 2022 levels.

According to Dr Andrew Wilson’s My Housing Market, national housing markets recorded steady price growth in May, with the late autumn selling season generally providing positive outcomes for most sellers. In the May quarter, the median house price in the national capital city increased by 0.3% to $1,134,494.

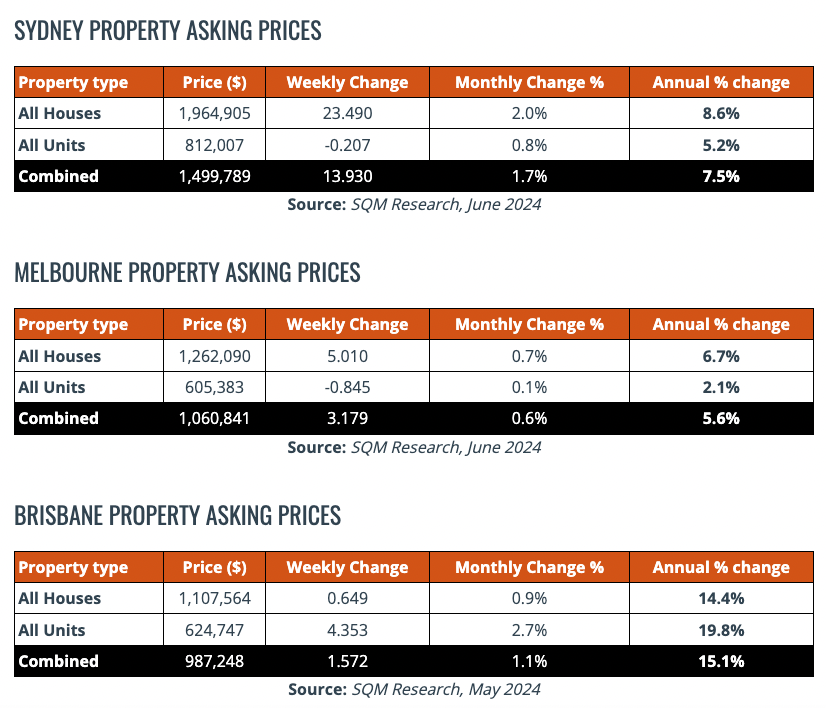

A good leading indicator for the property market is “Asking Prices”, which reflect seller sentiment and expectations for the future value of their home.

Australian property prices: the fundamentals

There are a variety of factors that influence property prices, and as we move through property cycles, they all come into play.

Property values will be driven by a number of factors that tend to boil down to two basic economic concepts: consumer confidence and supply and demand.

It is crucial for one to understand how these concepts work together to affect real estate in the future.

Conversely, if we take a telescopic view rather than a microscopic view of housing over the next decade or two, we will see that demographics (how many of us there are, what we want to live, where we want to live) and wealth will be the two biggest factors driving housing markets.

To begin with, let’s explore some of the key underlying factors that will influence our property markets in the medium term.

1. RATES OF INTEREST/AFFORDABILITY

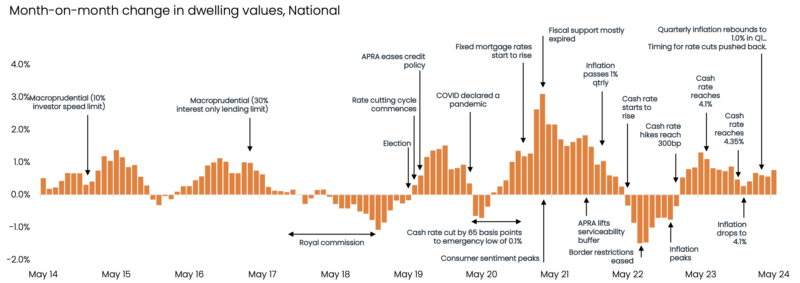

In spite of many people believing that interest rates are a key driver of property values, and that’s why so many pessimistic property forecasts were issued during the rise in interest rates during 2022-23, our housing markets proved extremely resilient and continued to grow despite 13 interest rate hikes from the RBA.

