Mixed messages are being spread when it comes to the current property market, begging questions such as “is it a good time to buy?” and “should we hold off for the market to drop?”

The last two years has seen a once-in-a-lifetime boom across the Central Coast leaving many asking how we are currently tracking as interest rates continue to rise.

Aus Property Professionals founder and managing director Lloyd Edge has described the Central Coast market as in decline and revealed standout suburbs for buyers and investors including Gorokan and Wyong.

“Currently, the Central Coast market is in a decline, as we’re coming to the end of a boom cycle,” Mr Edge told the Express.

“The market saw a 40 per cent growth overall during the pandemic, and now rising interest rates are causing property prices to drop. However, from mid-next year onwards, when the interest rate situation calms down, we should see another boom cycle begin for the Central Coast.”

However Belle Property Central Coast principal Cathy Baker disagrees that the market is in decline.

“We’re not seeing a decline in prices, it’s just a little bit slower and there are less buyers,” she said.

“It’s definitely a changing market, there’s been a lot of uncertainty due to interest rates, the election and media around the building industry.

“A lot of growth and the boom we had was around holiday homes. At this time of year people don’t tend to be as active in that area.

“The sales we are making are in line with property prices, within the 10 per cent range.”

Ms Baker said she hadn’t seen people doing fire sales or prices taking a “big hit”.

“We are still ahead of 2020 prices,” she said.

She said there would always be a bit of a correction after the last two year boom.

“Properties need to priced to the market. Agents need to be skilful to align the properties to reflect a realistic price range,” she said.

Ms Baker said waterfront sales remained strong despite less buyers.

“We are still looking at places for $10m plus. We still have a steady stream of investors qualified to buy,” she said.

“The coast is still being looked at favourably for investors looking for dual-living purpose to have a foothold here and in Sydney.

“It’s a good time to buy. There’s a good selection and you are able to do your due diligence around what value for money is. It’s just a case that it’s always changing, we just need to align with it.”

