As population growth and a lack of homes push up prices in regional Queensland, property values are surging.

Locals say Wide Bay’s beaches, hot weather, and “bang for your buck” properties are particularly attractive.

Property analysts predict the trend will continue.

One coastal region in Queensland is experiencing the most rapid growth in property prices.

In the past five years, property prices in Wide Bay, which includes Bundaberg, Hervey Bay, and Maryborough, have risen between 65-75 percent.

Wide Bay has an “incredibly exciting set of ingredients,” said property analyst Simon Pressley.

A big draw for someone looking to relocate from a big, congested city, such as Sydney or Melbourne, is the cost of housing combined with the lifestyle.

I would argue that it has the best weather in the country.

It’s an economic story, a lifestyle story, and a shortage of housing supply story.”

How does the drawcard work?

According to locals, the boom is due to the region’s beaches, good weather, and large backyards.

After putting two houses on the market in recent years, Bundaberg builder Jake Chappel has experienced growth at work and in his personal life.

It was nice to be on the selling side, he said.

“I feel sorry for the young people who are buying now. But I do not believe [prices] will go down any time soon.

It was probably cheap land and cheap properties at the beginning.

“The climate is usually good. It’s a bit hot right now, but it’s usually pretty comfortable and liveable.”.

As compared to the [Gold and Sunshine] coasts and Brisbane, we have great beaches, great people, and reasonable prices.”

Beaches, good weather, and big backyards are credited with the boon. (ABC Wide Bay: Johanna Marie)

Growth in the market

Over the past five years, Bundaberg’s property values have increased nearly 75 percent to a median value of nearly $480,000, according to CoreLogic’s report.

A jump of more than 67 per cent had occurred at Hervey Bay to over $615,000, while a jump of almost 66 per cent had occurred at Maryborough to almost $395,000.

With a median value of more than $965,000, the Sunshine Coast has overtaken the Gold Coast region for the highest median value in regional Queensland.

Tim Lawless, head of research at CoreLogic, attributed the high prices to Queensland’s strong population growth.

“We’re also seeing an ongoing trend in internal migration rates where more people are looking for regional housing or being driven to the regions due to job growth or affordable housing.”

Mr Lawless, however, said that high property prices were not good news for everybody.

According to him, home owners have built up quite a bit of equity across the market.

On the other hand, affordability is becoming more difficult for those who do not own a home.

“Household incomes haven’t risen near that amount.”

Preparing to pay a premium

The data didn’t surprise veteran Gold Coast real estate agent David Hamilton.

In his work, he has seen those numbers reflected and does not expect the market to slow down anytime soon.

“The big jump was in COVID years. It’s going to keep going up,” he said.

There has been an increase in interstate arrivals cashing in on the Gold Coast market, which he believes is adding to the already tight market.

Byron Bay, Sutherland Shire, or the eastern suburbs of Sydney are no different from us, Mr Hamilton said.

People want to live here and walk to the beach, and they are willing to pay a premium for it.”

Despite a strong year in 2023, Brisbane’s property market isn’t slowing down, and these suburbs could see major growth next year.

According to CoreLogic, Brisbane’s median dwelling price went up 11.9% from 1 December to 1 December. On average, houses were going for $870,000, now only about 7.5% below Melbourne.

Key points

Brisbane’s prestige suburbs are expected to keep growing, where the charm and lifestyle create a demand that never goes away.

The fast-growing Moreton Bay LGA might be a good place to look for a bargain.

Brisbane’s market hasn’t slowed down yet like Australia’s second largest city. Before too long, buying a house in Melbourne will be cheaper than in Brisbane if the current growth rate continues.

One analyst says prices in Brisbane will keep going up in 2024 is Louis Christopher of SQM Research

“Brisbane prices are expected to rise [in 2024]…driven by a recovering Chinese economy with strong demand for base commodities like iron ore,” he says.

Whether it’s mining jobs, the 2032 Olympics or our beaches, Brisbane’s population is set to grow for a long time.

Within a decade, 350,000 people will emigrate to Brisbane, both internally and from abroad, according to consulting firm RSM. Brisbane needs more housing than ever before, said former Deputy Premier Stephen Miles.

A plan is needed to make sure homes are delivered when and where they need to be.

In the 12 months to November, SQM reported the number of Brisbane property listings had fallen 12.6%.

Canberra listings were up 24.4%, Hobart listings were up 22.1%, Melbourne listings were up 4.2%, and Sydney listings were up 3.5%.

Several experts in the real estate industry have helped us pick spots in Brisbane that could be particularly lucrative.

Imagine buying a duplex on your own land at about half the price of a house. Think we’re joking? Think again.

For a much lower price than two similarly situated detached houses, duplexes often produce strong value growth and healthy rental yields.

Here’s a full explanation of how duplexes compare to other types of property and which one could be a better investment.

How does a duplex work?

In a duplex, two homes are joined by a common wall and either exist on a single land title and are owned and sold together, or they exist on separate land titles and are owned and sold separately.

A duplex’s owners must agree to an insurance policy covering both sides.

It depends on the age and jurisdiction of the duplex whether a body corporate is required.

For more information, contact the relevant authority in your state or territory.

How do duplexes and houses differ?

The difference between a house and a duplex is that houses only have one dwelling, whereas duplexes have two dwellings, each with its own entrances.

Is it possible to own half of a duplex?

If the duplex has been divided into two separate titles, you can only buy one half if they are on the same title.

What are the benefits of buying a duplex?

If you are an investor, buying a duplex means you’ll get two rental incomes from one property. If you’re a regular buyer, buying a duplex has several benefits. Building one means you’ll earn almost as much rental income as you would from two detached houses, while saving thousands on land costs, since a duplex requires a lot less space than two detached houses.

If you are a regular buyer, the main benefit is the price tag, which is often half of what you would pay for a similar detached house in the same location. Those seeking a low-maintenance lifestyle in a premium location, such as retirees and downsizers, will be pleased with this news.