The fall in interest rates and the subsequent increase in affordability are certainly powerful drivers of property price growth, but the reverse is not true.

In addition to interest rates, many other factors influence house prices.

Earlier this year, Australia’s largest lender, the Commonwealth Bank, predicted six interest rate cuts in 2024 and 25 starting in September, but it appears rates will stay high for a longer period of time as inflation remains stubbornly high and our economy and labour markets continue to perform better than the Reserve Bank would like.

In 2024, economists are divided about the timing and number of RBA rate cuts. Some predict three, while others predict none.

For borrowers who have large debts compared to their incomes, the difference between no rate cuts, and up to three rate cuts, can be a huge factor.

2. SUPPLY AND DEMAND

In the short term, housing supply affects house prices greatly: an undersupply causes prices to rise, while an oversupply causes them to fall.

Our lack of new housing construction has led to low vacancy rates and higher house prices despite very strong population growth through 2023.

The strong absorption of new listings for sale has suppressed the total number of listings in the market, intensifying competition among buyers.

A shortage of housing has resulted, outweighing the negative impact of rates on prices.

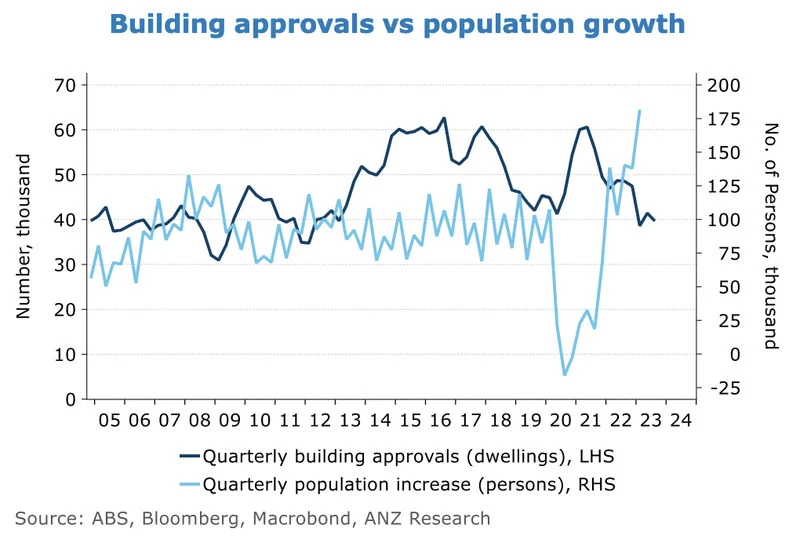

And there is no end in sight as building approvals (which are a good indication of future supply) are running at very low levels.

And just because a new apartment complex has been approved, it doesn’t mean it will get built.

At the moment very few new complexes are coming out of the ground because it’s not financially viable to build them at today’s market prices.

Of course, this means future new developments will have to sell at prices considerably higher than today’s market value and this will, in turn, pull up the value of established apartments.

3. CONSUMER CONFIDENCE

Consumer confidence is a critical factor affecting the direction of property prices.

We won’t make big financial decisions like moving home or buying an investment property unless we feel confident about our economic future and our financial stability.