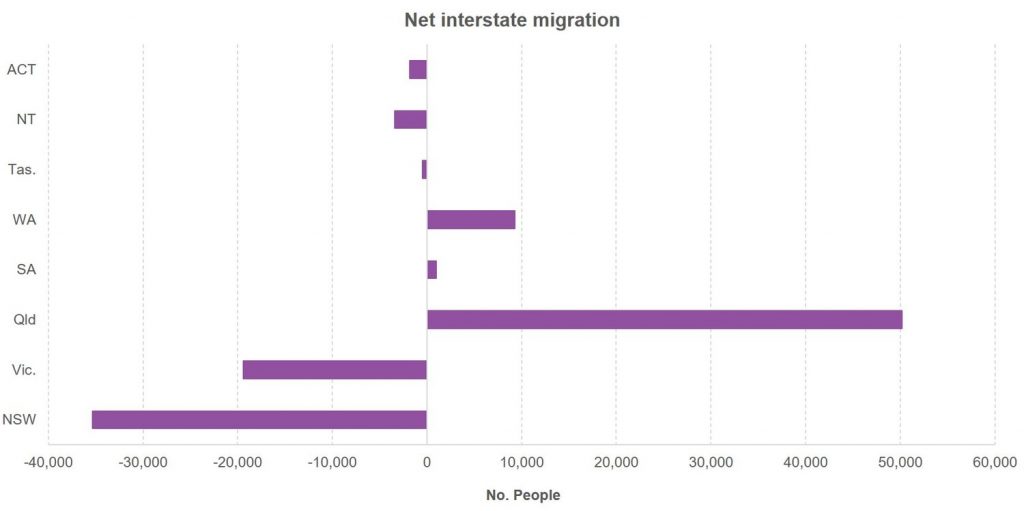

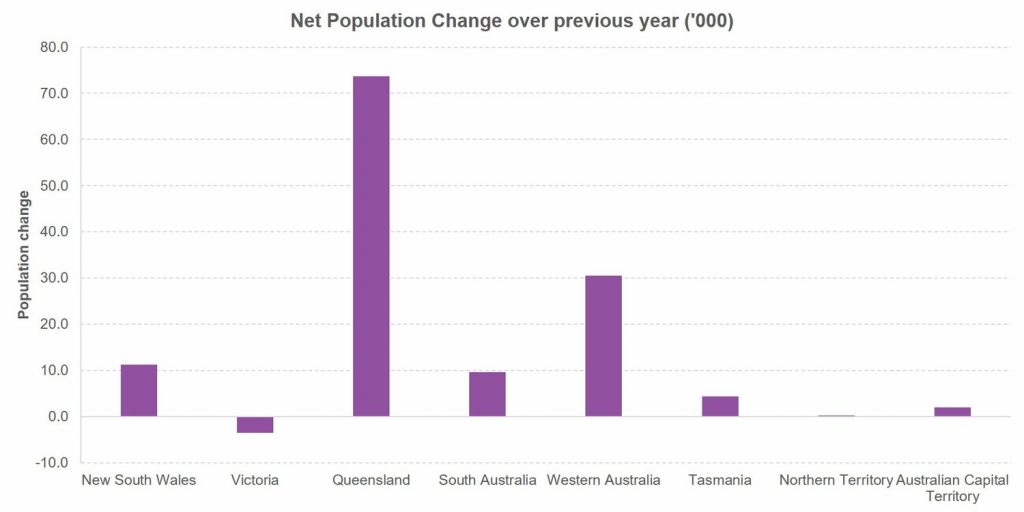

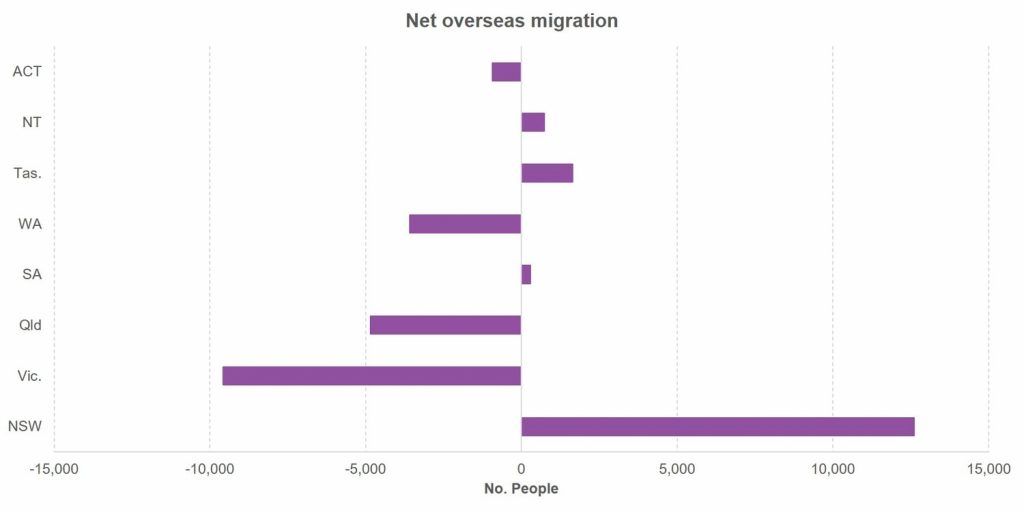

The latest population data has been released from the ABS today and demonstrated that Queensland is leading the nation in net interstate migration and population growth overall. In fact it is not just leading, it is dominating as a destination where people want to live. People are voting with their feet and leaving NSW and Victoria for sunnier climates and more affordable property. Jobs are relatively easy to come by compared to previous years, so the 25-44 year olds that drive Australia’s economy are increasingly packing up their families and moving to the Sunshine State.

The problem is that SEQ is almost full. Poor planning and monitoring of supply and infrastructure capacities has meant that most suburbs have little spare capacity in rental properties or available homes. Transactions are down because residents don’t want to risk being homeless. Brisbane City Council has attempted to address the supply imbalance by making those persons who have an investment property being used as short stay or air-bnb pay commercial rates. Whilst this may or may not be legal given the retrospective attributes to this announcement, it does demonstrate in real terms how desperate the councils have become to lift supply any way possible in the short term.

All of this comes on the back of a development industry that is suffering from the following; * Skills shortages in the construction sector; * Breakdowns in the supply chains; * An almost doubling of the time to build a detached home in many locations; * Considerable uncertainty around medium and high rise construction costs causing developers to shelve projects; * Long approval processes for greenfield sites whereby masterplanned communities usually take in excess of a decade to commence; * Layers and layers of legislation and overlays for large projects; * Shortages of good quality, well located industrial land; * Many road networks are stretched beyond capacity during peak hour.

With Queensland accounting for 57% of the nations total population growth and Western Australia another 23%, both States have some population issues to deal with. Resolving them quickly won’t be easy, nor will it be cheap.

Any talk of a residential price crash in SEQ for the moment would also seem highly unlikely. However the damage of an undersupplied market can be equally as harmful as one that is oversupplied.

What should be of significant concern to our policy makers is that overseas migration has not rebounded yet. When it does, Queensland’s economy will be supercharged much like the early 2000’s which set off almost a decade of growth.

What the population data alludes to is that the impacts of the Pandemic are far from being resolved. Business as usual is anything but. Whilst Queensland should continue to roll out the welcome mat, perhaps it should also state, “Please queue here”.

The John Hunter Hospital, the M1, Nelson Bay Road, and the New England Highway are among a dozen Hunter assets set to receive multi-million dollar boosts as outlined in Tuesday’s NSW State Budget.

Other projects to receive a tick of approval include fast rail connecting the Greater Hunter with the rest of NSW, the Hunter Valley Flood Mitigation Scheme as well as upgraded housing for First Nations people.

The region’s current growth rate is 1.4%, indicating funding for projects including health precinct development, infrastructure and road upgrades are necessary, welcome commitments for Hunter residents says Property Council of Australia’s Hunter Regional Director Anita Hugo.

This week’s budget, she says, delivers on its focus on infrastructure that would ultimately boost economic activity, development and job opportunities.

“This is welcome news but as a growing region we should always be planning for more,” Ms Hugo said.

“It was great to see an allocation of $300 million towards infrastructure delivery across key regional areas and we wait with interest to see how much of this will come to the Hunter and Central Coast.

“Strong funding was committed in the budget to ongoing delivery of health facility projects with $55m earmarked for the Hunter and it was also good to see a continued commitment of funding towards major road projects across the region including the Muswellbrook bypass.

“We should be leveraging off current commitments that will significantly grow our regional and state economies.”

Funding commitments to hospital and health precincts across the Hunter region have included $835 million allocated for the John Hunter Health and Innovation Precinct and a further $111.5 million to the Cessnock Hospital redevelopment.

More than $1.4 billion has been allocated over the next four years for the continued planning of the Pacific Motorway (M1) extension to Raymond Terrace and for the early works of construction on the widening of the Hexham Straight.