“This means you can either get into a better location for cheaper than buying a house in the same area, or, to put it another way, you can buy a house with your own strata land instead of buying an apartment in a similar area without land,” says Eureka Buyers Agents’ Nicole Marsh.

Marsh gives the example of a client with a $700,000 budget who wants to buy a house in a prestige waterfront suburb like Burleigh Waters.

It’s almost half the price for this client to buy a duplex in this premium suburb for under $400,000.

There are also the following perks:

A single adjoining owner rather than a large number of neighbours;

As there is only one duplex neighbor to consult, it’s potentially easy to make changes to your own home;

Marsh says living next door offers the security benefits of having a close neighbor without living “in each other’s pockets.”

Since you own your own land, you don’t have to give away pets;

Absence of body corporate fees could boost rental income;

Your garden requires little upkeep since you own a half-block (300-400sqm rather than 700+sqm).

The benefit of saving lots of money must be weighed against the reduction in privacy.

The following are potential pitfalls:

According to March, duplex configuration is crucial – “I don’t like duplexes with one unit at the back as the back neighbours might walk past your bedroom windows at night” – side-by-side or corner units are better;

Consider buying in an area where duplexes are the exception rather than the rule;

To maximize value, avoid duplexes with different front facades.

Depending on the location, Momentum Wealth’s Damian Collins also believes duplexes are good investments.

A duplex property in the right location can definitely be a good investment option for the right client.

Traditionally, properties with a higher land component value appreciate faster than properties with a lower land component value. People often compare duplexes to apartments.

There are also some downsides to investing in duplexes, according to Collins.

“If you own only one duplex, you are often restricted from doing external work to the property since it is a strata complex. This limits the ways you can make the property more valuable,” he says.

In order to make a great duplex investment, you need to do thorough research, just as you would with any other property you buy.

The rapid increase in Australian property prices during 2020 and 2021 is well known to anyone who has sold or bought a property in recent years. While the RBA lifted the cash rate and mortgage rates increased over much of 2022, property prices fell, even dramatically in some markets. CoreLogic’s Home Value Index recorded a slight rise of .6% across all capital cities in March and a rise of .5% in April-the first such rises in 11 months. Many property experts are already predicting the end of the property slump as prices remain above pre-pandemic levels.

The director of research at CoreLogic, Tim Lawless, noted at the release of the Home Value Index in May that net migration and a shortage of inventory likely contributed to the housing market’s recovery.

“Through the downturn, many prospective vendors have stayed on the sidelines, keeping inventory levels low and giving sellers some leverage at the negotiating table,” Lawless said.

It is believed by many buyers that the rate hike cycle is nearing its end.

It may be contributing to a general perception that the market has bottomed out, and that it’s a good time to buy, according to him.

It is likely that consumer sentiment will improve as interest rates stabilize, which will increase buying and selling activity in the housing market.”

Due to its high housing debt ratio, Australia was recently ranked as the second-highest country for “housing market risk” among 27 countries.

It is widely believed that the property market will crash in the near future. We spoke to two experts to find out their opinions.

A Covid-led Boom

Australian properties are still extremely expensive, despite the fact that they have become more affordable since the pandemic.

The Australian housing market reached its peak in April 2022, when it had risen by about 30%, says Eliza Owen, Head of Research, Australia at CoreLogic. Between late 2020 and early 2022, regional Australia experienced an upswing of about 40%, while capital cities experienced an upswing of about 25%.”

According to Owen, the boom was largely fuelled by emergency low interest rates during the Covid-19 pandemic, which reduced borrowing costs, and by a strong recovery with high demand, low unemployment, and high levels of savings.

The housing market was also buoyed by some preference shifts that occurred during the pandemic, including increased demand for holiday houses, tree-changers moving to regional areas, expats returning, and people wanting more space or their own space after lockdowns.

So Will the Property Market Crash?

Australian capital cities’ housing markets fell by -5% in 2022, according to Domain figures. In Sydney, house values declined by -10.9%, and in Melbourne, they fell by -5.9%. In Canberra and Brisbane, they declined by -6% and -1.1%, respectively.

By the end of spring selling season, most of the damage had been done. Between early 2022 and November, Australian combined capital city property prices fell 6.5%, according to CoreLogic figures.

However, Owen does not consider this a crash.

In my mind, a housing market crash is defined by the loss in value and a loss in mortgage serviceability, when people can’t service their mortgages, and they have to sell, but they can’t get enough money to pay off the loan when they try to sell.” We’re not seeing that right now.

Although the property market was in a downturn over the latter half of 2022, Kilroy says a crash is unlikely due to strong economic fundamentals. The first is demand, with high rents and the return of overseas migration resulting in more buyers. On the supply side, low unemployment is limiting the number of properties for sale, with distressed sales not yet evident.

Check out this article for more information: How to beat the rate hikes

The Impact of Rate Rises

Last year’s property market downturn was largely caused by rising interest rates, according to Kilroy. There is a credit availability issue driving this downturn, rather than an increase in unemployment or oversupply.”

After raising interest rates ten consecutive meetings beginning in May of 2022, the Reserve Bank of Australia raised the cash rate to 3.6% in April before holding it steady.

According to Owen, this is the fastest rate increase since the early 1990s as a result of extremely high inflation levels. A major cause of this correction in housing values has been the rise in interest rates, so this has essentially reversed the upswing in housing prices.”

Is 2023 going to be a year of rate declines?

What Is in Store for the Property Market?

In Owen’s words, “prices will continue to fall as long as interest rates rise”. Her research indicates that the magnitude of the declines has moderated in recent months, with a national drop of 1.6% in August slowing to a fall of 1.2% in October. Over the past few months (of last year), there has been a slowdown in the pace of decline, and an orderly trend is beginning to emerge.”

Then, of course, there was the slight rise in CoreLogic’s dwelling values in March of .6% and .5% for April, indicating that we may have reached the bottom of the falls.

Owen says the best guide for the housing market outlook is the cost of debt, with property prices likely to increase once interest rates start to fall, something Kilroy is expecting in either the last quarter of 2023 or the first quarter of 2024.