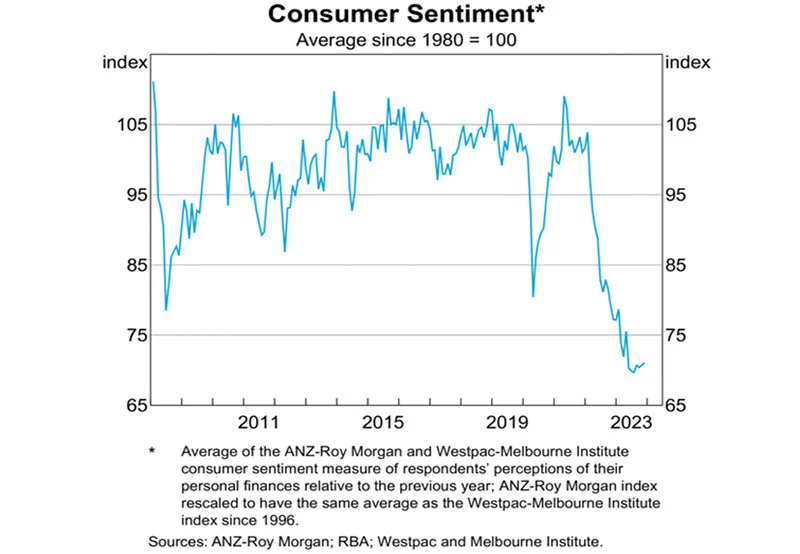

2023 was a year where consumer confidence was at historic lows because of all the economic and socio-political issues that confronted us.

I believe that during 2024 consumer confidence will rise as inflation slowly comes under control and we realise interest rates have peaked and are going to eventually fall.

At the same time, the “wealth effect” a very improving economy and rising property values will lead to further consumer confidence and bring home buyers and sellers back into the market.

4. ECONOMIC CLIMATE

Another key factor that affects the value of the property market is the overall health of the economy.

This is generally measured by economic indicators such as the gross domestic product (GDP), employment data, manufacturing activity, the prices of goods, etc.

Broadly speaking, the economy is strong and the RBA is trying to slow it down to bring inflation under control, but currently, everybody who wants a job can get a job and this will underpin our housing markets even if the economy falters a little moving forward.

5. POPULATION GROWTH

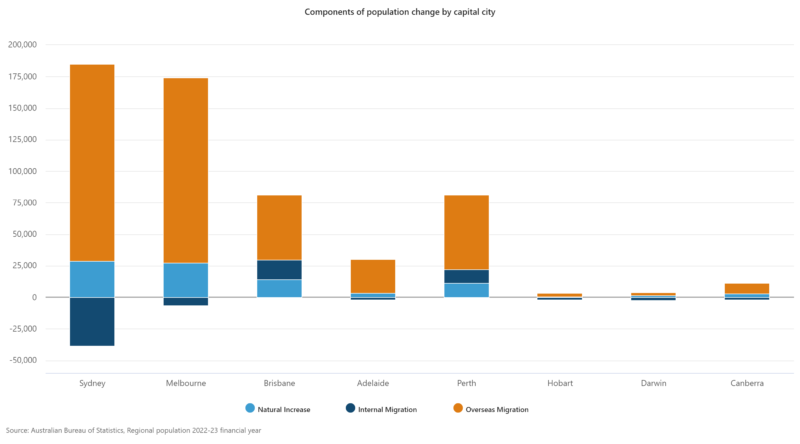

Australia has experienced a record-breaking rate of net overseas migration, estimated to have reached around 500,000 people in the 12 months to September 2023.

While population growth has always been a key driver supporting our property markets, the influx has pushed our supply/demand balance off-kilter and is key to the increase in housing prices and the shortage of rental properties.

6. AVAILABILITY OF CREDIT

When the credit (the ability to borrow from the banks) is readily accessible, with lower interest rates and less stringent lending criteria, it tends to stimulate the housing market since more people find themselves able to borrow money to buy homes, leading to increased demand for housing.

On the flip side, when credit is tightened through higher interest rates or stricter lending criteria (as happened when APRA made the banks tighten the purse strings in 2016-7), the effect can be a cooling of the housing market.

Such measures are usually a deliberate policy response to an overheated market, aiming to reduce the risk of a “property bubble” and subsequent crash.

7. INVESTOR SENTIMENT

This sentiment, essentially the collective attitude and outlook of investors towards property markets, can significantly influence both the demand for and the value of real estate.

Investors generally account for around one-third of all property transactions so positive investor sentiment can drive up property prices, especially in sought-after areas.

Conversely, negative investor sentiment, as occurred during the market downturn of 2022, can lead to a decrease in property values.