The next four years will also see $265.8 million pumped into the continued planning, design and commencement of preconstruction on the Muswellbrook bypass.

Other smaller road projects funded by the Budget include $36.6 million for the New England Highway upgrade, $19.8 million for the planning and commencement of the Singleton Bypass and $9.7 million for the flood immunity works on the Golden Highway at Mudies Creek.

Regional investment in planning and flood mitigation have also continued, with the Budget outlining $21.5 million in additional funding over eight years to maintain the Hunter Valley Flood Mitigation Scheme.

A commitment of $6.6 million will deliver new and upgraded quality homes for First Nations people through the Aboriginal Housing Office.

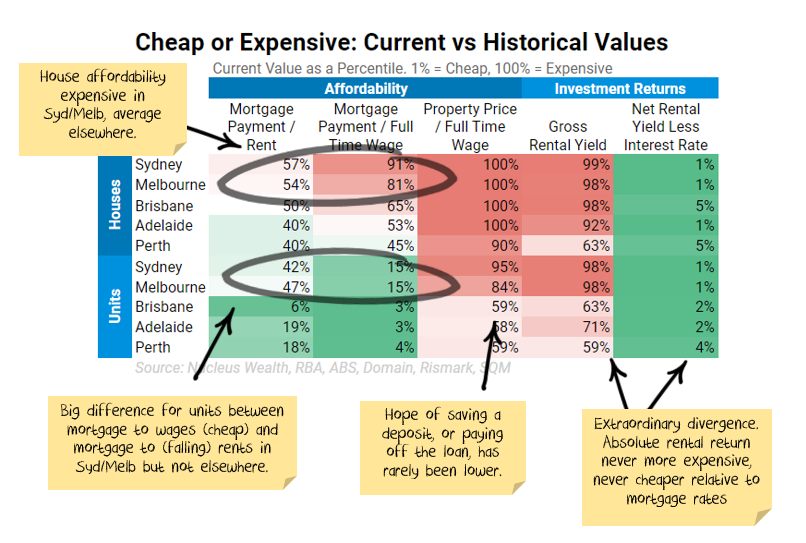

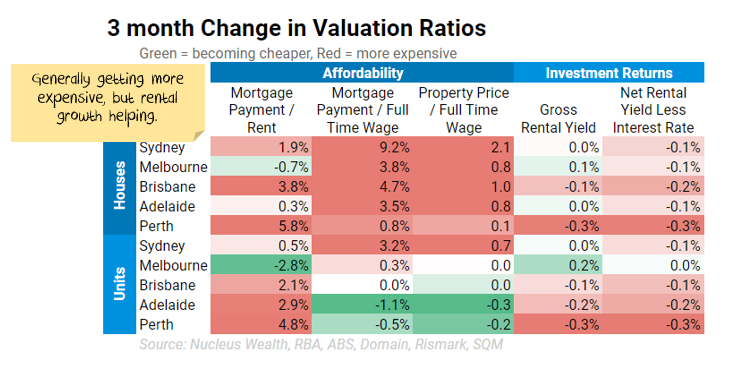

Australian property market prices continued to climb over the last month, with the past six months seeing some of the strongest growth on record. Mortgage fixed interest rates rose slightly, standard variable rates fell slightly but remain significantly above fixed rates. There are some extraordinary divergences in affordability. It has never been cheaper in some markets to service a mortgage, but never more expensive to save for a deposit or pay off the loan.

In general, housing valuation and affordability statistics worsened over August. For investors, rental yields have never been lower in an absolute sense, never higher relative to mortgage rates.

Regulatory actions in the background are worth watching. We are not expecting rising interest rates, but markets are starting to price them in. Last week the Reserve Bank of Australia had to intervene to keep interest rates in their desired range. We note even without official interest rate rises, bank funding costs will rise due to other regulatory changes. It is likely this will flow through to higher interest rates even with no official rate rises.

The Federal Government and Reserve Bank have successfully distorted conditions to encourage as many people as possible to borrow as much as possible. An investment in housing is basically a vote of confidence in their ability to keep force-feeding the market.

We run an Australian property market calculator to help investors or potential homeowners determine the returns on Australian property. The idea we want to illustrate is that there are a number of key inputs into housing valuation. Interest rates are the most important, but the other limiting factors are:

Mortgage Payments to Rent: comparing the cost of a mortgage with the cost of renting the same house. Using this ratio to constrain house prices, we assume that people will prefer to rent when the ratio gets high rather than buy.

Mortgage Payments to Wages: assuming when the ratio gets high, people rent because they cannot afford to buy.

Property Prices to Wages: assuming when the ratio gets high, people rent because they cannot save enough money to afford a deposit. We treat this as less important than the above two ratios.

Rental Yield: Rental yield is the annual rent divided by the property price. By using this ratio to forecast prices, you are assuming when the ratio gets low investors will not buy property as they are not getting a return that is high enough.