However, Kilroy adds that since the boom was fuelled by the unique circumstances of a global pandemic, property prices aren’t expected to bounce back to their previous highs in the short term, as interest rates are unlikely to fall as far. She is forecasting any fall in interest rates to bottom out at around 2.6%.

How Far Will Prices Fall?

“We’re expecting a nationwide dwelling peak-to-trough price fall of 11.5%, and we’re expecting that trough to be met in the second half of (2023),” Kilroy says, adding that BIS Oxford Economics forecasts are “at the low end of the scale compared to some commentators”.

However, the same falls will not be experienced universally.

“We’re forecasting a 13% fall for houses and 8% for units, and we’re forecasting Sydney to have the greatest fall in house prices of around 18%, while we have Perth houses at the other end of the scale with a more modest 4% drop.”

While CoreLogic doesn’t make forecasts, Owen says that the Big Four banks are tipping combined capital cities prices to fall by a median of 16%. “Based on the forecasts, this could be one of the largest housing market downturns that we’ve observed, but this is coming off the back of one of the biggest upswings we’ve observed in Australia’s housing market as well.”

However, by late April, ANZ had updated its forecast, downgrading its prediction of a peak-to-trough fall from 16% to 10%. In May, the big four all released revisions of their earlier housing price predictions, reneging their previously pessimistic takes.

Domain economist Dr Nicola Powell said there were signs that the bottom had been reached, and the turnarounds of the banks could be a strong indicator.

“This could very well be the bottom of the market, but we need another couple of quarters of sideways movement of prices, or slight improvements, before that is confirmed,” she said.

Whether this is the bottom or the beginning of another boom is yet to be seen, and, alike to the economists, the banks are split: CBA predicts prices to rise 3% in 2023; NAB expects a slight fall in the year; ANZ and Westpac say the market will be mostly flat for the rest of the year.

Is Australian Housing at Risk?

Most recently, the IMF released a report, A Rocky Recovery, that ranked Australia second only to Canada in relation to housing risk. It did so after looking at five key metrics:

Outstanding housing debt to household income in June last year. Australian housing debt is roughly 145.4%, of the country’s total disposable household income.

The share of housing debt on variable interest rates. Around 70% of loans are variable in Australia.

The share of home owners with a mortgage—around 37%.

Cumulative cash rate changes from March 2020 to September 2022. The RBA has hiked rates 10 times since April last year.

Real house price growth between March 2020 to March 2022, which in Australia amounted to a pandemic surge of about 25%.

Commenting on the IMF report, Owen said that while the ranking is sobering, there is reason for optimism.

“Many households have accrued strong savings buffers through the low interest rate period, and labour markets remain extremely tight,” Owen said.

“Housing market conditions are turning a corner amid low stock levels, rising demand from overseas migration, and consumer sentiment shifting higher as we approach what may be the end of the rate-tightening cycle.”

As the IMG said in its report: “In most cases, it is unlikely that an ongoing fall in house prices will lead to a financial crisis, but a sharp drop in house prices could adversely affect the economic outlook.”

The top 20 locations in Australia for property investors with a $100,000 deposit have been revealed, with seven suburbs in Newcastle included in the list.

Online research company Suburb Help has identified 20 locations in its $100k Investment Report. It includes nine suburbs in NSW, six in the ACT, two in South Australia, two in Victoria and one in Tasmania with a mix of both metro and regional locations.

To make sure locations were suitable for investors, suburbs were excluded if they had a:

Median price above $1m

Owner-occupier share of 65% or more than 90%

Renter share less than 10% or more than 35%

Vacancy rate more than 1.5%

Yield less than 3%

Median weekly rent that has increased by less than 5% over the previous 12 months

This process excluded the vast majority of suburbs in Australian, leaving just a small number of investor-grade suburbs. Suburb Help then whittled the suburbs down to a top 20 and ranked them based on median price (from lowest to highest).

“The cheapest median price is just $590,000, potentially making that suburb accessible for an investor with a deposit of $59,000,” said Suburb Help chief property strategist Veronica Morgan (pictured above left).

Morgan said it was not easy to buy a property right now for a couple of reasons.

“First, even though prices are declining in many parts of Australia, they’re still elevated following the recent boom,” she said. “Second, investors’ borrowing power is declining with every Reserve Bank rate hike, so it’s good to know that if you find a lender prepared to accept a 10% deposit, you can still buy into a good investment location for a relatively modest price, provided you do your research.”

Morgan said every location in the Suburb Help $100k Investment Report had been carefully selected.

“We wanted locations that were not only likely to record above-average capital growth over the long-term but would also provide a healthy cash return right now,” she said. “That’s why we limited ourselves to locations that had low vacancy rates and reasonable yields. As a result, if you buy a quality property in one of these locations, you should find it relatively easy to secure a reliable tenant prepared to pay a good rent.”

Brenden Lowbridge (pictured above right), director of Newcastle brokerage Money Links, said investors could enjoy the benefit of investing in a growing area close to Sydney.

“We have an affordable price point when compared to Sydney along with excellent lifestyle benefits, increasing rents and very tight rental vacancy which has provided the perfect storm for Newcastle and Lake Macquarie,” Lowbridge said. “Investors have also seen that capital growth in many cases over this last growth period has kept up with Sydney suburbs.”

Lowbridge said he had noticed an increase in investor clients wanting to purchase in Newcastle.

“I have noticed there are more experienced investors using the current negative market sentiment to their advantage,” he said. “We just assisted an investor purchase a unit in the beachside suburb Merewether for $650,000. There are many comparable sales from six months ago that are in the $720,000 range.”

Lowbridge said he forecasted this trend to continue.

“I believe when interest rates level out later this year, confidence will return and a larger wave of buyers will come into the market,” he said. “I also believe that a big reduction in construction starts due to build cost increases will put more pressure on existing rentals, meaning an increase in rental yields. Investors will be attracted to these improved yields and push into the market.

“Whilst people have transitioned to Newcastle from Sydney, due to limited employment opportunities I believe that this has been slow to begin with. As large national employers start to consider these areas as an option and employment opportunities present themselves, migration will really kick in which will push up local rents and prices.”