If investors believe that property prices will stagnate or fall, they may be less inclined to invest, or they might choose to sell off their properties, increasing supply in the market.

8. GOVERNMENT INCENTIVES

Government incentives can have both direct and indirect impacts on the real estate sector.

One of the most direct ways government incentives affect property values is through policies aimed at stimulating demand.

For instance, initiatives like the First Home Owner Grant (FHOG) or stamp duty concessions for first-time buyers directly increase buying capacity, leading to greater demand for property.

Another aspect is the development incentives provided by the government to promote specific types of property development, such as high-density housing or urban renewal projects.

These incentives can increase property values in targeted areas by improving infrastructure, accessibility, and community facilities, making them more desirable places to live.

Tax policies and regulations also play a crucial role.

Negative gearing can increase demand for investment properties, pushing up prices.

And every time there is talk about removing negative gearing or amending taxes including land tax, investors shy away from our housing markets.

$3.5 billion Big Build spend for Wide Bay in 2024-25

$952 million for the Wide Bay Hospital and Health Service

$786 million towards the Queensland Train Manufacturing Program

New Premier Steven Miles first budget is delivering for the quickly growing Wide Bay region, with more investment into health, infrastructure and education thanks to the 2024-25 Queensland Budget.

The 2024-25 Queensland Budget features a nation-leading $11.218 billion in concession and rebates to provide cost-of-living relief to Queenslanders, alongside a record $107.262 billion capital program for infrastructure statewide.

The Miles Government is putting major infrastructure into the spotlight with Queensland’s Big Build Spend for the region increased to $3.5 billion, generating 9,400 jobs in the Wide Bay.

The Bruce highway will benefit from major upgrades with $5.6 million in 2024-25 to go towards the Tiaro Bypass, and $110.6 million in 2024-25 to construct a new 26km, four-lane, divided highway between the existing Bruce Highway interchange at Woondum, south of Gympie, and Curra.

The regions rich rail history will be celebrated with $786 million going towards the Queensland Train Manufacturing Program, including a purpose-built manufacturing facility at Torbanlea which will deliver 65 new six-car passenger trains.

Community Safety is also front and centre with this Budget dedicated to improving frontline police services.

Including $4.1 million to complete the upgrade of the police facility at Maryborough, $15 million upgrade and enhance the function of Hervey Bay and Bundaberg police stations and additional funding to deliver additional aerial enforcement capabilities.

Premier Miles is continuing to invest in health with a $952 million investment for the Wide Bay Hospital and Health Service to deliver even better access to healthcare across the region.

$68.1 million in funding is to progress the new Bundaberg Hospital which will have more than 400 beds, increasing the number of overnight beds in the region by 121 and an $8.8 million investment towards delivering the new alcohol and other drugs residential facilities in Bundaberg, providing a service that is voluntary for people aged 18 years and over who want to make positive changes in relation to alcohol and other drug use.

As part of the Queensland Energy and Jobs Plan, $116.4 million will go towards the Southern Renewable Energy Zone Battery. The battery will have the capacity to supply 300 megawatts (two hours) of energy into the National Electricity Market, making it one of the largest battery energy storage systems in Queensland.

The Miles Government is continuing to invest in education and will provide $79 million to maintain, improve and upgrade schools in the wide bay, as well as $4.75 million to construct additional specialist classrooms at Kepnock State High School and upgrade the amenities at Biggenden State School.

As stated by the Premier Steven Miles:

“I am doing what matters for Queenslanders delivering the largest investment into Queensland Health services, infrastructure and frontline workers in the state’s history.

“My first budget as Queensland’s Premier is helping unlock the Wide Bay’s potential, from protecting the important heritage of this region to ensuring safe and secure water supplies, new hospitals and upgraded roads and schools.

“I am also delivering more frontline services for the Wide Bay with extra nurses, extra doctors and more ambulance officers.

“I will always put Queenslanders first and do what matters most to them.”