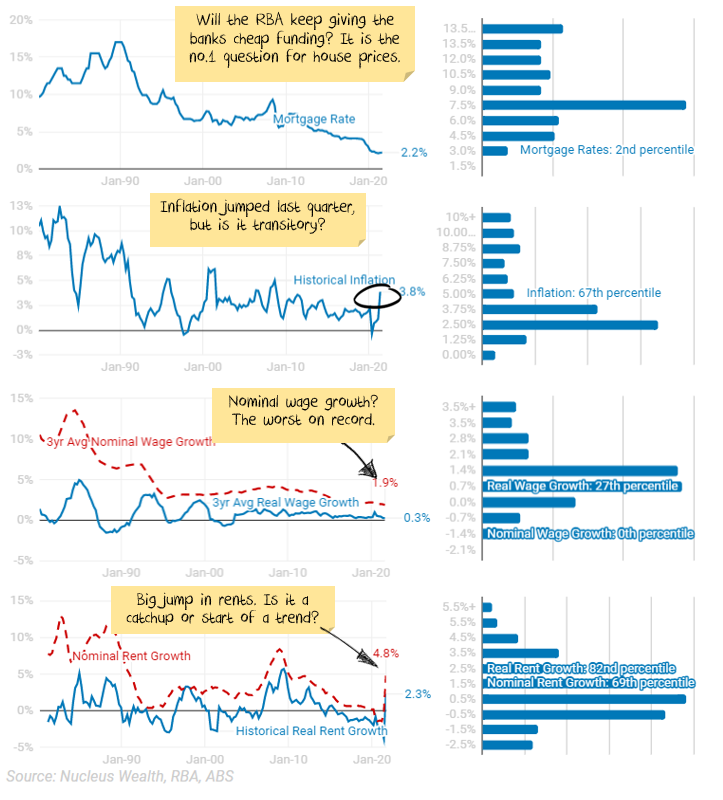

Australian mortgage rates can go lower but look like rising first.

There are effectively two different interest rates at the moment, the floating rate and the three-year fixed rate.

The floating rate is determined mainly based on the Reserve Bank of Australia. It reduced the floating rate to 0.1% in March 2020, which reduced the standard variable rate from banks to around 4.5%. This is unlikely to change.

In March 2020, the Reserve Bank also introduced a facility where they lent directly to the banks at 0.1% for three years. This facility (and other market interventions) allowed banks to drop three-year fixed mortgages to around 2%. Its name is the Term Funding Facility. It ended at the end of June.

When you adjust the factors in our property market calculator, you find that with low inflation, wage growth and rent growth that interest rates become even more important for determining property prices. But forget about the cash rate. The important factor is three-year fixed interest rate. This has risen very marginally. It seems likely the three-year rate will continue to rise unless we see further government or Reserve Bank intervention.

The short/medium term supply myth

Don’t get me wrong. The number of houses that get built matters eventually. But, in the short and medium term, affordability matters more.

The reason is that the stock of houses dwarfs the year to year supply numbers:

Each year Australia builds 100,000-200,000 dwellings

There are about 11m houses

11% are unoccupied (i.e. second homes, holiday homes, unleased properties etc)

At last census, there were 2.6 people per occupied dwelling

Do you want to absorb 350,000 new dwellings? Fewer flatmates per house, more young adults moving out. It doesn’t even show up in the rounded ratio of 2.6! Officially the number of people per occupied dwelling was 2.64. Change that to 2.55 and there are 350,000 new homes occupied.

How about another 150,000 new dwellings? Same trick with the rounded unoccupied rate of 11%. Change it from 10.5% to 11.4%.

Net effect: you could spend three or four years building another 500,000 dwellings, the population could stay the same, every new home could be bought and there would still be 2.6 people per house and 11% unoccupied.

I’m not arguing that supply doesn’t matter. It does. But over five year periods, affordability plays a far larger role.

Australian mortgage rates can go lower but look like rising first.

There are effectively two different interest rates at the moment, the floating rate and the three-year fixed rate.

The floating rate is determined mainly based on the Reserve Bank of Australia. It reduced the floating rate to 0.1% in March 2020, which reduced the standard variable rate from banks to around 4.5%. This is unlikely to change.

In March 2020, the Reserve Bank also introduced a facility where they lent directly to the banks at 0.1% for three years. This facility (and other market interventions) allowed banks to drop three-year fixed mortgages to around 2%. Its name is the Term Funding Facility. It ended at the end of June.

When you adjust the factors in our property market calculator, you find that with low inflation, wage growth and rent growth that interest rates become even more important for determining property prices. But forget about the cash rate. The important factor is three-year fixed interest rate. This has risen very marginally. It seems likely the three-year rate will continue to rise unless we see further government or Reserve Bank intervention.

The short/medium term supply myth

Don’t get me wrong. The number of houses that get built matters eventually. But, in the short and medium term, affordability matters more.

The reason is that the stock of houses dwarfs the year to year supply numbers:

Each year Australia builds 100,000-200,000 dwellings

There are about 11m houses

11% are unoccupied (i.e. second homes, holiday homes, unleased properties etc)

At last census, there were 2.6 people per occupied dwelling

Do you want to absorb 350,000 new dwellings? Fewer flatmates per house, more young adults moving out. It doesn’t even show up in the rounded ratio of 2.6! Officially the number of people per occupied dwelling was 2.64. Change that to 2.55 and there are 350,000 new homes occupied.

How about another 150,000 new dwellings? Same trick with the rounded unoccupied rate of 11%. Change it from 10.5% to 11.4%.

Net effect: you could spend three or four years building another 500,000 dwellings, the population could stay the same, every new home could be bought and there would still be 2.6 people per house and 11% unoccupied.

I’m not arguing that supply doesn’t matter. It does. But over five year periods, affordability plays a far larger role.