Interest rates’ limited impact is what prevents them from reducing real estate values, but for investors, Sydney and regional NSW may provide investment opportunities.

There should be more equitable distribution of pain among people with mortgages as opposed to the current interest rate strategy.

As expected, the Reserve Bank of Australia (RBA) held interest rates this month.

A softening of inflation figures presented the opportunity, and the Governor cited the need for “time to assess the state of the economy, the economic outlook and associated risks” in maintaining the cash rate.

There is, however, a risk of more rate pain in coming months unless a definitive downward trend is evident.

Although the RBA promotes the notion that rates are its only weapon against inflation, other tools are available to it as well.

In addition, there should be a better alignment of monetary and fiscal policies, consideration of whether the pain of reaching 2 to 3 percent inflation outweighs the benefits, and whether the definition of inflation should be revised, excluding housing costs and profiteering from some companies, for example.

Property prices are less affected by interest rate hikes than if wider measures were taken to combat inflation, since around a quarter of transactions are made in cash, including those made by downsizers and the wealthy.

In spite of rising rates, property prices remain stable

Price increases are typically dampened by rising rates, and this has once again happened. While the price rebound has gathered momentum in recent months, the extent of house and unit price increases has been mild. Rate rises have contributed to this tempered rebound.

Who knows where prices would have been had rates not risen so sharply and consistently over the last year.

Demand remains incredibly strong. Tweaks to stamp duty exemptions for first home buyers in New South Wales have just come into effect to add further pressure to the demand side.

On the supply side, the NSW Government has made various announcements, including developer incentives to include affordable housing as part of their projects in exchange for a more efficient approval process and extra building heights. In response, many councils have predictably hit out at their planning powers potentially being diminished.

If and when work on new supply starts on the ground, there may be some attractive opportunities on offer for investors. But for now it’s just all talk.

The critical shortage of rental accommodation and influx of immigration continues to widen the gap between rental supply and demand. Data from the Rental Bonds Board paints an unambiguous picture of the supply constraints on the rental front.

Almost without exception, one bond held by the Rental Bonds Board equals one rental property.

In NSW, the total residential bonds held as of 30 June 2023 was 961,471. As of 30 April 2023, it was 961,946. Over the past five years we have seen a decline in the growth of rental properties and now it’s going backwards.

Take a moment to consider the implications of this reduction. Of the tens of thousands of people who have needed to find a rental property in the last three months in the state, including the many who have arrived from overseas, sadly a lot have been unsuccessful.

The actions of Government in consistently targeting landlords with new regulations and legislation as apparent solutions to the rental crisis are having an obvious detrimental impact on renters.

Slipping regional areas on investors’ radars

There’s an interesting trend playing out in the regions. Some markets that were the darlings of the pandemic have come back to earth a bit. It’s not entirely unexpected and nor is it cause for alarm, as prices now compared to pre-Covid are still significantly higher.

CoreLogic’s Tim Lawless said recently: “After regional population growth boomed through the worst of the pandemic, internal migration trends have normalised over the past year, resulting in less housing demand across regional markets.”

The fact overseas migration is typically focused on the capital cities is having an impact too. In regional New South Wales, the decline in housing values from the recent cyclical high is nearly 10 per cent, according to CoreLogic.

For investors, who have been thin on the ground of late, it’s a trend that may be worth keeping an eye on, particularly in areas where easing prices correspond with new infrastructure investment. A return to growth may not be imminent in the short-term but nor is a major correction likely given the weight of demand and undersupply of homes.

Like CBD rental vacancy, regional vacancy remains extremely tight. REINSW figures for May 2023 put Sydney’s rental vacancy rate at 1.4 per cent while for the Hunter it’s 2.0 per cent and for the Illawarra 1.8 per cent.

A vacancy rate of 3 to 5 per cent is considered healthy, as it represents a balance of choice for renters and strong fundamentals for investors.

But both in Sydney and regionally, we’re still a long way from that balance.

A BIG country town famous for its golden guitar, another dubbed the beef capital, and a holiday hotspot ranked the country’s least liveable city have been named in a list of cheapest places in Australia to buy property.

A new report by leading property analyst and Hotspotting director Terry Ryder suggests investors seeking affordable property with prospects in the next six months should look further afield than their own backyards.

The Hotspotting report names five regional ‘cheapies with prospects’ across the country that meet the criteria of having affordable buy-in prices, solid rental returns, potential for price growth and growing populations.

It comes as new figures show Australia faces a population boom fuelled by a rise in net overseas migration of up to 1.755 million by 2028.

Regional areas are predicted to grow at phenomenal speeds, particularly in Queensland as migrants form NSW and Victoria seek out more affordable living options.

Hotspotting director Terry Ryder said the report featured five regional locations where investors could readily find properties in the $200,000s or $300,000s, and which also had solid growth potential.

“They’re not that hard to find because regional Australia is full of locations with good growth prospects and solid properties in the $200,000, $300,000, and $400,000 price brackets,” Mr Ryder said.

“They are regional centres which share characteristics of low prices, solid rental returns, and the potential for price growth. In fact, many of these areas can match the best capital cities for capital growth over time.”

Hotspotting general manager Tim Graham said many regional areas had outperformed the big cities in the past three years.

“Affordable prices, higher yields and superior growth: it’s a win-win-win situation for investors,” Mr Graham said.

“Of course, not every regional centre in the nation is a future hotspot. A location needs to have more to offer than cheap real estate to be featured in this report — it must also have growth drivers likely to lead to capital growth over time.”

Dr Laura Crommelin, Senior Lecturer in City Planning at the School of Built Environment at the UNSW said some regions had experienced a significant influx of new residents in recent years motivated by cheaper, more spacious housing on offer.

“Some who are priced out of the city housing markets may be able to afford a more spacious, standalone dwelling in a regional area,” Dr Crommelin said.

“Those regional areas within striking distance of the city are increasingly popular with those who still might commute once or twice a week to the city for work, but spend most of their time living by the coast.”