As stated by the Treasurer and Minister for Trade and Investment Cameron Dick:

“With more than $950 million for Wide Bay healthcare, we’ll hire more doctors, nurses and ambos for the region, adding to the 192 extra doctors and 564 extra nurses our government has delivered since 2015.

“With $59.1 million out of a $162.6 million total spend to provide 6,500 training places for eligible Queenslanders who are passionate about healthcare to study the Diploma of Nursing our increased health spending is about ensuring that we provide better services and that Queenslanders can get access to the medical care they need.

“Our ‘Big Build’ infrastructure spend will also support around 9,400 jobs across the Wide Bay and is helping grow the region’s economy by investing in health infrastructure and providing cleaner, greener energy for the community.

“This Budget continues our commitment to improving outcomes for students and teachers in the region, we are upgrading schools in Biggenden and Kepnock to provide these communities with better facilities to enable students to thrive.

“We are also improving accessibility to learning opportunities with new learning spaces, free kindy and fee-free TAFE.

“We are bolstering the Australian Government electricity bill relief by $1,000, meaning that Queensland households will receive $1,300 off their electricity bills.

“This budget was made with Queenslanders in mind, and we will do what matters most for them.”

As stated by Bruce Saunders, Assistant Minister for Train Manufacturing and Regional Roads and Maryborough MP:

“New Premier Steven Miles’ first State budget is doing what matters for Maryborough.

“This Budget will deliver $765 million towards the Queensland Train Manufacturing Program, building a new purpose-built facility at Torbanlea and an additional 65 six-car passenger trains.

“This funding secures local well-paid manufacturing jobs in Maryborough right now and into the future.

“When David Crisafulli and LNP were last in government, Maryborough’s manufacturing heartland was gutted and our region lost hundreds of local jobs.

The LNP does not back local manufacturing and they don’t back Maryborough.”

“The Miles Government’s Budget has delivered even more for our community with a sharp focus on cost of living relief, major infrastructure investment, and job creation for Bundaberg locals.

“Delivering large-scale health and education projects means that this budget has set a blue-print for better services and skilled employment opportunities across the region.

“This is what Labor Governments do, invest in services, invest in infrastructure, and deliver better outcomes for Queenslanders living right across our State.”

As stated by Adrian Tantari MP Member for Hervey Bay:

“I’ll always stand up for the Hervey Bay and fight to get our fair share of funding and infrastructure to keep up our growing region’s needs.

“That’s why I’m so pleased with our new Premier Steven Miles’ first budget which delivers what matters for the Hervey Bay.

“With $28 million for a new Hervey Bay Police Station, $40 million for the Hervey Bay Hospital Expansion and land secured for a new Hervey Bay Fire Station, our new Premier Steven Miles is committed to building a better Hervey Bay.

“But this is all at risk under David Crisafulli and the LNP who have outlined no plans for the Hervey Bay and have neglected our region before.”

Other Wide Bay Budget investments include:

$17.1 million in 2024-25 to support the delivery of the Bundaberg East Levee

$8.2 million in 2024-25 to upgrade the intersection between Hervey Bay road and Pialbla – Burrum Heads road.

$109.6 million to continue planning and enabling works for a new Paradise Dam wall.

$50.2 million in 2024-25 to replace and refurbish handling equipment and infrastructure at Meandu Mine.

PropTrack data suggests Toowoomba real estate market prices in 2028

There is a possibility that the median house price in four Toowoomba suburbs could exceed $1 million within the next five years, according to new data.

REA Group’s PropTrack has revealed how the local property sector may look by 2028 based on its analysis.

Housing affordability remains a persistent problem in Australia’s real estate market.

In recent years, this trend has spread to regional areas such as Toowoomba, where the median house price in wealthy suburbs such as East Toowoomba ($1.388m), Highfields ($1.11m), Middle Ridge ($1.141m) and Kleinton ($1.003m) could exceed seven figures within five years.

A further two areas, Westbrook ($952,000) and Mount Lofty ($956,000), may also be closing in on the figure.

According to PropTrack data, North Toowoomba might have the lowest median price by 2028, at $513,000.