Australian Property Market Outlook

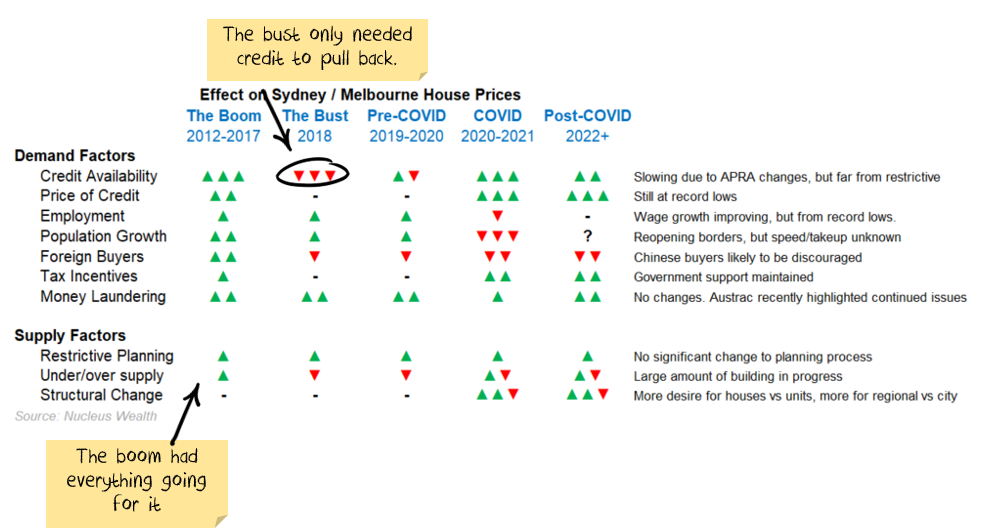

Property prices have been ripping higher in recent months. This has dented a number of affordability measures, but ongoing conditions appear as positive as they have been for some time.

On the one hand, plummeting immigration, pandemic disruptions and the end of eviction/mortgage payment moratoriums aren’t helping. A boost in supply is in progress, spurred by new home building. Rental growth jumped this quarter, but the last few years have been very weak. And Australia starts with a larger private debt burden than just about any other country. On the other, we have a burning political desire to keep Australian property market prices high and pump more debt into the economy. Wage growth is low, meaning interest rates can stay lower for longer. We have a roadmap to much lower interest rates to help. There is a structurally higher demand for houses vs units due to the fear of more lockdowns.

Australia is stuck in a debt trap. We’ve got so much debt we can’t raise rates because it makes it more difficult for people to pay back debt. To get more growth we have to cut rates, so people borrow more and the cycle goes on. In the meantime, there are other ways to keep the property party going. Once mortgages were for 20 years, then 25, now 30. Soon it will be 50. Japan has 100 year mortgages. Many people will never pay their mortgage back, so owning a home might become like renting – just that it’s renting from the bank.

Sources:

Nucleus Wealth has compiled this data using a range of different sources. We use Domain for more recent data quarterly property prices and rents, cross-checked with SQM to fill any short-term moves. Older information is from Rismark and the Australian Bureau of Statistics to fill time series. For economic data, we use either Reserve Bank of Australia or Australia Bureau of Statistics data. For older data, we have had to estimate some factors due to differing definitions over time.

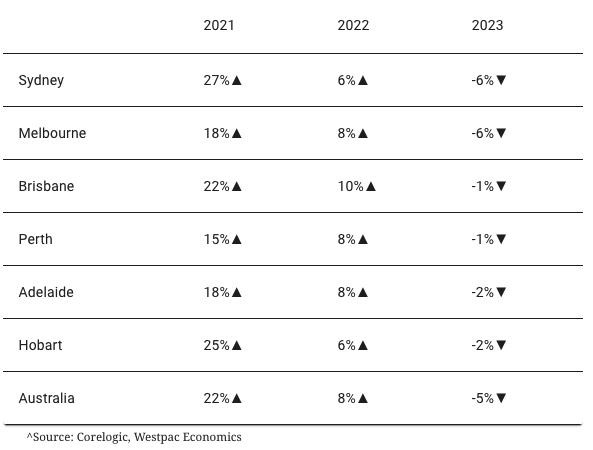

Westpac has upgraded its housing market forecasts, tipping house prices to lift by a further 5 per cent in the remaining three months of 2021 to be up 22 per cent for the year.

Prices in the major capital cities are already up 17 per cent for the year to September and are tracking for a 1.5 per cent gain in October.

Westpac expects Sydney home prices to lift by 27 per cent for this year, well above its previous forecast in August of 22 per cent, before lifting again next year by 6 per cent.

Melbourne is also expected to surpass its previous forecast by 2 per cent to be up 18 per cent for the year.

Brisbane’s house prices, already up 19.9 per cent over the last ten months, still has a further 2 per cent to grow before the close of the year, before picking up again by 10 per cent in 2022.

Nationally, prices are forecast to lift again next year, with Westpac revising its earlier call of 5 per cent to 8 per cent.

The bank expects most of 2022’s increase to be weighted in the first half of the year before moderating.

When are Australian house prices expected to drop?

Westpac chief economist Bill Evans said the bank was preparing for the market to move into a correction phase in early 2023 as higher interest rates, stretched affordability and the tightening of macro-prudential policies take hold.

“While the market upturn has weathered the latest Covid disruptions very well and is clearly carrying strong momentum, the boom is entering trickier territory,” Evans said.

“Price momentum has held up near term, prompting us to revise up the near-term outlook for prices.

“However, affordability is becoming stretched and policy tightening is now in play.”