Dr Crommelin said demand for affordable rental properties was also exceptionally high in some regions.

-AUSTRALIA’S TOP 5 CHEAPIES WITH PROSPECTS-

Rockhampton, Central Qld

Affordable housing

Revitalised CBD

Billions in renewable energy projects

$2.5 billion Shoalwater Bay Military Training Centre redevelopment

$1.1 billion Rockhampton Ring Road

$983 million River Fitzroy to Gladstone water pipeline

$495 million Lower Fitzroy River weir

$575 million master planned estate.

Mr Graham said Rockhampton’s affordable property market had been relatively unaffected by the pandemic.

“This resilience, plus the roll-out of several significant construction projects, are turning Rockhampton into a magnet for southern migrants, first homebuyers and investors,” he said.

“Demand for properties is high and vacancies are tight — below 1.5 per cent in most Rockhampton postcodes.”

Mr Graham said Rockhampton’s diverse economy was being boosted by the resources sector with construction of the Bravus (formerly Adani) coal mine well under way.

Tamworth, Regional NSW

Strong future as regional freight hub

High population growth

$210 million hospital upgrade

$1.3 billion Dungowan Dam project

$37 million University of New England Tamworth CBD campus

Mr Ryder said Tamworth continued to grow, with billion-dollar infrastructure projects rolling

out.

“With its intermodal freight hub, Tamworth Global Gateway Park is set to be one of the engine rooms of the New England economy,” Mr Ryder said.

“The city is also part of a significant emerging region for renewable energy developments, with projects worth more than $10b on the horizon, including a Tamworth Big Battery.”

Mr Ryder said Tamworth was also appealing for its affordability and rural lifestyle, and along with its space and established facilities.

“A wave of new residential developments is also now under way, or in the pipeline, throughout the LGA and in nearby areas,” he said. “The Tamworth property market is strong, with low vacancies and the consistent delivery of high rental yields continuing to attract investors. Units are also recording double-digit annual growth of 20 per cent and above.”

Mount Gambier, Limestone Coast, SA

Affordable housing

Low vacancies and rising rents

$120 million renewable energy plant

Forestry industry development hub

Timber plant expansions

Hotel upgrades

Mr Graham said Mount Gambier was rated one of the best regional centres in South Australia for property investment due to its affordable housing, lifestyle opportunities and employment growth.

“Forestry is also one of the key industries in the region with expansion plans in the pipeline for several of the region’s largest employers,” he said.

“The region has also become popular with interstate and intrastate residents moving to the Limestone Coast.”

With a median house price of $375,000 and yields above five per cent, Mount Gambier is a location worth considering by investors seeking affordability, notable cash flow and prospects for growth, plus rental availability is extremely tight, with vacancies staying below one per cent since 2020, he said.

Lockyer Valley, Regional Qld

Strategic location between Ipswich and Toowoomba, with good road links

Strong, diverse economy including manufacturing, agriculture, tourism,

resources, and government admin

$11 billion Inland Rail Project

$245 million water distribution plan

$180 million food processing plant

$110 million Equine Precinct

$100 million Lockyer Energy Project

The population in Queensland’s Lockyer Valley, halfway between Brisbane and Toowoomba, is expected to grow by more than 37 per cent by 2046, jumping from 41,000 now to 57,000, according to new population figures.

Mr Ryder said the region was rated among the top 10 most fertile farming areas in the world.

“The area is also home to light industry and a Queensland University campus, is at the gateway to the Surat Basin mining precinct and has a growing renewables sector,” he said.

Good road links and a scenic backdrop of the steep hills and mountains meant the area’s natural beauty and rural charm attracted visitors and residents from across the state and beyond, he said.

Geraldton, Regional WA

WA’s second largest port

Largest WA city north of Perth

Australia’s windsurfing capital

Major mining centre

High-speed train to Perth proposed

Commercial activity hub

Affordability and rising sales activity

Very low vacancies

The only city on Western Australia’s Coral Coast, and the largest north of Perth, Geraldton is a key regional centre that has grown swiftly in recent years, in line with growth in Perth and the State overall.

“With an increasing population and growing economy, there has been a notable increase in the LGA’s property market,” Mr Ryder said.

“Geraldton experienced a marked uplift in sales activity in this period that was partly due to budget prices when compared to Perth, with houses typically priced in the $300,000s.”

Earlier this year, Geraldton came last in a study by Avenue Perth of the most liveable cities in Australia, based on safety, average cost of living, number of banks and number of restaurants.