Toowoomba’s growth has been “unusually” strong since the start of Covid-19, according to PropTrack senior economist Angus Moore.

“Over the past five years, home prices in the Toowoomba region have increased by just over 52 percent, compared to 58 percent for regional Queensland overall,” he added.

Although the growth has been a little slower than some other regional Queensland areas, the broader point is that all of these areas have experienced very strong growth.

During the pandemic, we saw very strong demand for homes in southeast Queensland, driving prices up very rapidly.”

It is Toowoomba’s continued growth over the past year that sets it apart from other areas at a time when interest rates are on the rise.

According to him, “we are still seeing strong demand support prices.”.

In the past year, Toowoomba’s prices have risen a bit over 8 percent, which is much stronger than what we have seen in much of the country, where prices have fallen as interest rates have increased.”

Despite stating that the 2028 forecast could be realized, Mr Moore suggested that some heat would eventually leave the market.

“The rapid pace of growth in the past five years – and what it would mean for median prices if it were to occur again – demonstrates how unusually strong the past five years have been,” he stated.

In regional Queensland, including Toowoomba, prices have increased by more than 50 percent since the pandemic began.

To provide some context, prices nationwide increased by 23 percent in 2021 alone.

In 140 years, since 1880, that is the third fastest year of price growth.

This is clearly an unusual growth rate, and we are unlikely to see it again in the near future.”

A new shopping, medical and entertainment precinct has been planned for a fast-growing community east of Toowoomba and one of the tenants has already been identified.

One of the fastest-growing communities in the Lockyer Valley could get even bigger, after plans were lodged with the Locker Valley Regional Council to build a new bulk retail, entertainment and medical precinct at Plainland.

Applicant Plainland Crossing submitted the proposal last week for the 13,000 sqm site, which would include space for five major uses and 160 car parks.

Dubbed Plainland Home and Life, the development will include a bulk retail area, indoor entertainment space, medical centre, shop and food outlet.

One tenant in Pet Stock has already been identified as part of the development application.

The development is next door to the new Bunnings Warehouse and Aldi supermarket and forms part of a major cog in the commercial precinct of Plainland as it expands rapidly.

Hundreds of lots have either been sold or are on the market.

More are to be released in the coming years.

Other major commercial developments to come include a massive expansion of the existing Plainland Plaza to about five times its current size.

According to the planning report by Development Directive, the project would cater to the immediate community being created at Plainland.

“The proposed development represents the highest and best use for the site, as it caters for a range of users and provides additional services and amenity to the residents of Plainland,” the report said.

Reports were also submitted with the application into waste management, traffic impacts, engineering and landscaping.

The Lockyer Valley Regional Council has yet to respond to the application.

There is endless discussion and debate over the state of the Australian housing market around the office cooler, dinner table, and in the halls of parliament.

In particular, housing affordability is now a major concern for many Aussies trying to buy a home.

Many factors affect property prices and the broader housing market, including global and local economics, housing legislation, tax policies, development incentives, migration and demographic changes, and lending requirements.

What is the outlook for the Australian property market?

Despite ongoing economic headwinds, the Australian property market continues to grow.

Despite high inflation, rising interest rates, reduced borrowing capacity, and increased cost-of-living pressures, property prices rose over successive quarters in 2023.

According to Domain data, house prices fell modestly in Melbourne in the first quarter of this year, but they rose in Sydney and all other capital cities except Darwin.

In most capitals, house price growth has slowed, suggesting that the wider property market is losing momentum.

According to experts, the underlying fundamentals of the Australian property market – chronic undersupply of new homes, strong population growth, and a tight rental market – will continue to support demand.

Housing supply will continue to be constrained in the near future as new dwelling approvals plunge to a near 12-year low.

It is likely that a reduction in the cash rate by the Reserve Bank of Australia would stimulate housing activity, while an increase would have the opposite effect.

Many buyers in the market now rely on other sources of financing than home loans, such as family help or cash.