Dwelling price forecasts

Westpac was the first major bank to tip rate rises ahead of the Reserve Bank’s current 2024 guidance, with Evans forecasting the first increase above the current historically low 0.1 per cent in early March 2023. Other economists are preparing for the RBA to begin raising rates over 2023 and 2024 to a natural rate of about 1.25 per cent. Westpac estimates rates any higher would place “significant stress” on household finances. “We still expect the market to slow over the course of 2022 as macro-prudential policy; prospects of increased rates; and affordability reaching record lows triggers a correction phase that will begin in 2023 and is likely to extend into 2024,” Evans said. “The combination of high levels of new building and slow population-driven demand may also weigh on some sub-markets.” Corelogic research director Tim Lawless said the slowing growth conditions were the result of higher barriers to entry for non-home owners along with fewer government incentives to enter the market. “With housing values rising substantially faster than household incomes, raising a deposit has become more challenging for most cohorts of the market, especially first home buyers,” Lawless said. “Existing home owners looking to upgrade, downsize or move home may be less impacted as they have had the benefit of equity that has accrued as housing values surged.” Housing credit has been growing at an annualised pace of about 7 per cent in recent months, more than double the rate of income growth. According to data from the Australian Prudential Regulation Authority, the number of new mortgage loans where debt is at least six times greater than income lifted by 6 per cent in the June quarter.

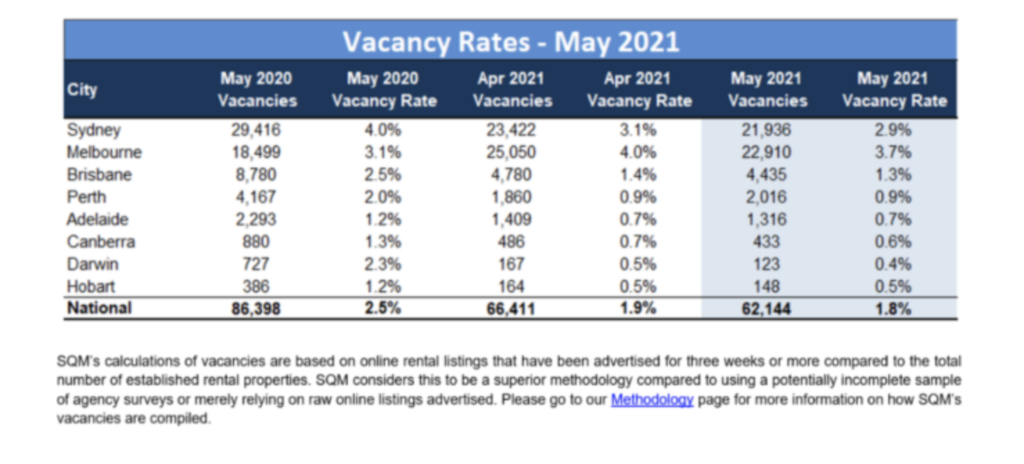

SQM Research has released its rental vacancy report for May, which reports a national rental vacancy rate of only 1.8% – the lowest level of vacancies since October 2012.

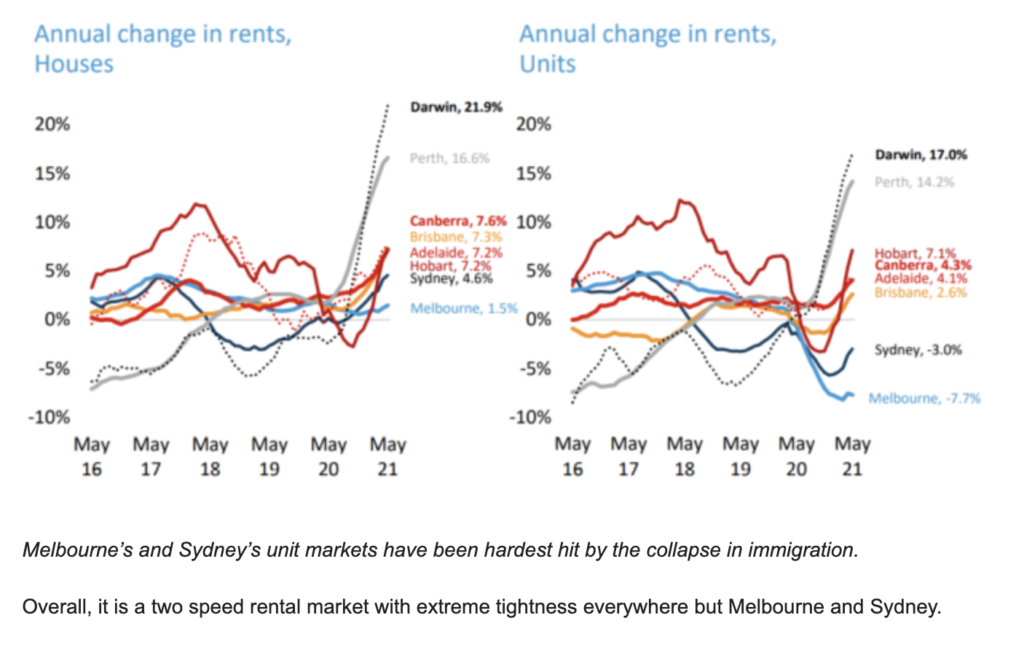

Rental vacancies are zipped tight everywhere except Melbourne and Sydney, which have been hit hardest by the loss of international students, as illustrated clearly in the table below.

Rental vacancies are tight everywhere outside of Melbourne and Sydney.