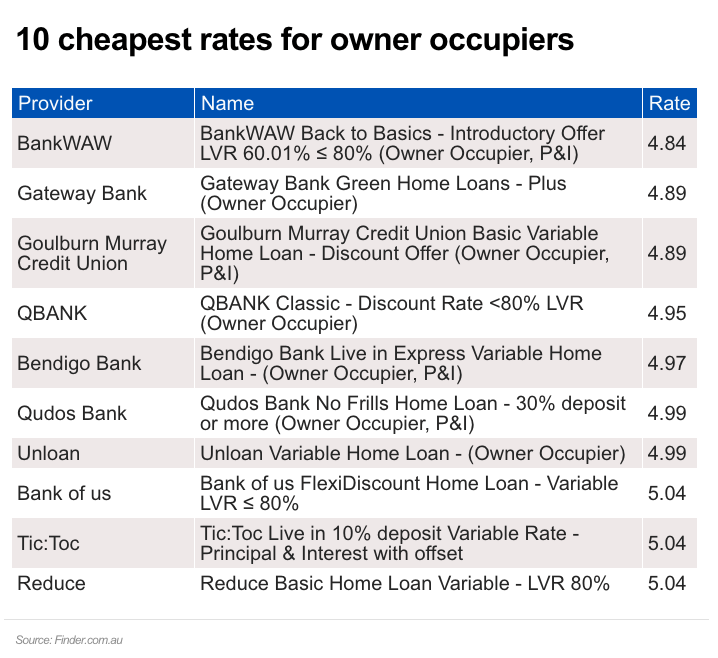

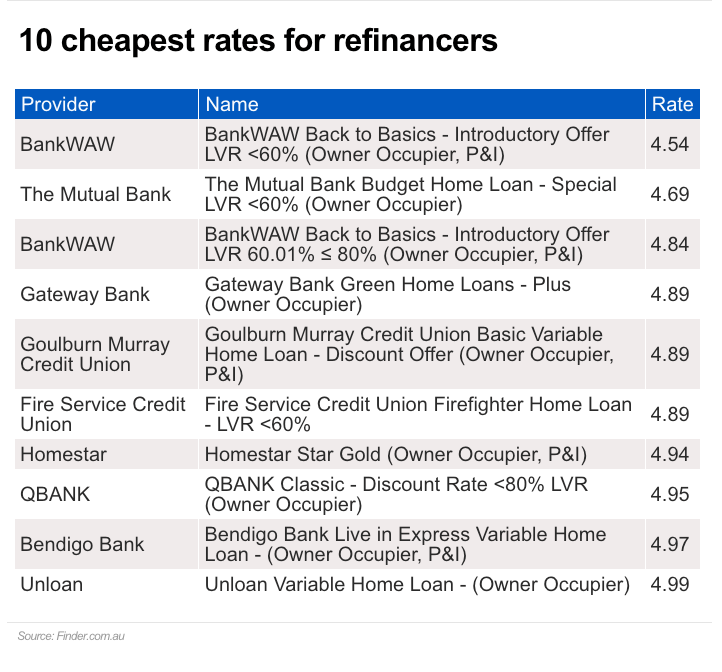

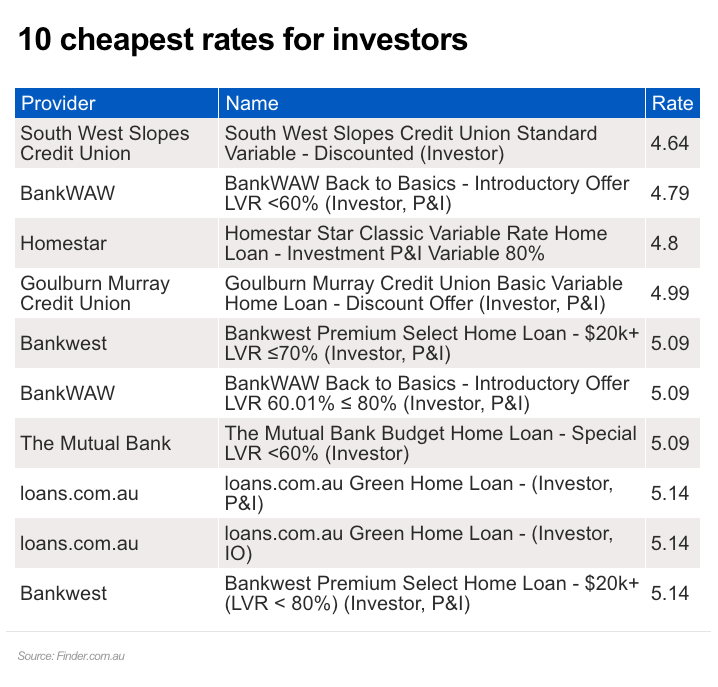

As the RBA pauses rates, savvy homeowners, buyers and investors can save plenty over the course of their loan. See the best deals and use our calculator to work out how much you will pay.

Property owners and buyers have a window of opportunity to get loans at interest rates below 5 per cent following the Reserve Bank’s decision to put the cash rate on hold this month.

The Reserve Bank of Australia announced at its Tuesday board meeting that it would hold off raising the cash rate again, but it also noted that “global inflation remains high” and this could “lead to tighter financial conditions”.

With further rate rises still a possibility, analysis from comparison group Finder.com.au showed only a handful of loan products were still on offer with a rate that had a four in front.

The cheapest loan product currently available for new home buyers was 4.84 per cent, while the best rate being offered for refinancers was 4.54 per cent.

The cheapest rate for investors, who usually have to borrow at a higher rate than owner occupiers, is 4.64 per cent, according to the Finder.com.au study.

The bulk of the cheapest loan products were from lenders outside of the big four major banks.

Finder.com.au head of consumer research Graham Cooke said mortgagees shopping for the cheapest loans needed to be wary of focusing solely on the interest rate.

This was because products with low rates could often have added fees, while other features such as the minimum deposit required were critical components of the loan.

“Consumers may find it tempting to look for a minimum deposit under 20 per cent, however borrowers should be cautious of buying a property with such a low deposit,” he said.

“Firstly, it can dramatically increase the interest cost of your loan over 30 years.

“Second, in a declining market it narrows the gap between the value of your loan and your home – opening up the potential for borrowing to go into negative equity.”

Mr Cooke said that some lenders have introduced cashback offers which reward consumers for taking out a mortgage by giving them dollars back into their bank account.

These products also required caution, he said.

“There are a number of loans with competitive rates that offer up to $4000 cashback. This could be a welcome boost at a crucial time, but pay attention to the details before signing – don’t get distracted by the bells and whistles.”

It comes as economists continue to speculate whether the Reserve Bank of Australia has finished its current cycle of cash rate rises.

Ahead of the central bank’s April board meeting, a panel of 42 economists and market experts polled by Finder was split on the prospect of another rise, with 62 per cent believing there would be another increase.

Among them was economist Saul Eslake, who noted that high inflation and increasing rates in other countries such as the United States would force the RBA’s hand.

“On balance, and noting the increases in rates by the Fed, the (European Central Bank) and (Bank of England) over the past month, I suspect that the RBA Board will come to the view that the case for a ‘pause’ at this meeting isn’t sufficiently persuasive,” Mr Eslake said.

The University of Tasmania’s Mala Raghaven said living costs were rising too quickly for the Reserve Bank to hold rates.

“Though the monthly CPI indicator shows signs of slower growth in goods prices, the costs of essential items such as housing, food and non-alcoholic beverages are still way above the target rate,” she said.