“I wonder if the buyers who have been propping up the housing market will run out if interest rates stay at these high levels indefinitely,” he says.

What are the steps I need to take to get into the Australian housing market?

Getting on the property ladder is no easy feat, and buying your first home can be a challenging experience.

Among the topics covered in Domain’s first-home buyer’s guide are understanding finance language, setting a budget, and securing a mortgage.

But first, you will need a deposit. If you can’t afford a full 20% deposit, there are several ways to buy. It’s possible – and somewhat common now – to buy with just 10%, or even 5%, but you must understand both the risks and rewards of doing so.

For lower deposit amounts, banks can offer lenders mortgage insurance (LMI), which is insurance for the bank in case of default. You may have a parent who would be willing to act as guarantor using equity they have on their own property, or you may be able to access one of the government grants, schemes or discounts.

It is important to know what you can and cannot do when it comes to housing. Consider “rentvesting”, buying in a bridesmaid suburb or teaming up with a sibling or friend. You can obtain pre-approval from a lender or mortgage broker before starting your property search to ensure you know your limit and can move quickly to secure a property.

A mortgage broker can offer advice on saving strategies and tell you what banks look for when approving a loan early in the process.

Once you have pre-approval, it’s time to create a buying brief (your location, budget, preferred property type, “must-haves”, “nice-to-haves” and immediate red flags) and start researching and inspecting properties. Modify your brief based on recent sales in your price range and preferred areas.

In 2024, will house prices drop?

In the first quarter of the year, capital-city housing prices reached record highs in Sydney, Brisbane, Adelaide, and Perth, but declined in Melbourne and Darwin. The combined regional median house price also fell 1%.

As a result of rising costs of living, high interest rates, and reduced borrowing power, the overall rate of house price growth has slowed down in recent months.

Domain chief of research and economics Dr Nicola Powell says quarterly gains are about three times slower than the previous quarter.

However, she adds, it is unlikely to translate into significant price drops this year.

“Prices are still rising, and what it highlights is the lack of supply across the country – and when you consider that building approvals are at 12-year lows, that undersupply will continue to cause pricing pressure.”

What is the best suburb to invest in?

A property’s location is a big part of the investment process and your overall strategy. It needs to suit your goals and budget, and it needs to make financial sense.

When searching for the best suburb to invest in, many experienced and new property investors seek the advice and guidance of an industry professional.

It is still possible to find a place to live across the country even on a first-time homebuyer’s budget.

Investing in properties in another state or region should not deter investors, says Luke Harris, chief executive of Property Mentors.

Some people find peace of mind in driving past it. “But that’s why you have a property manager. Take the emotion out of it. Buy in the suburb that makes sense.”

When looking at prospective suburbs, dive into the data. Take a look at a suburb’s current and historic median house and apartment prices, as well as recently sold properties, if you’re looking for capital growth or rental income. Rental vacancy rates can help you estimate the income a property can generate, while median rental prices can suggest how strong or weak the local rental market is.

Investors can access Domain’s house price reports, rental reports, and other relevant information.

Local amenities like schools, shopping centres, parks, and healthcare facilities can all increase the value and desirability of a rental property. Due to the large workforce that is likely to be seeking homes nearby, suburbs close to hospitals are attractive.

Inquire about future development plans in the area and how they might affect your property as well.

What is causing the rise in Australian house prices?

Demand has continued to outstrip supply, despite stretched affordability and high interest rates.

According to Powell, “we’ve seen strong, strong rates of population growth run into undersupply of housing and a very tight rental market.”.

Despite rising building costs and planning delays, new building approvals have fallen to a 12-year low.

In addition, recent buyers were likely to have equity, cash, or family assistance.

According to Jarden chief economist Carlos Cacho, “the average household is no longer able to afford the average home, so home buyers are skewing much higher in income and wealth.”

CBA’s home borrowers now have a combined income above $200,000, he says, as well as a shift towards buyers with larger deposits and a drop in those with low deposits.

According to him, much of that would be intergenerational wealth transfer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}