According to SQM Managing Director Louis Christopher, rental vacancy rates have fallen across the board, which has driven rents higher:

“Rental vacancy rates have fallen across the board in May, driving rents higher, especially in regional locations. This trend is likely to remain through the second half of the year, given the fierce competition for rental accommodation in many areas. We are still seeing falling vacancies everywhere from Victoria’s Mornington Peninsula, the Gold Coast, right through to inland areas like the Murray Regions of NSW and South Australia to outback Northern Territory, along with Darwin, which is having the effect of boosting rents as tenants compete for rental homes”.

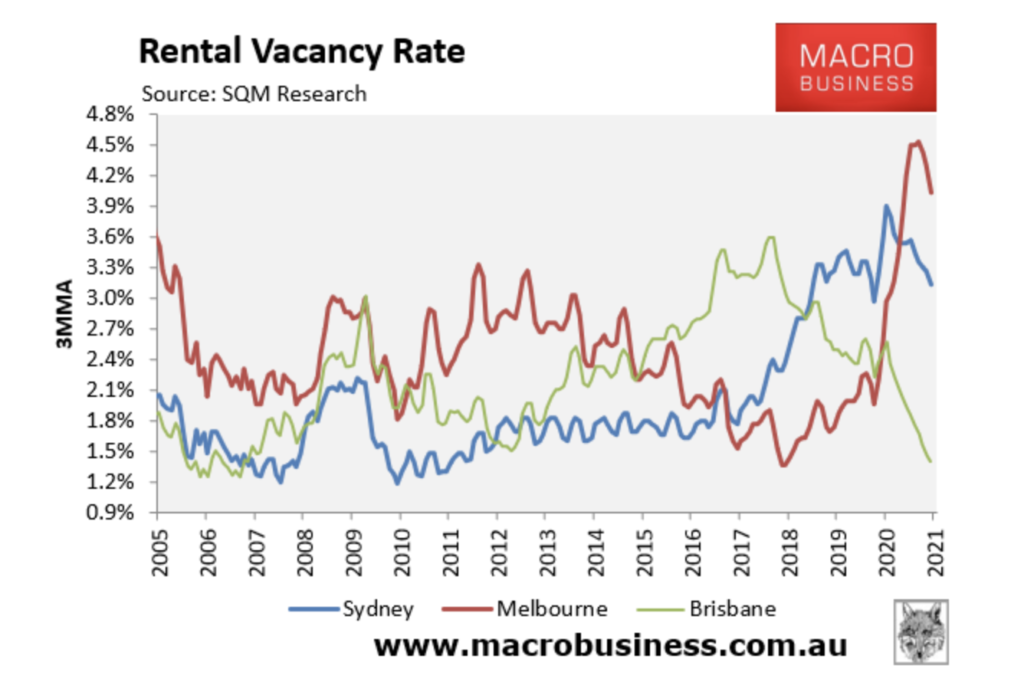

The biggest contrast is seen across the three major east coast cities – Sydney, Melbourne and Brisbane. Brisbane’s rental vacancy rate has shrunk while Melbourne’s and Sydney’s is elevated:

risbane’s rental vacancies have diverged sharply from Melbourne’s and Sydney’s.

SQM’s rental vacancy data accords with CoreLogic’s latest rental results, which shows strong rental growth outside of Sydney and Melbourne, alongside very strong rental growth nationally:

Queensland also takes the second and third position in the charts with Mackay LGA and Toowoomba, respectively.

In NSW, Port Stephens LGA, Greater Hume Region Federation LGA and Federation LGA make the top ten list.

Representing Victoria are Greater Bendigo City, Greater Geelong LGA and Warrnambool.

Tasmania’s Circular Head takes the final position in the top ten line up.

Regional areas have become the most attractive option throughout 2020, with evidence of buyers capitalising on lower median property prices.

The ‘PRD Stand Out Regions’ report highlights affordable regional areas in QLD, VIC, NSW, and TAS.

These areas have median price affordability and provide strong indicators for property investment, local employment growth, and a sustainable economic future.

The selection criteria includes:

Affordability: The Local Government Area (LGA) has a median price below the maximum affordable property sale price.

Trends: The LGA will have 20 transactions or more in 2019 and 2020, with positive price growth within that time.

Investment: To ensure solid investment opportunities, the LGA will have an on-par or higher rental yield than its capital city, as well as an on-par or lower vacancy rate.

Development: There will be a high estimated value of future project development, with a higher concentration of commercial and infrastructure projects to ensure a positive economic outlook.

Unemployment: As of the September quarter of 2020, the LGA will have an on-par or lower unemployment rate than the state average to ensure there is local job growth.

According to the report, there has been a high influx of first home buyers that have entered the property market in 2020, resulting in a growth of 50.4% between the December quarters of 2019 and 2020. This further boosted an already strong market with record low-interest rates and increasingly lenient bank lending policies.

Experts predicted 20% drops. But 12 months after COVID-19, prices are soaring.

Exactly a year ago, things were looking bad for the Australian property market, and everything else. The pandemic was just getting started, with lockdowns, unemployment and the sudden end of the travel of the industry.

For anyone wanting to sell and buy property, open inspections switched to private viewings and auctions went online. House prices began to fall.

“Vendors are anxious, fearful and panicked. Many are bringing auctions forward or cancelling campaigns,” Real Estate Buyers Agents Association of Australia Cate Bakos told Finder in March last year.

Real estate agents were forced to cancel open inspections, in some cases even offering remote viewing via phone.

Experts suggested that in the worst-case scenario, Australian property prices could fall by 20%.

But 12 months later the Australian property market is in a completely different position. Defying the worst predictions, property prices are soaring. Auction clearance rates are high. First home buyers are back in a big way.