“Households in the lowest wealth and income quintiles face significantly more financial stress than those in higher quintiles. Therefore, given the rising cost of living, the RBA is expected to tighten the monetary policy in April in its effort to tame inflation.”

Many of the economists who predicted the RBA to put rates on hold argued that there may a need for the bank to reflect on the impact of previous increases.

“It makes sense for the RBA to wait in this new risky financial environment,” said University of Sydney economist Cameron Murray.

RBA governor Phillip Lowe said in a statement following this month’s board meeting it needed to assess the impact of earlier rate changes.

“The Board recognises that monetary policy operates with a lag and that the full effect of this substantial increase in interest rates is yet to be felt,” he said.

“The Board took the decision to hold interest rates steady this month to provide additional time to assess the impact of the increase in interest rates to date and the economic outlook.”

When Diana Eloise Binay and her partner got just two weeks to vacate their Sydney rental property a couple of months ago, they knew they would have to compete hard to get another rental property.

“We didn’t have much time to find another rental home, so we decided to offer 10 per cent to 20 per cent above the asking rent in each of the properties we applied for, but we were outspent by the competition most of the time,” Diana says.

Diana Eloise Binay was forced to offer up to 20 per cent above the asking rents to secure a rental home. Louie Douvis

“We ended up getting approved for a unit in Belmore, about 11 kilometres south-west of the CBD, but it was tough to find something that’s liveable and reasonably priced. We have to stretch our budget to afford this one.”

Rents are exploding across the country, and the latest influx of Chinese students is set to make the situation worse for tenants such as Binay.

“We are already in a rental crisis which few people dispute how bad it already is,” says Louis Christopher, SQM Research managing director.

“Market asking rents have risen by 37 per cent on average since the start of 2020, so as a proportion of wages, market rents are at record highs. With the now expected influx of international students, market rents are likely to keep rising at an accelerated rate.”

Rent surge

Without new properties coming to market, the situation is likely to get worse, says Steve Mann, CEO, UDIA NSW.

“Rising rents are purely representative of demand outstripping supply. We simply do not have enough rental properties to satisfy people’s needs,” Mann says.

In the past 12 months, rents surged at a record-breaking pace of 14.6 per cent for houses and by 17.6 per cent for units as vacancies plummeted to their lowest levels ever, Domain data shows.

“Low supply is driving a landlords’ market across all capital cities, worsening an ongoing rental crisis in many parts of the country,” said Nicola Powell, Domain’s chief of research and economics. “The continued growth in asking rents, along with increasing demand, exacerbates a highly competitive environment for tenants.”

Sydney-based landlord Free Morrison said he was surprised to get $50 more a week on his newly purchased apartment in Kensington, 4 kilometres south-east of the CBD.

Sydney-based landlord Free Morrison says he was shocked to get $50 more rent on his new investment property. Louie Douvis

“I was blown away by the strong demand from renters. We had about 40 people applying on the first day alone,” the 27-year old investor says.

This comes as vacancy rates nationwide slumped to a record low 0.8 per cent in January, with Sydney and Melbourne falling to 1 per cent after a seasonal rise to 1.4 per cent in December. Brisbane, Perth and Adelaide all fell below 1 per cent, while Canberra and Darwin dropped to 1.5 per cent and 1.3 per cent respectively.

“These ultra-low vacancy rates are simply not healthy, and it’s a nationwide issue, not just Sydney or Melbourne,” says Dr Michael Fotheringham, managing director of Australian Housing and Urban Research Institute (AHURI).

“A healthy rental market should have around 3 per cent vacancy rate to allow for a churn of people moving in and out of the rental market.

“When it drops to 1 per cent or below, there’s just not enough stock available for people, and we’ve been sitting around the 1 per cent mark for about nine months now, something which we haven’t seen before.”

ANZ senior economist Felicity Emmett says a dominant force fuelling the rental crisis is the increased demand that started during the pandemic.

“What we saw in the pandemic was a significant lift in demand for housing created by the shift to working from home which gave people laser focus on living arrangements,” Emmett says. “People shifted to smaller households, which has also offset the lack of overseas migration.”

The extraordinary rise in house prices during the pandemic has also priced out many aspiring homeowners and forced them to rent for longer.

“First home buyer activity has halved since moving through near record highs in January 2021, implying more Australians are staying in the rental market,” says Tim Lawless, CoreLogic research director.

“Additionally with the migration program for 2022/23 rising from 160,000 to 195,000, that’s an additional 35,000 people that will need shelter, with a large portion likely ending up in the rental market. This has probably driven rental demand higher than normal.”

Decline in supply

But supply has been progressively declining for some time, and there are no signs new rental homes are being added to the market according to Lawless.

“Private sector investment, which is the main contributor to rental supply in Australia, has generally been trending lower since 2015, apart from a temporary surge in investment during the recent phase of strong capital growth in housing values,” Lawless says.

“Investors have seen additional disincentives which have probably contributed to the supply shortage of rental accommodation, including a substantial reduction in their ability to depreciate assets since July 2017.

“There have been a raft of state-based regulations focused on providing fairer outcomes for tenants which may also be causing investors to think twice about property as an asset class.”

Landlords have also been slugged with up to 0.62 percentage points higher mortgage rates than their owner-occupier counterparts since 2015 when APRA tightened investor lending.

Focus on homeownership

Nicholas Proud, chief executive of PowerHousing Australia says Australia simply hasn’t built enough homes over a sustained period, and policy has been geared towards homeownership.

“There simply are not enough structured affordable rentals in the market,” he says. “The past 40 years has seen a substantial lack of investment in social housing. In 1981, around 4.9 per cent of Australian households were in some form of social housing. That number is now 3.8 per cent. Just to get back to those levels we would have to create an additional 100,000 new social housing dwellings.”

Based on the 2021 Census, only 12.2 per cent of rentals were owned by a state/territory housing authority or community housing provider, down from 13.7 per cent in the 2016 Census.

“In the broader housing market, a stable supply of affordable housing of around 20,000-30,000 homes per annum would start to ease the challenge for the growing numbers that need that price point,” Proud says.

“A stable 200,000 homes delivered per annum with at least one third being rentals over time produces an equilibrium supply and a more stable pricing growth than what we have seen in the past three years.”

The government has also come out with the draft of their Housing Australia Future Fund (HAFF) legislation which promises to build 30,000 homes in the next five years.

But efforts like these will take time, and the current dire rental situation calls for immediate action, says Lawless.

“While the federal budget has outlined a boost for social and community housing funding, along with incentives for institutional investment in the build to rent sector, this additional funding doesn’t go live until 2024, and is likely to be a slow burn after that due to factors such as planning and build time,” Lawless says.

“There isn’t much immediacy in the rental supply response, so a focus on fast-tracking rental supply would be well received.”

More private investors needed

While not the only solution, private investors are one of many important variables required to solve the rental problem says Kent Lardner, director of Suburbtrends.

“Driving private investors out of the market will see fewer rentals added or replenished, he says. “We need more supply of new stock and plenty of private investors buying them as rentals.”

Margaret Lomas, veteran property investor and founder of Destiny Financial Solutions says reducing stress on investors by providing incentives would encourage them to return to the market.

“We need to make it easier to become a landlord and provide better protection to landlords who are now becoming afraid of getting a tenant they can never evict,” she says.

SQM’s Christopher agrees and noted that property investors do represent part of the current solution.

“Property developers need presales before they commit to undertaking a new housing development. Those pre-sales generally come from owner occupiers and the property investor community,” he says.

UDIA NSW’s Mann says the government also needs to deploy policies to get pre-sales moving, such as removing stamp duty and the foreign investor surcharge.

“Building new homes takes time. We need to ensure developments that have commenced and under construction are completed, especially during these immensely challenging times with escalating interest rates, supply chain disruptions, high material cost increases, resource shortages and the real threat of more builder insolvencies,” Mann says.

Vulnerable renters will also need immediate assistance, but the $6 billion a year Commonwealth Rental Assistance has to be retargeted, Dr Fotheringham of AHURI says.

“We did some modelling of this a couple of years ago, and we found that all the government has to do is tie the payments to not just the income of the household but also the level of rent they’re paying so that those lower income households that are paying more than 30 per cent of their income in housing, or in rental stress, those are the ones that receive it. Those who are paying lower rent don’t need to receive it.

“This will save some and get a more efficient response. It is a pretty simple thing to do, and we’d be keen to see implemented.”

While experts agree that there isn’t one silver bullet to address the current rental crisis, they also agree that prolonging the pain is not a viable approach.

The government has the tools and resources to ensure greater housing supply, they just need the political will to do it.

Whether you’re considering refinancing, looking for a new home or your first home, you need to rid your life of these financial red flags right now.

Whether you’re considering refinancing, looking for a new home or trying to get your first leg up on the property ladder, you need to get rid of any financial red flags, in all aspects of your life, now.

This includes a three-month “home loan cleanse” according to finance guru Mark Bouris.

In an uncertain real estate market, with borrowers coming under increasing pressure as interest rates continue to rise, home buyers need to make themselves as attractive a proposition to lend money to as possible.

That means cutting the financial fat out of your money diet.

“You need to clean up your expense profile, such as your betting app, that can indicate a habitual expenditure process,” Mr Bouris, executive chairman of Yellow Brick Road said.

“You need to reduce your exposure, and reduce the level of risk lenders see in you. A lot of people don’t understand that things that might seem simple, such as how many credit cards you have, can dramatically affect your chances of getting a loan.

“That’s why you need to embark on a three month cleanse of your finances. To illustrate a spending pattern, or lack of habitual spending, that shows you’re not a lending risk.”

As banks come under increasing pressure from the industry regulator APRA and shareholders to limit who they are lending to and how much, prospective borrowers need to clean up their finances more than ever.

Mr Bouris suggests people use a broker to help you with the cleanse – “they know all the tricks” – but he also recommends people do their own research and are diligent and disciplined about what they need and want in their lives.

It’s not just about deleting your betting app, but about ensuring there aren’t numerous betting deductions against your saving accounts or late night visits to the casino, for example.

There’s also your credit cards, which can be a big black mark against you.

“If you have three credit cards, ask yourself if you really need them all,” Mr Bouris said.

“You should only keep what you really need because lenders assess you on all your cards. So if for example, you have three cards, each with a $4000 limit, the lenders will assume you owe 12 thousand, so get rid of as many as you can.”

Your use of Buy Now Pay Later services such as Afterpay could also cause issues, as lenders could consider that monies owed also.

You should also question your use of food delivery services and streaming services, deleting those apps where possible too.

“I know plenty of people who have Netflix for example but never look at it, get rid of those too if you can, ” Mr Bouris said.

“You can always have a break and if you decide you want it back, you can sign up again.

“If you have a cleaner, that’s something else you should look at. Do you need them, do you need them as often?

“Review everything, and again a broker can really help you here. Wait three months to do it, to clean things up and then go hard for that loan.”

Getting yourself match fit for your loan also gives you a chance to understand what that cost of living squeeze might be after you refinance or b

uy that new house. Can you keep that kind of budgeting up?

It gives you an good idea of what sort lifestyle you are signing up for and if you decide it’s not for you, you can always pull back the boundaries.

“If you try it out and you don’t like living that way, you can always borrow less,” Mr Bouris said.

“Change what you want. Instead of going for that dream house, go for a townhouse or a semi-detached home and have the lifestyle you want. You don’t have to borrow $1.5 million and live on Vegemite toast.”

HOW TO GO ABOUT YOUR THREE MONTH HOME LOAN CLEANSE

– Limit/stop habitual spending

– Delete your betting app

– Reduce the amount of credit cards you have

– Don’t use Buy Now Pay Later services, clear any debt to them you have

– No more food delivery services

– Limit your streaming services subscriptions

– Be disciplined but disciplined about what sacrifices you can make

– Give it three months and go hard for that loan

– If you don’t like living that way, you can always borrow less