Property prices did fall. But not by anywhere near as much as they might have. At a national level, Australian property prices only fell from May to September of 2020 before recovering.

Melbourne, having faced the most prolonged lockdowns, saw the biggest drops. According to CoreLogic, the median 3-month average sales price for Melbourne property peaked at $712,000 in December 2019.

This average fell by 8% to $648,875 but has now crept back up $708,000, just short of the pre-COVID-19 peak.

Sydneys’ median property price was $889,992 in May last year, according to CoreLogic figures. It fell down to $859,943 in September.

Now that median sits at $895,933 and Westpac economists are predicting a further 10% rise in prices this year.

And property prices are growing in other cities and regional areas too. 2021 is looking to be a very strong year for Australian property prices. But how did we get here? How did the market go from a predicted COVID-collapse to a boom?

There are multiple factors driving prices upward now:

COVID-19 under control. It’s an obvious point but Australia’s handling of the pandemic has allowed something like normal life to resume for many of us. The fact that real estate transactions were only briefly interrupted has definitely helped the property market grow.

Low interest rates. The Reserve Bank lowered the cash rate several times before and during the pandemic. It did this not to raise house prices specifically but to boost spending and encourage economic growth. But it has resulted in historically low interest rates on home loans, making it cheaper for buyers to borrow more money.

First home buyer policies. Government policies aimed at helping home buyers, such as the First Home Loan Deposit Scheme and HomeBuilder, have given a few first time buyers a boost at a crucial time.

Recent price falls. The current growth in prices comes off the back of a very uneven period. From 2017 until 2020, prices in cities like Melbourne and Sydney fell, then rose, then fell again as COVID-19 struck. While still ridiculously expensive, prices had room to rise. Even now they’re only getting back to previous peaks in some cities.

Availability of credit. In addition to low interest rates, lenders are a little more flexible now than they were a few years ago. It’s a bit easier to get a home loan now than it was in, say, 2018 or 2019, and with government plans to simplify lending rules it could soon get even easier.

In short, COVID-19 and the economic decline that followed, along with government policy, created a situation in which property prices were bound to rise.

But it isn’t all a story of growth. For renters in certain parts of the country, notably inner-city Sydney and Melbourne apartments, rents have fallen. This is partly because travel and immigration numbers have plummeted during the pandemic, and partly because renters have flocked to suburbs with more space.

And property investment activity remains low. It’s first home buyers currently driving growth. Of course, that might change as property gets more expensive and investors start chasing big gains again.

Record-low rates, government support and stimulus measures ,and the pandemic-driven rush north by Melburnians and Sydneysiders have turbo- charged the recovery under way in Brisbane’s private rental market, pushing the vacancy rate down to a near nine-year low.

Greater Brisbane’s rental vacancy rate fell to 1.5 per cent last month from 1.7 per cent in January and was well down from 2.2 per cent a year earlier, new figures from consultancy SQM Research show, driving the overall rate in the Queensland capital to a level it last touched in July 2012.

The population growth that saw the Sunshine State gain a net 7237 people from interstate in the September quarter – while NSW shed 4110 and Victoria lost 3749 – has compounded a recovery that was already under way after the apartment-building boom triggered a private rental market vacancy rate that REIQ figures show peaked at 4.1 per cent in December 2016.

“Over 2020 there was a real acceleration in interstate migration towards Queensland and generally speaking, Brisbane is the first port of call in Queensland,” SQM managing director Louis Christopher said.

“Queensland was picking up Victorian residents – when they were allowed in, of course – they were picking up residents from Sydney and so I believe that there’s been an acceleration. But construction and dwelling completions haven’t yet responded. This is what’s leading the rental vacancy downwards.”

The tight market is already stimulating more development. Red & Co founder David Laverty, who last month acquired a $4.75 million development site in inner-city Albion, said rising rents were a leading indicator of rising capital values.

Turnaround city: Brisbane’s vacancy rate has dropped to a nine-year low. Lydia Lynch “It’s not really a natural cycle because no one really predicted we were going to have this massive boom,” said Brisbane-based Asti Mardiasmo, the chief economist of PRD Nationwide.

NO ONE REALLY PREDICTED WE WERE GOING TO HAVE THIS MASSIVE BOOM. — PRD Nationwide economist Asti Mardiasmo

“If you remember at the beginning of 2020 we were all saying the market is going strong at the moment … then the pandemic happened and everyone predicted we were going to crash. Then the government intervened and the RBA intervened.

“Because of these interventions, it has created an extraordinary cycle in the housing market. No one predicted we were going to be seeing double-digit price increases in some areas. No one predicted that rental prices will be increasing.”

Greater Brisbane had 12,332 properties for rent in January last year, when over 6000 units and houses were vacant, SQM figures show. After dropping to 9644 rental properties on market in March last year, the figure jumped back over 11,500 in April, likely boosted by owners of short- stay rentals putting their homes on the long-stay market, Mr Christopher said.

The city had 7378 vacant properties last week, comprising 4306 units and 3072 houses. But while the fast-recovering market and the factors underpinning it have prevented many of the initial worries, particularly for renters, from being realised, it has also created new concerns for them.

“At the beginning of the pandemic, everyone was scared about whether or not they were going to have a place to live because they might be losing their jobs and couldn’t afford to stay in their place,” Dr Mardiasmo said.

“Now, people can’t find a place to live because there are too many people looking for somewhere to live. There is not enough supply and rental prices have gone up. It’s really ironic.”